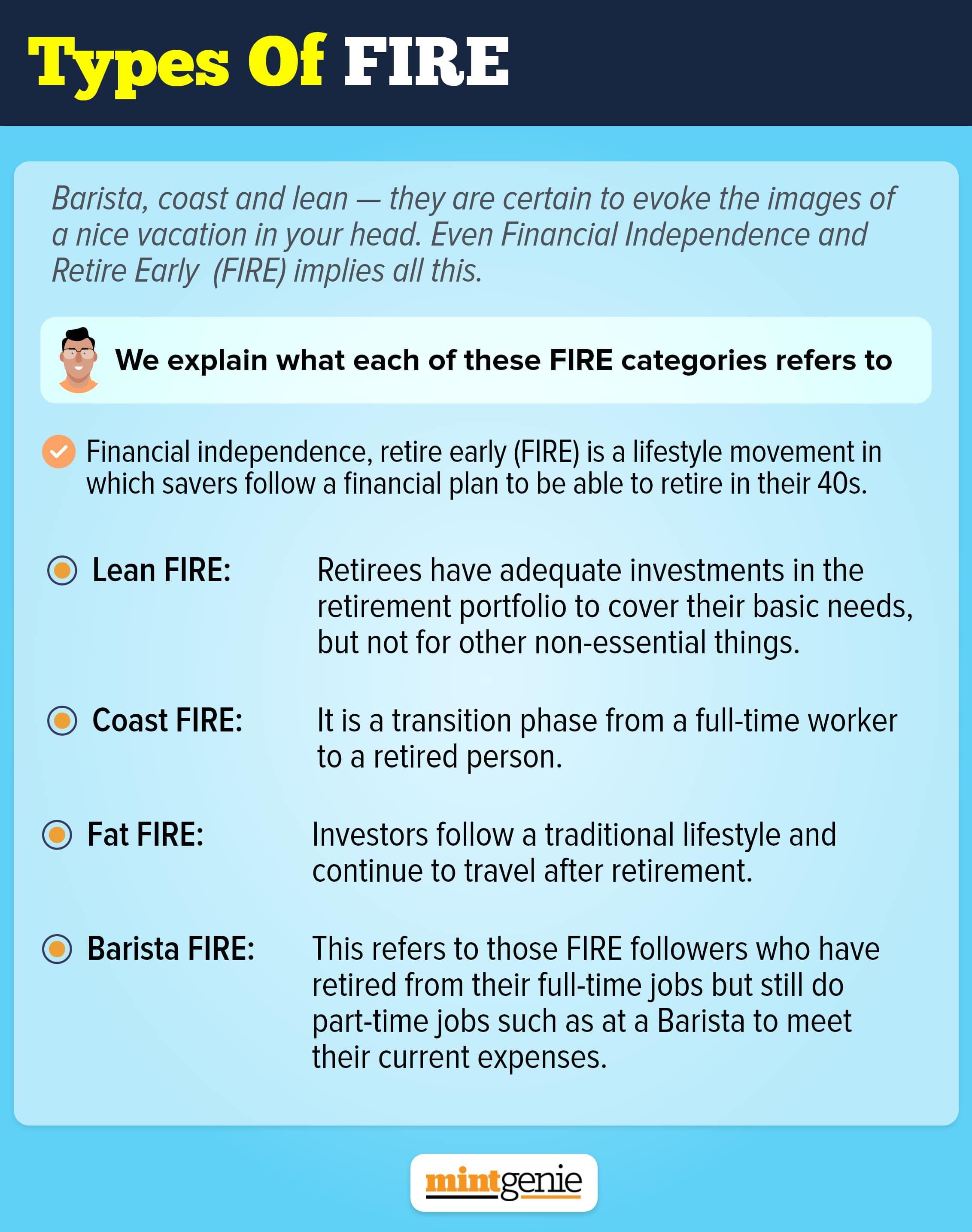

Financial independence, retire early (FIRE) is a lifestyle movement where future retirees follow an organised financial plan that allows them to retire early by resorting to a strict regime of saving. This entails a simple lifestyle since it allows the savers to save at least 70 percent of their earnings so that they can retire in their 40s, far earlier than the conventional age of retirement of 60s.

As a rule, someone who wants to retire early tends to save a substantial portion of his earnings which he can later withdraw in small chunks during retirement. As a matter of fact, FIRE is not an infallible plan, and it also entails huge sacrifices in the present for a better future.

The concept was a brainchild of Vicky Robin and Joe Dominguez who wrote a book – Your Money or Your Life that introduced the concept of FIRE. In this, each expenditure incurred is seen in relation to the time spent at work to earn the equivalent amount of money.

The philosophy of FIRE suggests that the investor ought to save at least 30 times of their annual expenditure before they decide to retire. After they have retired, the followers of FIRE, to meet their expenses, withdraw only 3-4 percent of their total savings. This requires diligence and discipline, and a strict adherence to the pre-decided spending regime.

There are four key types of FIRE:

Lean FIRE

As the name suggests, lean fire entails having adequate investments in the retirement portfolio to cover your basic needs, and not for other non-essential things such as travel and holidays. The fund in lean fire provides a safety net to savers in their post-retirement life. If one has access to 25-30 times of their annual expenses then it will be called lean fire. It will ensure a retiree to lead a decent life minus luxuries and travel with the retirement fund.

Coast FIRE

This includes a category of FIRE followers who do not retire completely, and continue to work part time despite saving enough for retirement. This means that the savers have saved enough and without investing further, this fund will automatically grow to a point where it can take care of the post retirement expenses. But FIRE followers must earn sufficient enough to meet the expenses before the fund appreciates to the point where retirees can start withdrawals.

For instance, if someone’s monthly expenditure is ₹1 lakh and he earns ₹2.5 lakh in a full-time job. Then he doesn’t need to save more than ₹1 lakh. As a result, he may leave the full-time job, and become a freelancer or consultant to earn ₹1 lakh. It is more of a transition phase from a full-time worker to a fully retired person.

Fat FIRE

This is different from lean fire in a way that the investor does not follow a strict regime but they still follow a traditional lifestyle where they save more than a regular retirement investor. This is difficult to achieve but the followers of fat fire do not have to make financial compromises in their post retirement life. They continue to travel as before.

If a person spends ₹15 lakh while he is working full time, and he wants to continue to spend leisurely, then he will need to save far more than 25 times of annual expenditure. This is made possible generally when the retirement fund is invested in interest bearing investments and generates a regular income such as through high dividend, interest or rental income and the retiree can live comfortably with this income without having to dip into the invested capital.

Barista FIRE

This refers to those followers who have taken retirement from their typical full-time jobs but still take up projects and part-time jobs to meet their current expenses for which their retirement fund falls short. This is more relevant to those who do not want to wait for too long to build a massive portfolio.

For instance, if Suresh’s monthly expenses are ₹one lakh a month, and currently his retirement fund can generate only ₹60,000 then he can leave his job now and work the job that he loves to earn the remainder of ₹40,000. The downside of this FIRE type is that he is retiring early without having an adequate retirement fund. A more conservative approach would call for earning for a few more years and save enough before retiring completely. In that case, he can still work if he wants to – but not to meet expenses.

So, we can define FIRE as a lifestyle movement where the followers stick to an organised plan to retire fairly early in their career, at least two decades prior to the conventional retirement age of 65. For this, they follow a strict saving plan, allocating nearly 70 percent of their total income, eventually creating a retirement fund which is around 30 times the annual expenditure. Once they retire, they can withdraw around 3 to 4 percent of their total retirement fund every year.