Q. I am a 24-year-old businessman. I am confused between various retirement/pension schemes available in the market. I am self-employed and I wish to invest in the investment option having minimal risk.

-Ajay Polysetti, Visakhapatnam

Self-employed individuals have to be very cautious about retirement planning since they do not get any pension from the government or from any other source. Some of the most popular long-term investment options which can help you in securing a stable income/pension for your retirement are:

National Pension Scheme, Public Provident Fund and Retirement Mutual Funds. Self-employed individuals cannot invest in another very popular retirement scheme - Employee Provident Fund.

Before understanding which particular retirement scheme will involve minimal risk, let us first understand the features of all three options.

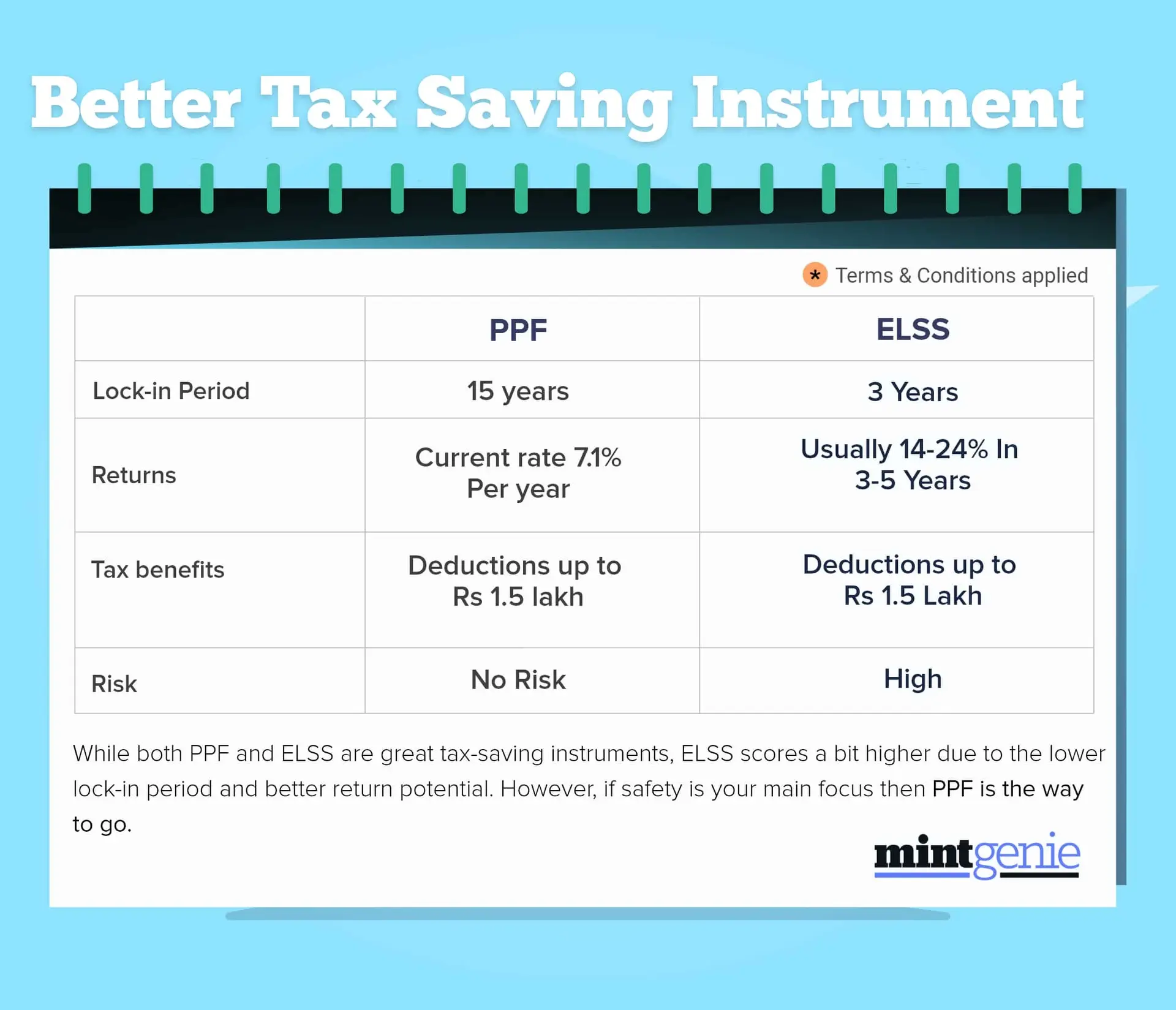

Public Provident Fund (PPF)

Introduced in 1968, the sole aim of this scheme was to offer investors a way to save money and grow their wealth over time with high returns. The Public Provident Fund (PPF) is backed by the Government of India. It is therefore one of the most secure investment solutions available to individuals.

An individual can open a PPF account with as little as Rs. 100. In a year, the minimum investment amount is Rs. 500 and the maximum investment per annum is Rs. 1,50,000.

This contribution limit applies to both minors and adults. You can make a maximum of 12 contributions annually. The maximum amount that can be invested in PPF is up to ₹1.5 lakh per year and the interest earned on it is tax-free. The total tenure for a PPF account is 15 years. After that, one can extend it for five years at a time. Investors can avail of a loan against their PPF account. With PPF, you’re allowed to avail a loan against your PPF account from the 3rd to 6th year of the PPF account's opening. The current rate of interest being offered by PPF is 7.1% compounded yearly.

Retirement Funds - Mutual Funds

Financial independence after retirement is one of the most sought-after goals among millions of investors. Many Asset Management Companies (AMCs) in India have floated plans specifically to respond to the needs of retirement planning, they are classified as ‘Solution-Oriented Retirement Fund.’

A Solution-Oriented Retirement Fund is an open-ended mutual fund with a lock-in period of five years or the retirement age whichever is earlier. Currently, as on 19 July, 2022 India’s best performing Solution Oriented Retirement Fund is HDFC Retirement Savings Fund - Equity Plan basis 5 year Compound Annual Growth Rate (13.85%).

National Pension Scheme (NPS)

The NPS scheme is a retirement benefit programme established by the Government of India to provide all subscribers with a steady income after retirement. It is governed by the PFRDA (Pension Fund Regulatory and Development Authority). The NPS scheme aims to help people develop the habit of saving for their retirement. It is an attempt by the government to find a long-term way to make sure that every Indian has enough money saved up before they retire.

The two account categories that NPS offers are Tier-I and Tier-II. The pension account with limited withdrawal facilities is known as a Tier-I account. The Tier-II account is a voluntary account that offers liquidity for investments and withdrawals. It is allowed only if the subscriber has a Tier-I account that is active.

In NPS, Tier-I users can receive up to 60% of their corpus as a lump sum at retirement, which is completely tax-free. Even the remaining 40% can be tax-free if it is used to purchase an annuity plan (it is tax-free if purchased from an empanelled insurance provider). The remaining amount needs to be placed in an annuity that will provide consistent income for the remainder of one’s life. Even though the income from the annuity is taxable at the relevant slab rate, this sum is excluded from taxes.

Investments in both NPS and Solution Oriented Mutual Funds do not guarantee any kind of return. Investments in both are subject to market risk. For a person with a low-risk appetite, PPF is the most preferable option because of the stable as well as guaranteed nature of returns offered by PPF.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.