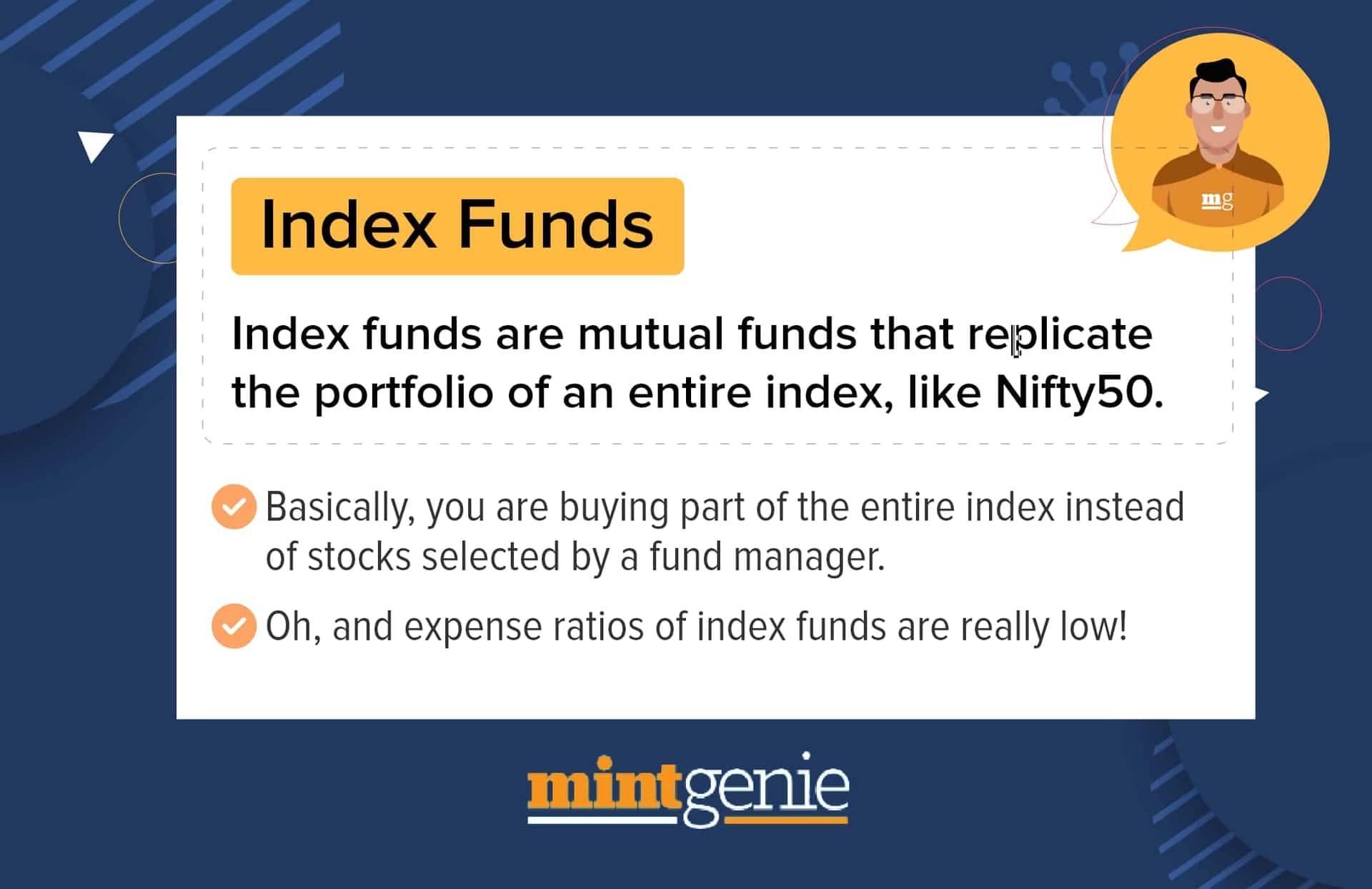

“Don’t look for the needle in the haystack, just buy the haystack,” quipped American investor John Bogle. This may probable be the best summation for Index Funds – funds that allow you exposure to pretty much the whole market.

But caveat emptor – an investor still needs to do some smart thinking rather than just buy it and forget it.

“By investing in an index fund of one’s choice, an investor is freed from research but gets the benefit of investing in a well-diversified portfolio of stocks at nominal cost,” says -Chintan Haria, Head - Product Development & Strategy, ICICI Prudential AMC.

READ MORE: New to investing? Here's why you should start with an index fund

For a retail investor, it can be challenging to invest in selective stocks and track their performances periodically.

Given that an index fund replicates an index, the returns generated will also mirror that of the index under consideration.

“Since there is no active investing required for managing index funds, the fund management cost is low which is beneficial for investors who are inclined towards low cost investing solutions,” explains Amar Ranu, Head - investment products & Advisory, Anand Rathi about the benefits of index funds to the retail investor.

“Another aspect of index funds that I like is the transparency,” says Omekeshwar Singh, Head, Rank MF. This is because the Index Fund will invest exactly in the companies that constitute that particular index.

Within the index funds universe, an investor must look at his/her investment priorities.

READ MORE: Why should you rebalance your portfolios using index funds?

“While broad based benchmark index funds can be considered for core portfolio, it would be optimal to have sector or thematic funds as a part of satellite portfolio,” suggests Haria. This is largely because sector or thematic funds have periods of outperformance or underperformance which can affect your portfolio disproportionately.

Also, your investment into an index fund may be more cost-effective than investment into an actively managed fund.

According to SEBI regulations, index funds' Total Expense Ratio (TER) ceilings cannot exceed one per cent (1%) of their total net assets, including investment and advisory expenses.

