Getting diagnosed with cancer is nothing short of a nightmare. Add to it the gradual and sustained changes in our lifestyle habits that have increased the chances of suffering from cancer manifold. Studies by the World Health Organization point towards the increasing ubiquity of cancer.

With an increasing number of people getting detected for myriad types of cancer each day, the risk of falling victim to cancer is equal for both men and women. The Union for International Cancer Control designed the fourth of February each year as “World Cancer Day” to raise worldwide attention towards cancer and call for collective action towards a cancer-free society.

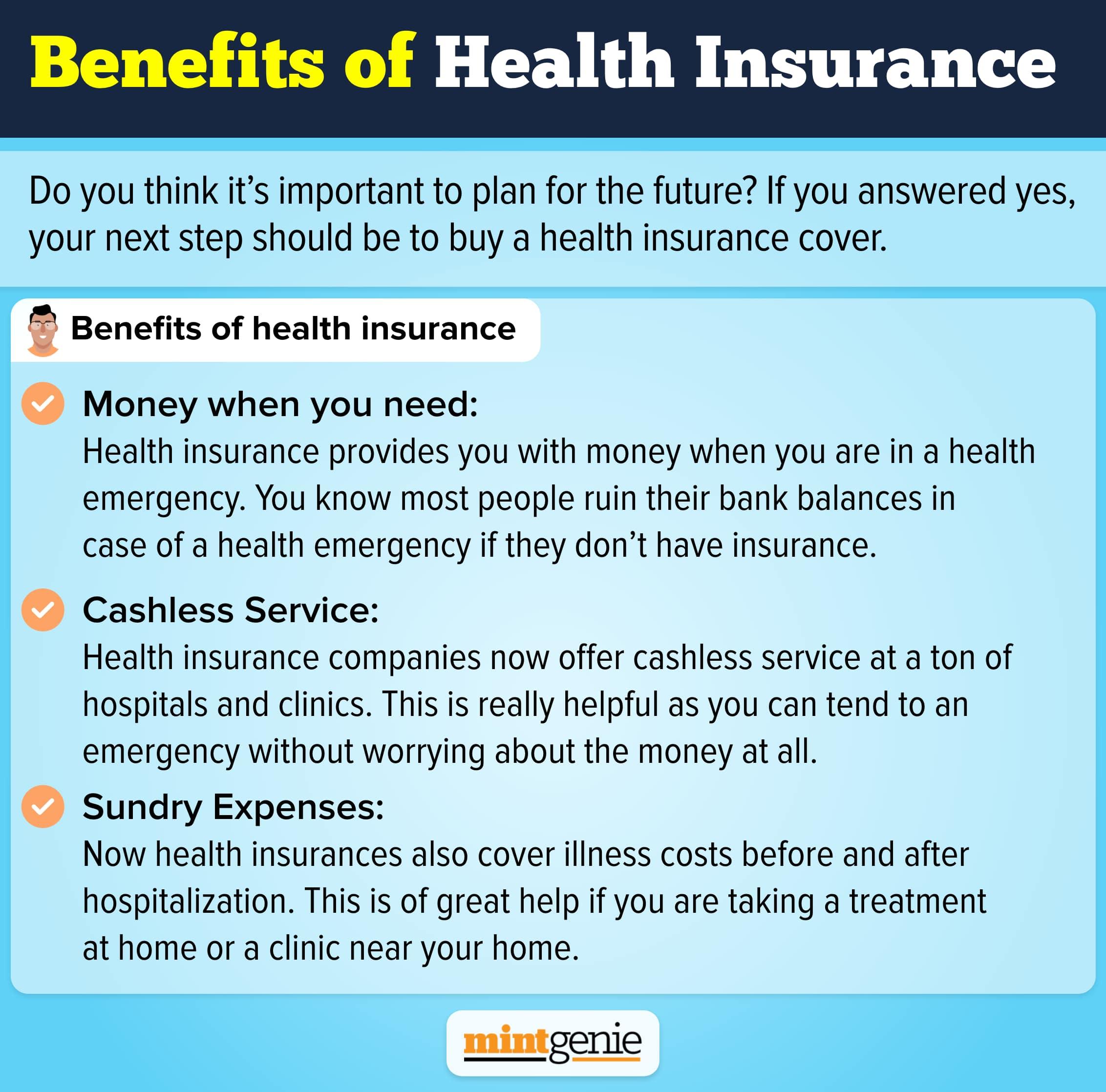

Treatment of cancer being exorbitantly high can make a dent in your savings. With the pervasiveness of cancer getting higher every day, it makes sense to have a cover in place that can cover the expenses of hospitalization and subsequent treatment while paying for post-hospice charges too.

