Aside from common financial goals such as buying a house, car and children’s education; one of the key objectives for which we invest throughout our lives is to build a sizeable corpus for retirement.

This corpus comprises consistent saving over a long period of time, and investments across asset classes such as equity, debt, bonds, fixed deposits, mutual funds, precious metals, commodities and alternative assets.

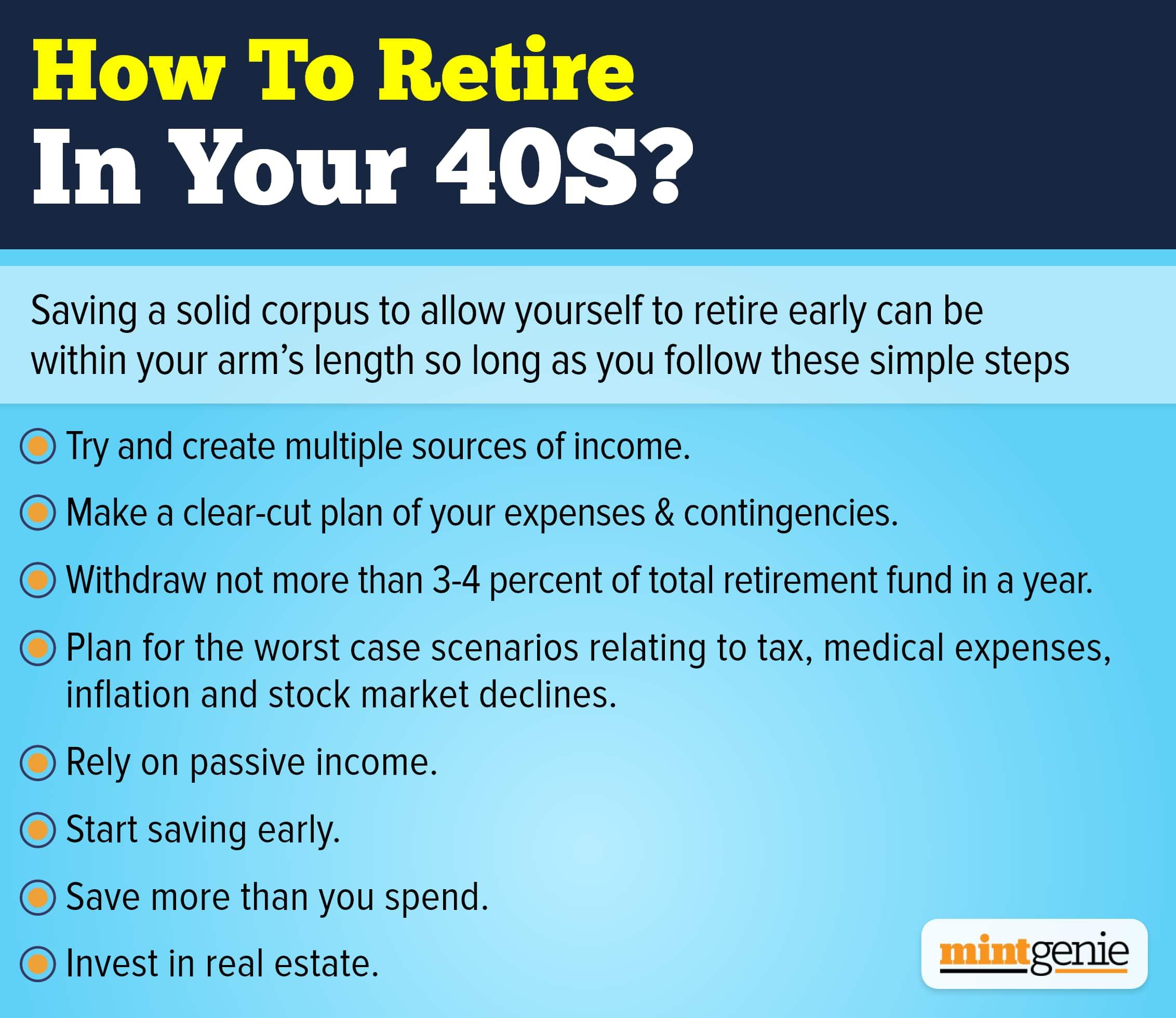

And once the corpus has been built, it is vital to ensure that it does not run out prematurely during the period of retirement. This calls for the need to stick to a safe withdrawal rate, also known as SWR.

This is a principle which ensures that investors’ retirement kitty doesn’t get exhausted during the retirement. It is vital to mention here that there is an array of factors that affect the quantum of this retirement fund and the pace at which it may get exhausted, for instance the macro-economic factors, exposure to equity at the time of retirement, rate of inflation that prevails, so on and so forth.

Since these have a direct bearing on total investments, one should be extra careful as to how much one should withdraw for the longevity of this corpus.

The age-old financial maxim states that investors should stick to 3-4 percent withdrawal from the retirement fund in a year and this can, according to experts, ensure that retirees do not run out of money during their lifetime.

The study that shows that withdrawal of 3-4 percent is a sustainable rate assumes a retirement period of 30 years and emphasises that one can withdraw 4 percent in the first year and in the subsequent years, one can withdraw inflation-adjusted withdrawals. This mechanism will ensure that the corpus does not get finished prematurely.

Although safe withdrawal rate, or SWR, is a universally accepted rule, financial advisors say that it is to be seen from case to case. A fixed pace of withdrawal may work in some case and not in other because it all depends on overall asset allocation, choice of investment tools and the returns given by the market towards the end of the working life.

“During retirement one can have asset allocation in place and keep 40 percent in equity and the remaining in fixed income instruments such as fixed deposits, post office deposits, corporate FDs, etc. And this equity investment can be withdrawn quarterly at the rate of 8 percent per annum. This can ensure that one has the required cash flow during the post-retirement and one can successfully beat the inflation. After all retirement period can be as long as 25 years, and one ought to rely on equity to beat the inflation,” says Sridharan Sundaram, SEBI Registered Investment Advisor, and founder of Wealth Ladder Direct.

So, there is another alternative to SWR, which is to calculate the total monthly expenses one would need in the post-retirement life, after factoring in inflation and calculating its present value. Then one can create a retirement fund comprising essentially of fixed income instruments and some equity.

These fixed returns should be high enough to cover the post-retirement expenses. This way, one doesn’t intend to exhaust the retirement kitty but only utlilise the fixed returns generated by it.

However, needless to mention that this kind of planning requires a higher amount of retirement corpus.