You will rarely find anyone with an aversion to gold. Be the sheen of the yellow metal or its stability as an investment option for the long run, many investors prefer parking a percentage of their funds in gold investments. Apart from the inherent stability of gold as an investment option, many people also include it in their portfolio to diversify their investments in a way such that it beats the average inflation.

Apart, concerns of soaring inflation and imminent recession sparked by continued US interest rate hikes have forced many people to look for safe havens to park their money in the medium term. This is because businesses are likely to be affected owing to the higher cost of capital resulting in ramping the selling of stocks.

The recent market volatility from January 2022 shook many investors to the core as they saw their earnings in the past year being wiped off in merely five to six months. Even those investing through systematic investment plans (SIPs) cringed as they questioned the validity of investing in the stock market to create a corpus. In such a scenario, investing slowly and steadily in gold seems to be a viable option.

If you are still not sure why you must gold to ensure sustained growth in your portfolio, check how and why the yellow metal can help cool off the unwarranted heat and stress from the market.

Financial expertise is not required

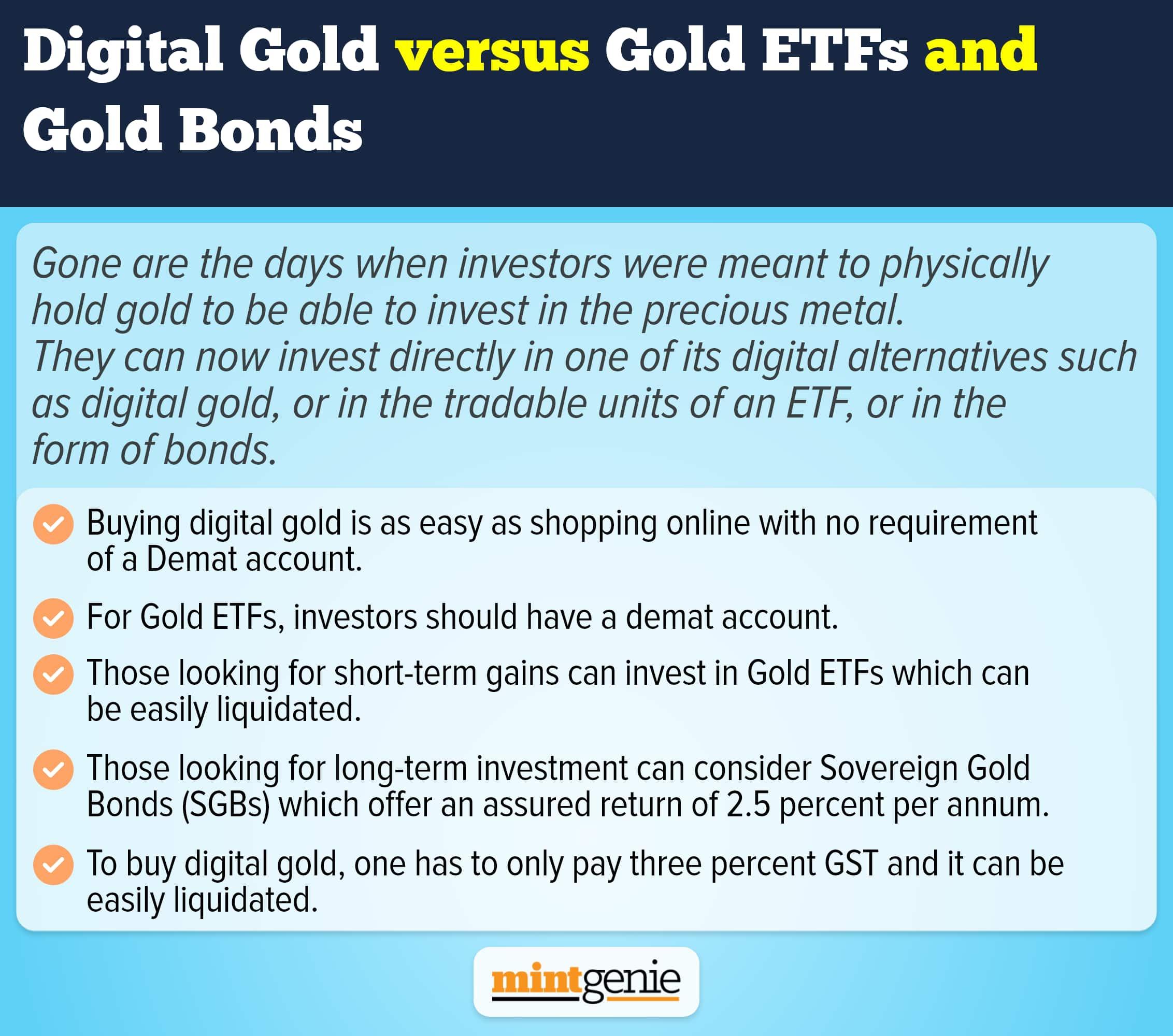

Unlike stocks and mutual funds, wherein you must account for various factors including price, valuation, expense ratio, returns rate over a period, portfolio turnover ratio, market capital, earnings, and more, investing in gold requires no such expertise. Gold as an investment has been in existence for aeons. The affinity for gold started with women buying jewellery during festivals and special occasions. The lack of liquidity coupled with the losses faced on non-retrieval of making charges prompted many to shift to paper gold.

Then, came gold exchange-traded funds (ETFs) that aimed to track the market price of gold to allow people to invest in small amounts. These being passive investments are relieved from the active management and interference by fund managers. These funds invest in gold bullion and are, therefore, based on gold prices, thus, allowing investors to decide their gold investments accordingly.

Gold mutual funds are also good, though you might want to be aware of the expense ratios involved. However, it is their high liquidity factor that attracts most investors.

Sovereign gold bonds (SGBs) are also an interesting way to keep your money parked though you must opt for them only when you wish to invest in a lump sum. Imagine that you have earned lump sum profits from a business or sale of a fixed asset. One way can be to park in some government bonds that will yield moderate but stable returns.

