Heart attacks and cardiac arrest are on the rise amongst the youngsters in India with almost 25% of cases under 40 years, not sparing those between 20 to 30 years of age as well. According to the World Health Organisation, about 18 million people die due to cardiovascular conditions every year, leading to 32 percent of all deaths globally. These alarming figures call for an urgency to maintain a healthy lifestyle to avoid situations that can lead to severe heart conditions.

Constant stress could increase your risk of heart and circulatory disease, as it has been linked to higher activity in an area of the brain linked to processing emotions, and an increased likelihood of developing heart and circulatory disease. The leading causes of cardiovascular diseases are poor dietary practices, smoking and lack of active lifestyle.

Cholesterol, Obesity and High blood pressure are the most common health conditions which lead to cardiovascular diseases. Ignorance of symptoms and disinterest on the part of the patient or family are also causing a delay in getting evidence-based treatment.

Hence, it has become crucial to take a moment, pause and contemplate how to take good care of yourself and your heart. On a day that has been earmarked to emphasise the importance of this vital organ, resolve to protect it. Also, while one ensures to take better care of heart and health, one should be prepared for the uncertainties that can hit anytime which means ensuring good financial health considering the high cost of treatment for cardiovascular diseases. Regular medical indemnity plans may not be sufficient during such medical emergencies as it is more than just hospitalisation expenses to worry about.

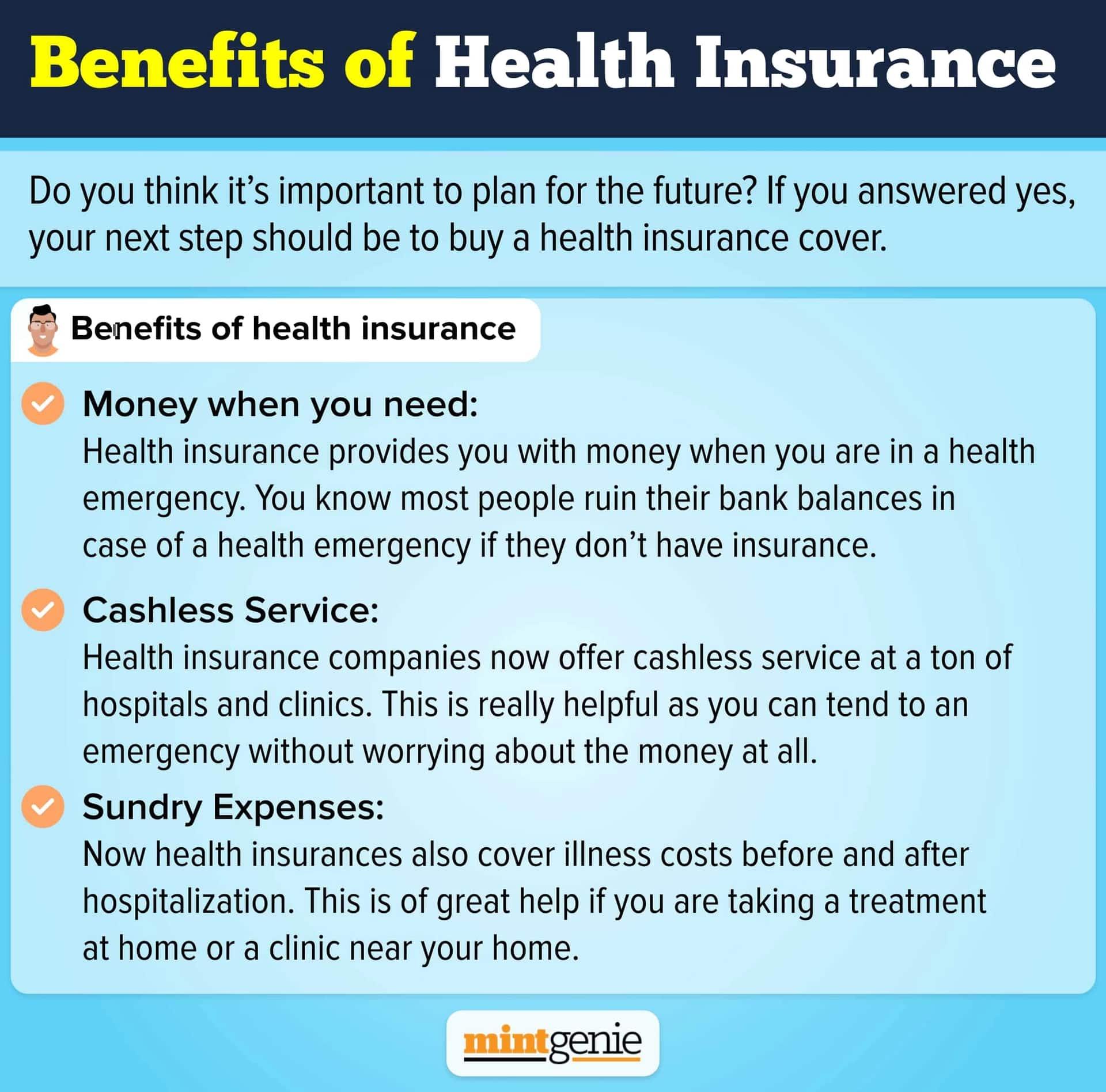

Critical illnesses require prolonged treatment even after the patient is discharged from the hospital and could include expenses like medicines and other miscellaneous expenditure. The most cost-effective way to ensure your peace of mind during such a situation is to have a fixed benefit critical illness policy or a fixed benefit critical illness rider with your existing term plan. This will ensure any unexpected medical emergency does not drain an individual financially.

The efficiency of critical illness riders/policies:

The critical illness and disability rider/policy creates a financial shield against a large number of listed critical illnesses, including life-threatening diseases such as cancer, heart attack, and stroke, among others, as per the rider's terms. These products ensure that the life insured gets a lump-sum payment if diagnosed with a critical illness. Such an amount can help pay for the cost of care and treatment for specific illnesses and recuperation expenses.

How to choose the right critical illness rider/policy?

The insurance market offers different types of insurance plans, including critical illness riders/plans. Hence you should know how to choose the best critical illness rider/plan for yourself. Below are some features to look for in a critical illness rider/plan:

Number of health conditions covered

The first thing one needs to check is the number of critical diseases and conditions covered under the rider/plan. For example, different critical illness riders / plans by different life insurance companies may offer cover against about 15 to 40 illnesses and health conditions.

Amount of cover you need

An essential aspect of any coverage is to select the right amount. It is important when you are buying term insurance with a critical illness rider. Ideally, critical illness cover should range from 30% to 50% of your term life cover.

Waiting period

All health insurance policies/riders have a clause for a waiting period before they start covering specific diseases. Critical illness policies have a waiting period of up to 180 days for covering a new diagnosis. Any illness diagnosed typically within 48 months prior to the policy start date falls into a pre-existing disease bucket and may not be covered by the policy unless already disclosed.

Maximum age of coverage

Different insurance companies have different age limits up to which you can continue critical illness insurance. Hence, do check the maximum age for coverage even while buying term insurance with critical illness cover.

In case of emergencies or in situations where an individual is dealing with a cash crunch, one should purchase a dedicated critical illness policy. This World Heart Day, purchase a critical illness policy to protect your heart and make healthy choices for your heart.

Akshay Dhand, Appointed Actuary, Canara HSBC Life Insurance.