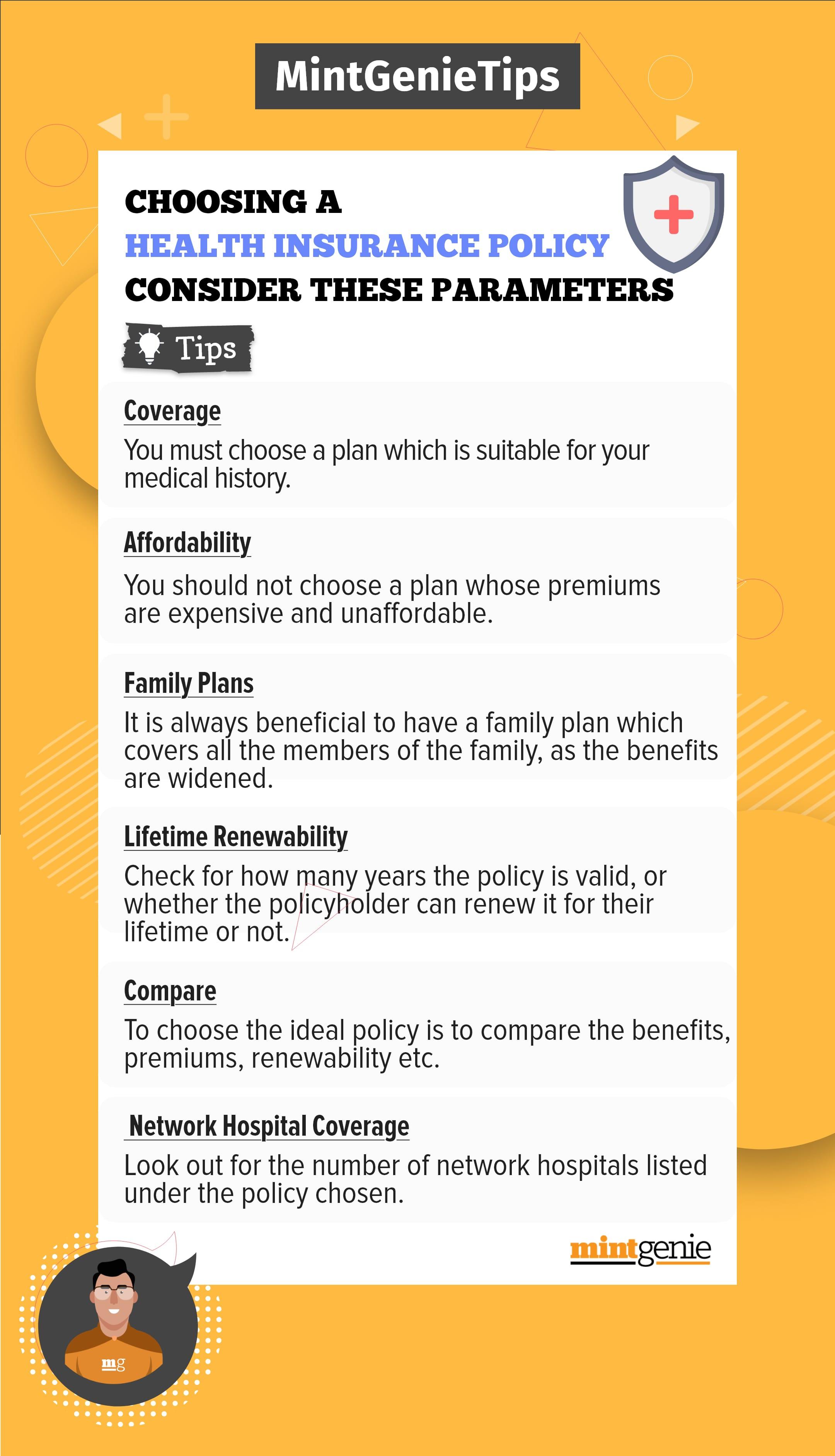

Before buying a health insurance plan, it is imperative to check for the list of diseases covered under health insurance as many policies may exclude chronic illnesses like cancer without your knowing. This may leave you bereft of the necessary money needed to treat diseases like cancer.

