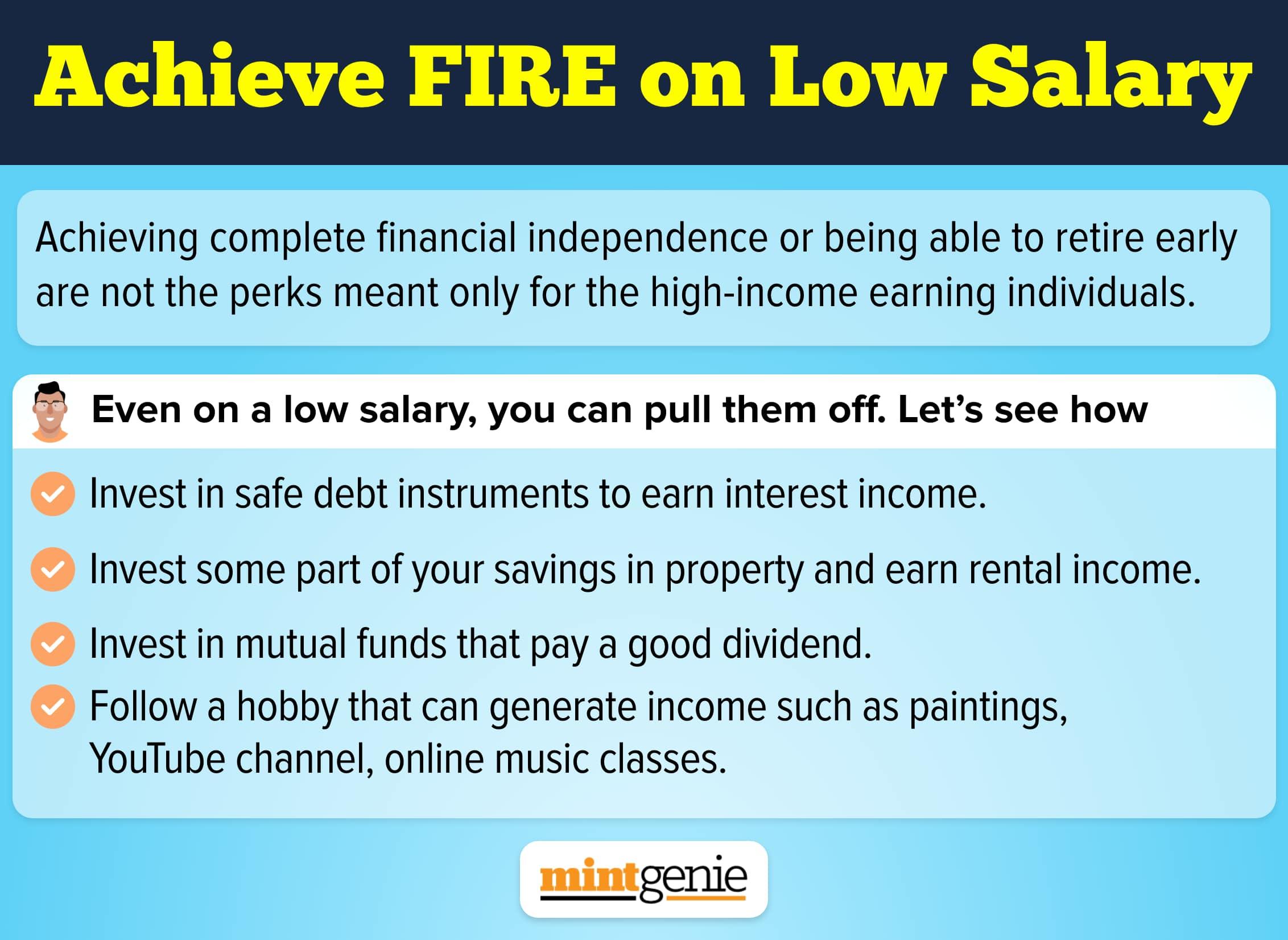

The pension fund body PFRDA (Pension Fund Regulatory and Development Authority) recently launched NPS (National Pension System) prosperity planner.

It is an easy-to-use tool of PFRDA that allows investors to calculate the amount they should invest in the NPS in order to accumulate adequate corpus at the time of retirement.

This system follows three steps. Firstly, it tells investors how much pension they stand to receive based on the current contribution. Secondly, it tells them how much pension they will need based on their monthly expenses and expected inflation in future. And finally, it suggests what plan of action can be taken to resolve this. In other words, how much additional contribution they need to make to fill the deficit.

Pension you stand to receive:

The virtual platform first asks you what category of employee you are: Centre, state, corporate or individual.

In the first step, it asks you to fill in all the details relating to date of birth, date of joining NPS and date of retirement.

The system further asks for the current NPS balance. Based on this, it tells you how much is your average yearly contribution.

For example, if your current NPS balance is ₹150,000 and you started your account seven years ago, the system will calculate that you -- on average -- contributed ₹14,898 every year and cumulatively invested ₹1,04,286 that grew at 9.1 percent CAGR to swell to ₹1,50,000.

Also, based on your age, it tells out your date of retirement assuming that you would retire at 60.

Now, the system tells you how much you stand to receive at the time of retirement in both the scenarios: with purchase price and without purchase price.

It also tells you the impact on monthly pension if you increase the annual contribution by a fixed percentage, say 10 percent.

Pension you will need:

In the second step, it calculates the actual pension requirement based on your monthly living expenses and the rate of inflation. Based on the figures you enter, it will tell you the difference of figures between what you stand to receive (with current contribution) and what you should receive to maintain the current lifestyle.

This leads you to the third and final step i.e., the action you need to take to ensure safe and secure retirement.

In the last step, the system tells investor the proportion of increase in annual contribution so as to arrive at the targeted retirement figures of annuity and monthly pension.

For example, if your annual contribution is ₹14,898 and to achieve the targeted figure, you need to make an increased contribution of ₹1,88695, then it will show the same.