The other way out would be to put the money away in SGBs for at least eight years. Though the tenure of these bonds is eight years, you can opt for the encashment/redemption of the bond post completion of five years. Moreover, instead of going to the bank to mark your investments, you can simply sign up with your details on RBI Retail Direct which allows you to put money in SGBs from the comfort of your home.

Invest in small amounts

There are myriad benefits of parking money in digital gold formats like gold ETFs and gold mutual funds. One benefit is that you can invest in small amounts instead of waiting to accumulate a lump sum and then buy gold. Buying gold in very small amounts can be difficult considering how many gold retailer shops are apprehensive about selling this precious metal in such small quantities. The purity of the metal is again questionable. Gold ETFs, on the other hand, can be bought and sold in small amounts, thus, allowing you to trade with small amounts. The same holds for investments in gold mutual funds too.

Many apps including Google Pay, Paytm and PhonePe have enabled investments in digital gold. Irrespective of the financial situation, those interested in gold investments will always find a way out to put some money into them. With these apps, people can start investing in small amounts as low as Re 1 only. Apart, they can decide the frequency of investments too, which means that they put money on a daily, weekly, monthly, quarterly, half-yearly or yearly basis depending on their financial goals and how much money they wish to invest.

Though the investments may seem small, these add up over a period to allow you a lump sum. This money can be converted into a sizeable amount of gold or redeemed for massive returns.

The cost factor

Think of buying physical gold, and what strikes your mind is the additional expenses involved. These may be in the form of making charges and storage costs of keeping gold. Gold ETFs are way more efficient in this regard as one gets to buy and sell gold at the prevailing rates without any extra charges added up to the metal.

However, you must be willing to pay the demat account, trading account and other maintenance charges needed to invest in gold ETFs. If you already invest in shares, the charges on these would be automatically absorbed. However, the same may seem some added expense on you if you have opened a Demat and trading accounts exclusively for investing in gold ETFs.

B Padmanaban, Founder, Fortune Investment Services says, “Investing in gold ETFs is ok if you already have a Demat account. Just for the sake of investing in digital gold, there is no need to open Demat and trading accounts. If you do not have these accounts, putting money in a gold fund is ok, since there is not much difference in the returns earned.”

