Q. I am a 45-year-old working professional. I wish to open a fixed deposit account (FD), but I am confused between the multiple options available in relation to FDs, such as tax saver FD, regular FD, recurring-FD, corporate FD, etc. Which category of FD is suitable for a period of five years?

-Sanjay Dadhich, Jhansi

Investment in fixed deposits has been historically one of the most popular investment options amongst Indians. With time, new categories of FDs have been introduced by banks and NBFCs. The popularity of FDs does not seem to be declining inspite of the emergence of investment options such as mutual funds, unit-linked insurance policies, cryptocurrencies, etc.

Before understanding which particular FD will be suitable for the purposes of a five-year period, let us first discuss the most popular categories of fixed deposits.

Regular Fixed Deposits

The investor places his money in the Regular FD account for a set period of time, typically ranging from 7 days to 10 years. The fixed and predetermined interest rate is higher than the interest rate on a regular savings account. Loan and overdraft facilities are available in exchange for standard FDs. You can also withdraw your funds before the account matures, but you will be penalized for doing so.

Flexi Fixed Deposits

These FDs incorporate the convenience and flexibility of a savings account with the consistency of a Regular Fixed Deposit. In a Flexi Fixed Deposit, your savings are 'swept-in' to an FD above a pre-determined threshold. Funds that are below the pre-determined threshold still earn interest at the savings account interest rate. If there is a debit from the account and the savings account balance is not sufficient to meet the demand, then funds can be automatically 'swept-out' of the Flexi FD basis ‘last-in and first out’ system to meet the needs, and the remaining funds continue to earn interest.

The Flexi FD combines the features and benefits of FDs and savings accounts, so you get the higher interest rates of FDs as well as the liquidity of savings accounts.

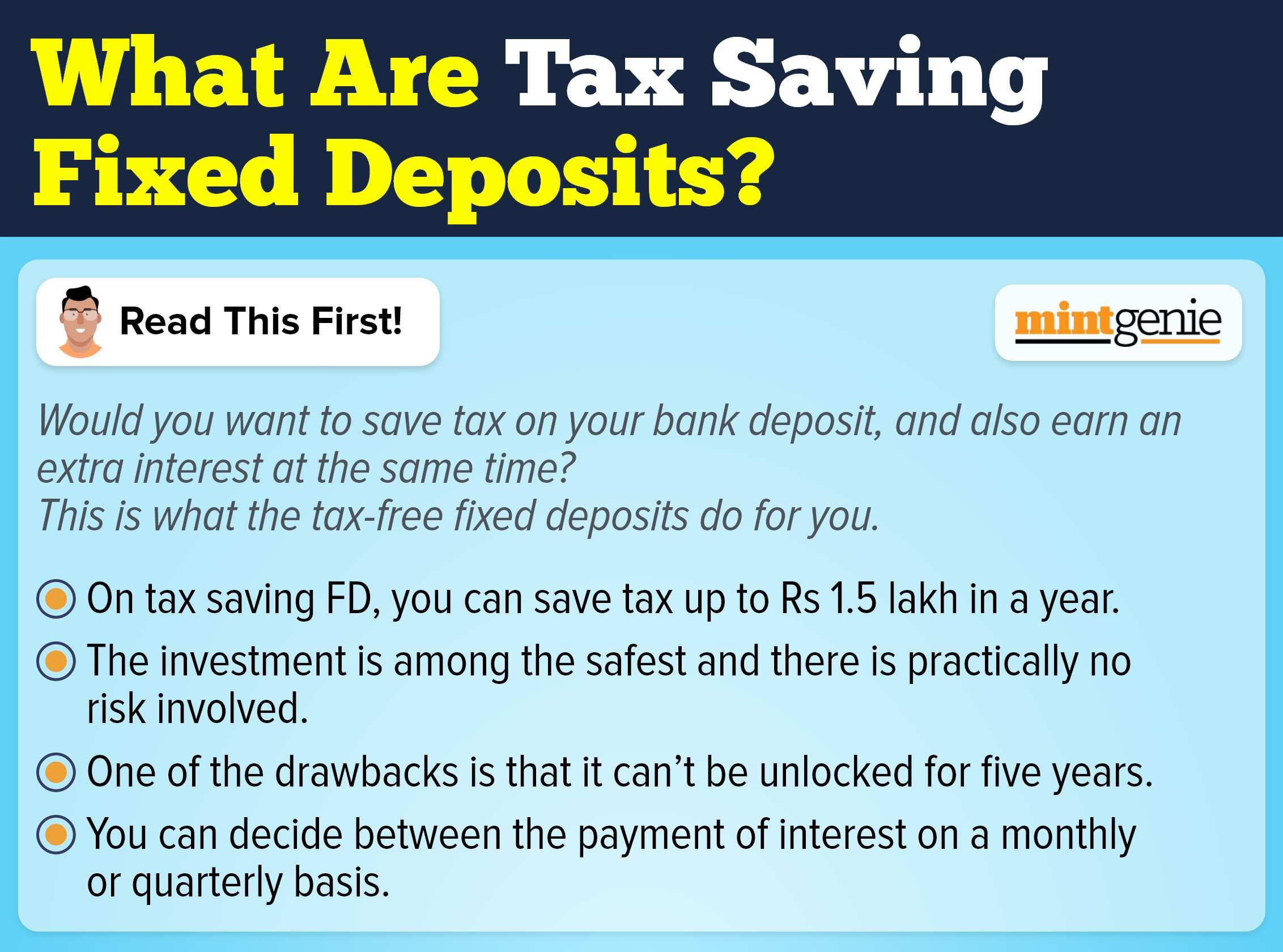

Tax Saving Fixed Deposits

Tax-Saving FDs have a mandatory five-year minimum mandatory lock-in period, so you cannot withdraw your money before five years. Furthermore, loan and overdraft facilities are not available in conjunction with tax-saving FDs. However, under Section 80C of the Income Tax Act, 1961, you can claim tax exemptions of up to ₹1.5 lakh.

Fixed Deposits for Senior Citizens

These are for people over the age of 60. They provide higher interest rates than traditional FDs. The length of stay here can range from 10 days to 10 years. Senior Citizen FD can be tax-saver or regular, but in both scenarios it will offer higher interest than a non-senior citizen fixed deposit of similar nature.

Cumulative Fixed Deposits

These FDs allow you to choose the interval at which interest is compounded. The interest is added on to the amount you invested and is paid when the FD matures.

Non-Cumulative Fixed Deposits

In the case of a non-cumulative fixed deposit, the interest is not reinvested but is paid out to the account holder periodically. It is a good investment for people who want a sustained income from interest.

Corporate Fixed Deposits

Corporate Fixed Deposits are typically offered by finance companies classified by the Reserve Bank of India as Non-Banking Finance Companies (NBFCs). They generally offer an interest rate which is higher than that offered by banks. However, there is a risk-reward trade-off. Fixed deposits offered by banks typically have better credit ratings than the credit ratings of NBFC’s FDs.

Please note that all the categories mentioned above may overlap with each other. A Corporate Fixed Deposit may also be cumulative and also be tax-saving at the same time.

For a time period of five years, the most suitable fixed deposit would be the tax-saver fixed deposit, since, apart from offering high-interest rates, it will also offer you tax savings in form of income tax exemption. Income upto ₹1.5 lakhs is deductible from taxable income if the same is invested in a tax-saver fixed deposit.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.