Also, opting for a major health insurance policy that covers all major critical illnesses including cancer may not suffice as it may pay only for inpatient hospitalization and for treatment at its network hospitals across the country. Besides, the policy amount may not be enough to cover the entire treatment cost, especially, for many people who seek a cover as low as ₹5 lakh under the misconception that cancer affects only the luckless and unfortunate.

Why buy a cancer insurance policy?

The effect of having comprehensive health insurance to secure the entire family against multiple health problems is however limited owing to the various sub-limits on the amount payable at different stages of payment. This restricts from getting full benefits from buying and relying on a comprehensive health plan for the treatment of a critical illness like cancer.

This explains the need to buy a critical illness benefit cover that covers a host of serious ailments including cancer that may not be otherwise covered under a simple health plan. Better, if you buy a cancer insurance policy directed towards payment for treatment of cancer alone. This is a more viable option at greater risk of suffering from cancer owing to hereditary causes or prior history of cancer.

Simply speaking, comprehensive care insurance plans cover most kinds of cancer, affecting both men and women, at both early and advanced stages. These plans are designed to alleviate the costs of cancer treatment while also providing the policyholders with necessary financial support.

Dedicated cancer care insurance plans are essentially special critical illness insurance policies that hand out a lump sum amount to the policyholder on diagnosis of cancer. These cancer protection plans are defined benefit plans that hand out a fixed benefit to the policyholders irrespective of whether they are diagnosed with early or malignant stage cancer during the policy period.

Apart, cancer special policies lend an added advantage over others as they waive off payment of further premiums on the policyholders being diagnosed with early stages of cancer. With inflation having an augmenting effect on treatment expenses too, some critical illness covers designed to cover cancer treatment alone have an in-built provision of increased sum assured by a specific percentage every year in case of no claims made.

If the sum assured is more than ₹10 lac, some insurers also announce discounts on premiums to encourage people to buy insurance policies with a higher cover amount. Since these plans cover only cancer treatment expenses, the premiums charged on them are much lower than what one has to pay towards a comprehensive health insurance policy.

Some exclusive cancer care insurance products available in the market include Cancer Care Plus, HDFC Life Cancer Care, Cancer Insurance Plans, LIC Cancer Cover, Max Life Cancer Insurance Plan, SBI Sampoorna Cancer Suraksha and more. Most cancer care plans cover all kinds of cancer including breast cancer, ovary cancer, lung cancer, stomach cancer, hypopharynx cancer and prostate cancer, though in most cases skin cancer may be excluded that you must check before buying.

Exclusions in cancer insurance policies

You must check for the types of cancer disorders covered under the cancer protection cover you are looking to buy. This is because many insurance companies tend to exclude treatment of cancer problems like skin cancer, which means that you may not be able to claim the cover amount even after having bought the policy. Apart, the insurance company may refuse to release the benefit amount to the policyholder if he or she is diagnosed with cancer from the following conditions.

- Cancer during treatment of sexually transmitted diseases like HIV or AIDS.

- Cancer due to congenital conditions or birth defects.

- Cancer due to inebriation by alcohol or drugs

- Cancer due to contamination, be it nuclear, biological or chemical.

- Cancer suffered due to organ offer and acceptance.

These exclusions are over and above the fact that the insurance company is not liable to cover towards treatment of pre-existing cancer problems.

Take note of waiting and survival periods

While added features and benefits of having a higher cover advocate the buying and inclusion of cancer care policies during financial planning, there are certain limitations that you must be aware of. You must be mindful of the initial waiting and survival periods before making any claims.

The policyholders cannot make any claims during the initial waiting period typically ranging between three and six months from the date of policy inception. The survival period wherein the insured must survive for a specific number of days from the first diagnosis of cancer generally lasts between 30 days and six months.