In contrast, depending on the AUM (assets under management) of the scheme, the TER for other schemes may go as high as two and a quarter per cent (2.25%).

“Typically, expense ratios for actively managed equity funds would be in the range of 0.65% to 1.5% for direct plans and 1.65% to 2.5% for regular plans,” says Dhaval Kapadia, Director – Managed Portfolios, Morningstar Investment Advisor India. Direct plan expense ratios for index funds would be in the range of 0.1% to 0.5% and slightly higher for regular plans.

READ MORE: Is the market fall the right time to invest in index funds?

Again, like their actively managed counterparts, index Funds allow participation via, both lumpsum and SIP (systematic investment plan) methods. However, experts advise the SIPs routes which would be a better approach (as opposed to lump sum) particularly for retail investors as it helps in building wealth in a disciplined way and avoids the vagaries of market timing.

Also, like all equity investment options go into index Funds with a long term objective. “The investment horizon for equity index funds would tend the same as that for actively managed funds, which is 5 years and above, as the underlying asset class remains the same,” advises Kapadia.

Other experts point out that you need to stay invested in the market over a long period of time so that market cycles even out and you can realise a profit.

But, now the cakewalk ends and the due diligence (for the retail investor) must start.

If an investor is bullish on a specific sector based on opportunities available, one can take an exposure to these sector specific funds. “But these investments come with higher risks and may not give you the desired return if the particular sector does not work,” says Ranu. Thus, an investor should be cautious of exposure in a sector specific fund.

“Index funds are still susceptible to the risk of tracking error,” says Abhinav Angirish, Founder, Investonline.in.

Tracking error refers to the degree to which the index fund deviates from its underlying index. A tracking error may occur in an index fund as a result of liquidity provisions, changes in index constituents, business activities, and other factors.

Index funds do not benefit from the expertise of the fund manager or the structured investment approach that an active fund manager provides. “At least in a country like India, where there are sufficient prospects for an alpha (profit), actively managed funds are expected to outperform index funds, which means that index funds will likely underperform,” says Angirish.

“For categories such as small & mid cap it may be advisable to consider actively managed funds as the potential for generating alpha via stock & sector selection is higher than in large caps,” says Kapadia.

READ MORE: ETFs vs Index Funds: Know the key differences before you invest

“Index funds have a lack of Reactive Ability (to market dynamics),” says Vinit Bolinjkar, Head of Research, Ventura Securities. Thus if a stock becomes overvalued, it actually starts to carry more weight in the index. This is just the point of time when astute investors would want to be lowering their portfolios' exposure to that stock.

Similarly while they may buy an index fund, they may have no control over the individual companies in the fund.

“Also, you can’t have exposure to various strategies,” says Bolinjkar.

Since index funds invest into index constituents, there is no alpha to be generated from this kind of investments. “You would just get the market return,” says Ranu, who advises that an investor pick a good (financial) advisor to pick a fund depending on the market scenarios.

At the end of the day, you must know your own (investment) priorities.

Because index funds replicate the performance of a market index, they are an effective tool for reducing risk. “They also have lower returns than other types of investments because their goal isn't just to make money but rather to provide stability over time,” emphasises Angirish.

Index funds and taxes

Long term and short-term capital gains are applicable in case of index funds. The rate of taxation depends upon the holding period. In case of equity-oriented index funds, if the holding period is less than 12 months, the gains are classified as short-term capital gains and if held for more than 12 months, the gains are classified as or long-term capital gains. Short-term capital gain is taxed at flat 15% while long-term capital gains above Rs.1 lakh is taxed at 10%, according to inputs shared by ICICI Pru AMC.

Compare and contrast

Experts advise against trying to compare index funds with actively managed counterparts.

“Any comparison of actively managed funds to index funds will inevitably involve cherry-picking, and I advise you should steer clear of it,” says Abhinav Angirish, Founder, Investonline.in.

Also do remember that index funds in India are a relatively new concept. Also, beyond the broader indices, there are very few passive funds in the mid and small cap categories that can be used as a benchmark.

Angirish suggests that one may use a rolling return outperformance consistency as a metric, where Active Funds have managed to beat index funds over the period of time.

Thus, If we compare SBI NIFTY index fund with HDFC Top 100 and Mirae Asset Large cap Fund, we find that from 2010, SBI NIFTY index fund has delivered a Minimum return of -1.93% in 5 years and 3.94% in 10 years period. The maximum returns for the same period were 17.79% and 14.34% respectively.

HDFC Top 100 has delivered minimum returns of -2.12% and 5.38% returns in the same period while maximum returns were 21.03% and 14.82% respectively.

Mirae Asset Large Cap Fund delivered minimum returns of 1.17% and 9.22% while maximum returns were 25.54% and 18.90% respectively.

“Clearly, active funds have outsmarted index fund in the long run” says Angirish.

“The mandate of an index fund limits the possibility of alpha (read profit) generation,” points out Chintan Haria, Head - Product Development & Strategy, ICICI Prudential AMC.

“Active investing when done with proper due diligence and discipline is bound to beat index investing in the long run as change in composition of index is normally with a lag,” points out Vinit Bolinjkar, Head of Research, Ventura Securities.

Index funds and other asset classes

Index funds are available for other asset classes, outside equity too.

“Yes, index funds are available for other asset classes including debt and gold,” Dhaval Kapadia, Director – Managed Portfolios, Morningstar Investment Advisor India.

Recently, AMCs have been launching target maturity funds which track an index with specific securities such as 5-year government bonds or a mix of corporate bonds and state government securities.

These are passively managed funds at low costs, which help investors benefit from higher yields on specific bonds on the yield curve for various maturities.

Gold ETFs and fund of funds which invest into the ETF are also available. These are low cost, liquid and provide an investment which passively tracks the price of gold.

Manik Kumar Malakar is a personal finance writer.