Gold is a strategic investment asset compared to most other investment options. When the market goes down or sideways, panicked investors rely on gold ETFs for diversification. Investing in gold ETFs or funds ensures an effective hedge against inflation and the downsides of a falling economy. Also, since gold is not listed among equity investments, investors are not subject to the extra Securities Transaction Tax (STT) that you must pay default on equities and equity-related products. This leaves you with more money for the redemption of gold ETFs or these funds.

Liquidity

Liquidity matters in all kinds of investments so that you may redeem them at ease as and when required. This is why you must rely more on gold ETFs while building up your investment portfolio. The primary benefit of putting money in digital gold is that you redeem your investments with just the click of a button as opposed to physical gold that you must carry to a reputed jeweller’s place to sell the same.

Since gold ETFs are traded on the exchange, the liquidity factor is embedded and inherent in the investments. Since there are market makers (authorized participants) to create liquidity, one benefits from hassle-free redemption. Just opt for gold ETFs with high transaction volume to ensure liquidity at all times.

Some analysts recommend putting money in gold mutual funds after factoring in the single category of costs involved apart from their liquid nature.

Consistency in returns

Are you aware of how much return gold investments have earned over the past seven years? Statistics underscore how gold yielded a CAGR of roughly 10 per cent since 2014. Compare this with most other investment options that have given erratic returns in the recent past and have suffered heavily under the effect of the Covid-19 pandemic.

Indian Rupee has been on a free fall for the past few months, thus, forcing many to shift their focus to foreign investments or indigenous gold investments. Those unaware of how to park their money in foreign stocks can put their money in gold as a reliable investment opportunity.

| Name of the gold ETF | CAGR (in %) | Three-year returns (in%) | Five-year returns (in%) | Seven-year returns (in%) |

| Kotak Gold ETF | 11.42 | 11.27 | 11.80 | 10.17 |

| Nippon India ETF Gold BeES | 10.63 | 11.04 | 11.61 | 10.11 |

| UTI Gold ETF | 10.61 | 10.80 | 11.57 | 10.11 |

| Quantum Gold Fund (G) | 9.31 | 11.05 | 11.63 | 10.06 |

| SBI Gold ETF | 8.94 | 11.32 | 11.75 | 10.16 |

| Source: NEGENPMS | ||||

The difference in tax benefits

Putting money in SGBs or gold ETFs has tax benefits too. The burden of taxation is most in physical gold investments. This is because when you buy physical gold including jewellery worth more than ₹2 lakh, you will not only have to pay one per cent tax deducted at source (TDS) plus three per cent GST on the value of gold. When you sell physical gold, you are subject to a flat 20 per cent tax rate plus a four per cent cess on long-term capital gains.

Gold ETFs are taxed differently. Moreover, the burden of taxation is far less. How much tax you must pay depends on whether the gains are of short-term or long-term nature. If you are redeeming your gold ETFs within three years, the short-term capital gains are added to your income and taxed as per the existing slab rates.

Holding these bonds for more than three years will amount to long-term capital gains, thus, subjecting you to a 20 percent tax on the earnings with indexation benefits. This means that if the value of gold goes up by 10 per cent every year while the inflation rate is 7 percent, then tax will be applicable only on three per cent of the profits earned. This is far less than what pays on physical gold, thus, explaining the need and urge to shift to digital gold.

SGBs are completely exempt from tax. This means that neither you need to pay anything upfront on purchase nor on the sale. Moreover, the investment is set aside for a prolonged tenure, thus, allowing you to benefit from massive returns generated on gold over a period. However, this helps only when you have enough money to invest and are ready to set aside this investment sans any urgency to sell it prior to the lock-in period. However, if you sell the SGBs before the redemption period, you will be subject to capital gains tax as per the prevailing income tax slab rates.

Viral Bhatt, Founder, Money Mantra says, “Both digital and physical gold have advantages and disadvantages. If you only want to buy gold for financial purposes, you can buy digital gold instead of physical gold. Digital gold, on the other hand, is unregulated and has a time limit on how long it can be kept in digital form. In certain instances, other digital investments such as sovereign gold bonds, gold mutual funds and gold ETFs may be preferable. On the other hand, physical gold is suitable for the personal use of investors but not for investment.”