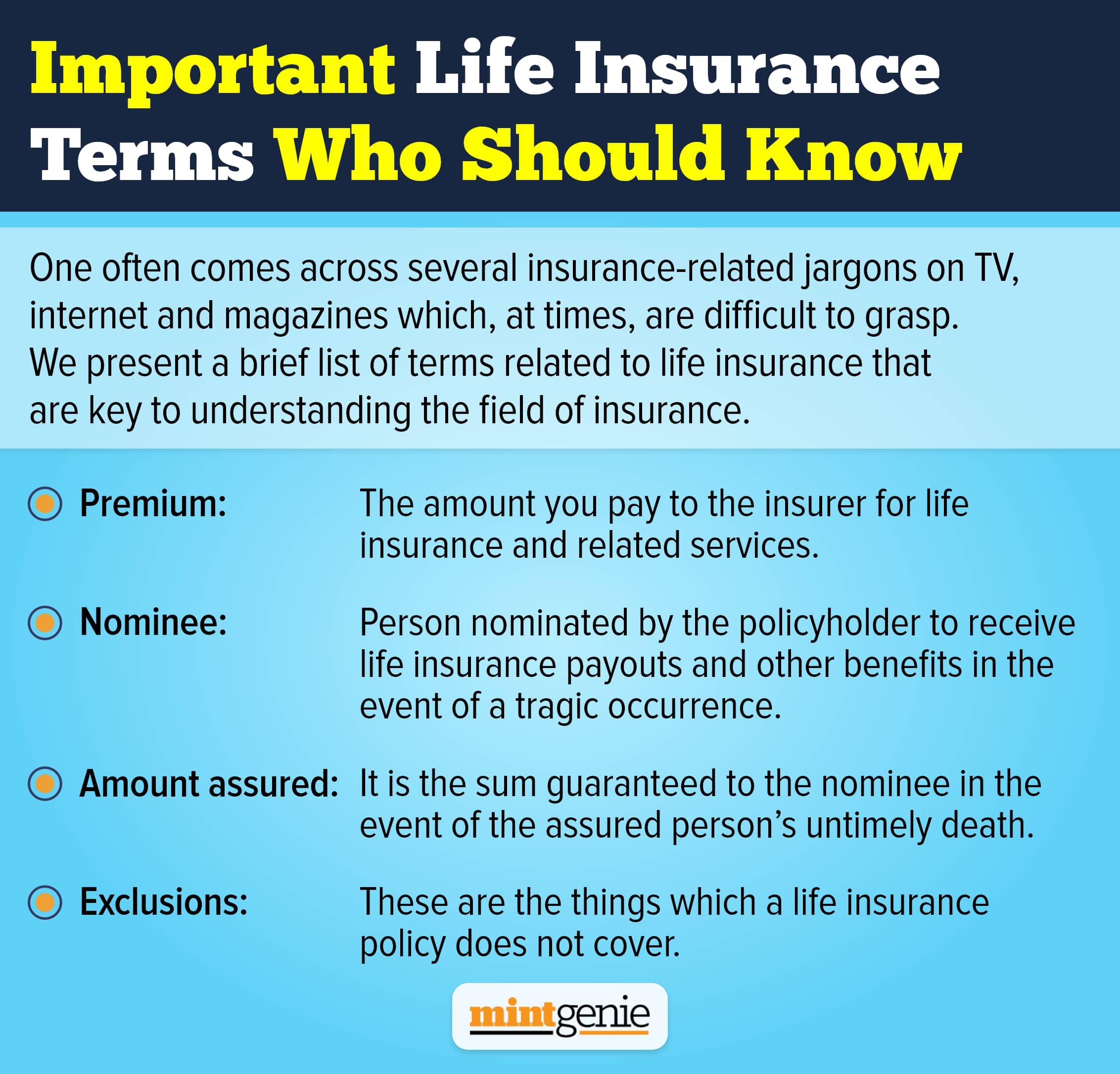

When was the last time did you hear of a homemaker buying insurance? In India, buying insurance is mostly limited to breadwinners who rely on its value to financially secure their families. This is because most life insurance products are positioned such that families look at them as an alternate income source in the event of sudden income loss owing to demise. However, if insurance is all about indemnity against unforeseen financial challenges, then buying child insurance plans would have been equally futile. Had we understood how insurance must be construed as a long-term security option, many of us would have encouraged the homemakers in our families too to buy life insurance cover.

Should homemakers buy life insurance?

The question regarding the purchase of a life insurance plan is not about rights but about responsibilities. Families must understand that the onus of buying life insurance does not lie on their earning members alone. Anyone with a family to look after or with financial responsibilities must take care to have one.

To start with, you must stop devaluing the fiscal value of homemakers. True that they are not in a salary-based nine-to-five job. However, their contribution toward running a family smoothly cannot be negated. From managing household expenses to looking after the everyday chores, teaching children and ensuring the smooth running of the house on a daily basis, homemakers add more value than their estimated worth. Most families undervalue these services, not realizing to what extent their life would be immobile without them. It’s time to reciprocate and value those selfless services in terms of money. Remember that their sudden deaths will not only leave an unfillable void for years to come but will cause a dent in your pockets as you will now have to avail all those services now.

Putting an economic value on a homemaker (aka wife, mother or elder sister) may not be easy. For this, you have to check what and how much you would have to pay to get the same chores done by an outsider or a full-time helper. Add the price that you would have to pay to ensure complete and continued service toward the children and the elders in your family. Remember that these are the expenses that most tend to ignore. The sudden loss of the family’s homemaker will put you under considerable financial duress. You can however make good the loss from the money received from the life insurance policy received, which you can then use to manage the expenses.

How can homemakers benefit from life insurance?

Buying life insurance early in life helps as it gives access to a greater coverage amount at nominal premiums. Apart, many life insurance companies have come out with exclusive plans for homemakers, especially, women who already benefit from cheaper life insurance policies as insurers offer them lower premiums compared to men.

Some insurance companies have come out with women-oriented life insurance plans keeping in mind the distinct need of single mothers and homemakers working from home. These specifically designed plans can be moneyback plans, unit-linked insurance policies, endowment policies or those providing pension cover after a certain age.

Have you heard of homemakers being left alone to fend for themselves as children move out to live in different cities to seek employment? Apart, families, these days are more nuclear with grown-up children preferring to live apart from their aged parents just to get a taste of freedom. This leaves most homemakers financially drained and emotionally exhausted considering how they may have spent most of their lives’ earnings to bring up and educate their children. A life insurance plan is more like a silver lining for them. They can fall back upon the maturity amount, which is enough to pay for their living, medical or any other expenses. Greater coverage means that the homemaker has the much-needed amount to sail through the retirement phase of life quite smoothly.

Some women-centric policies come with add-on riders either for free or at very nominal costs. This helps as women are more prone to suffering from lifestyle diseases like cancer and so on. Having a sufficient cover amount frees them from the constraint of having to rely on their families for necessary medicinal support that can otherwise cause a dent in their savings.

Assessing coverage amount

It is difficult to assess the exact coverage requirement. However, homemakers can decide by gauging their estimated expenses after a certain period. Mathematically, they can opt for an amount equivalent to 50 per cent of the coverage amount that a working woman seeks. Homemakers may opt for unit-linked insurance plans that help them to earn returns in sync with the market while being backed by an insurance cover. An endowment policy would ensure a definite cover post-retirement, which would be enough to rely on.

Even a single woman, sans the responsibility of children and spouse, must buy life insurance. Buying insurance is the first step you take to ensure financial security in the long run. It is not about the money alone; it is more about ensuring peace of mind and financial independence.