We all keep a substantial chunk of our savings in bank deposits without thinking for a moment of the safety of our money. Rarely would we come across a situation when a bank goes bankrupt, and is unable to refund the deposits to its customers. However unusual this might sound; this could be a possibility.

What if a bank declares insolvency and its debt obligations outstrip its total assets – leaving scores of depositors in lurch. To pre-empt such a scenario, banks are supposed to take deposit insurance.

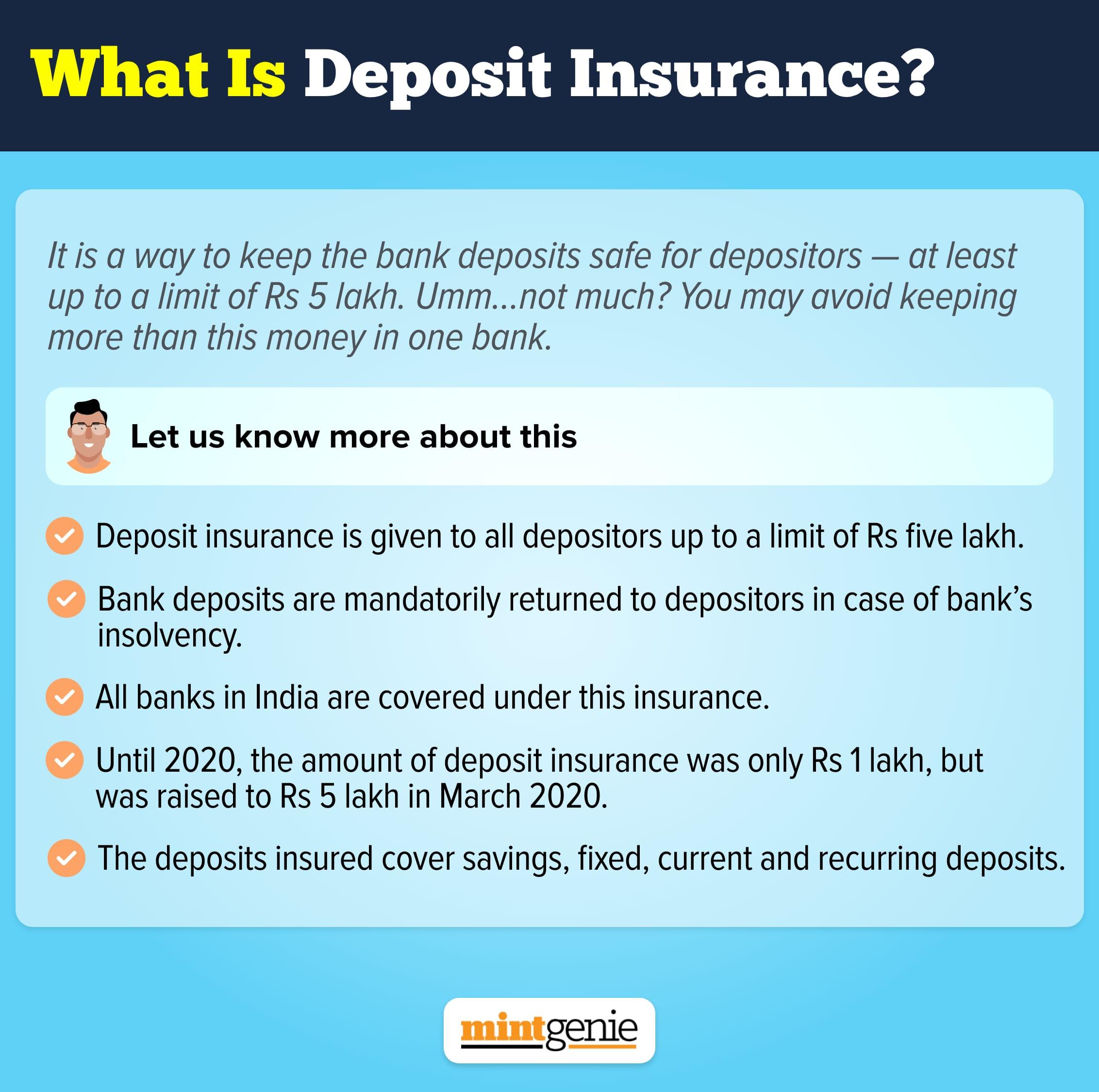

Deposit insurance is a way to keep the bank deposits safe for depositors — at least up to a certain limit. This is used only when banks find them unable to pay debts. This is a mechanism to ensure financial stability in the markets and economy. In India, this deposit insurance is available up to a limit of ₹5 lakh. This means that the bank deposits are guaranteed to be returned to depositors in case of bank’s insolvency. All banks in India are mandatorily covered under this insurance.

So, if you hold a bank account with any commercial bank, including a branch of a foreign bank, regional rural bank or local area bank, then the account must have been covered under the deposit insurance scheme.

These deposits are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC). Deposit insurance in India began in 1962. Until 2020, the amount of deposit insurance was only ₹1 lakh, but it was raised to ₹5 lakh in March 2020. This means in the case of a bank's bankruptcy; depositors stand to receive only ₹5 lakh.

The deposits insured cover savings, fixed, current and recurring deposits. In case a depositor holds multiple accounts in one bank then all the deposits held in multiple branches are put together for the purpose of deposit insurance. For instance, if a customer has ₹one lakh each in three accounts with one bank, then the total insurance amount would stand at ₹3 lakh.

The multiple accounts may also include savings, current, recurring and fixed deposits. This means the total amount saved in all different accounts held by one person are aggregated to arrive at the figure of total insurance i.e. ₹5 lakh.

The amount of ₹5 lakh includes both principal and interest combined. It is vital to note that multiple accounts held in different accounts are insured separately. This means if an individual holds accounts in two different commercial banks then the total amount of insurance will be ₹10 lakh.

So, in the case of bankruptcy of a bank, deposit insurance provides a safety net. It is a system that offers a guarantee in case of a worst-case scenario.