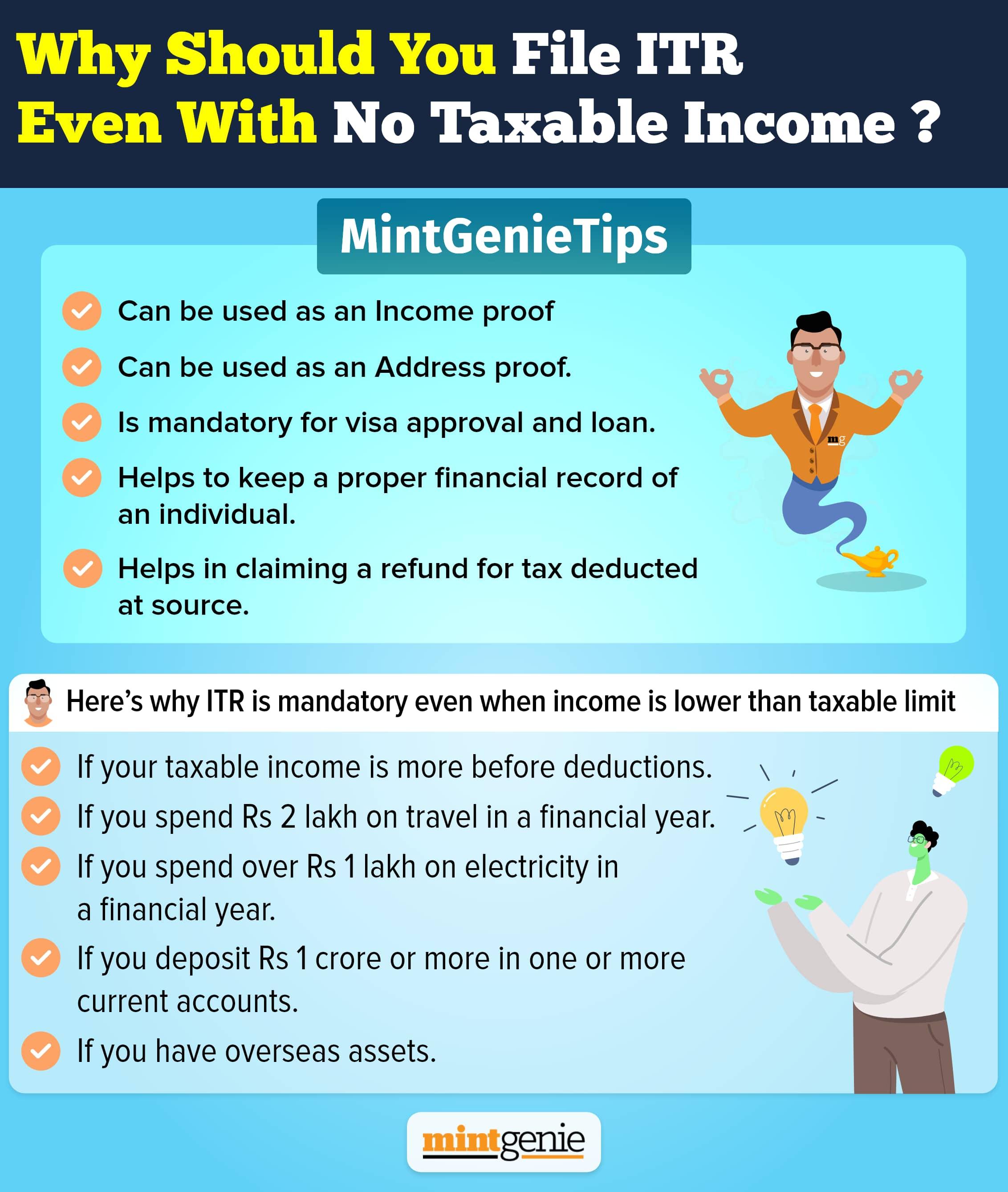

Q. I have recently graduated from NIT, and have joined one of the top automakers in India. I will be filing my first income tax return next year. I am utterly confused about the old and the new tax regimes and which one is more beneficial for a person who has just started earning and has a salary below ₹15 Lakhs. Presently, I am investing in NPS to avail tax breaks under Section 80 C of the Income Tax Act, please let me know if tax exemption is available under both the old and new tax regimes.

D Prabhat, Chennai, Tamil Nadu

Many first-time taxpayers are not aware of the fact but there are two income tax regimes which are concurrently running in India at present and a tax-payer can opt for either one at the time of filing his income tax return.

Ms. Nirmala Sitharaman, India’s current Finance Minister, announced in the budget 2020 a new tax system with more tax slabs and more importantly lower tax rates. Most Indians wanted this for a long time, but it came with a serious catch - nearly all the deductions and exemptions that were available under the old tax regime were taken away. To make things even more confusing, the Finance Minister gave taxpayers a choice between the new regime and the one that was already in place. It is now up to them to choose which regime they want to file their taxes under.

Old tax regime

Under the old regime of taxation, the assessee may claim deductions, exemptions, and allowances that enabled them to properly plan their taxes and save money. The old tax regime is complex and provides many loopholes or exemptions using which one can reduce his/her tax liability considerably.

Through the addition/amendment of various sections to the Income Tax Act, over the years, the government has granted around 70 exclusions and deductions to Indian tax residents, allowing them to reduce their net taxable income and consequently allowing them to reduce their tax liability.

These deductions permit you to reduce your tax liability by investing, saving, or spending on particular items. Section 80C is the most popular and substantial deduction, allowing you to deduct up to Rs. 1.5 lakh from your taxable income.

Deductions and exemptions under old tax regime

Exemptions

- House rent allowance

- Leave travel allowance

- Mobile and internet reimbursement

- Food coupons or vouchers

- Company leased car

- Uniform allowance

- Leave Encashment (at the time of resignation/retirement)

Deduction

- Equity linked savings scheme (ELSS)

- Employee provident fund

- Public provident fund

- Children's tuition fees

- Health insurance premiums

- Investment in NPS

- Life insurance premium

- Principal and interest component of home loan

- Tuition fee for children

- Saving account interest

Benefits of opting for the old tax regime

- The old tax regime encouraged individuals to save for events which may cost them a huge amount of money like, higher education, the purchase of a home, or medical expenditure/ investing for these events was encouraged under the previous tax regime by providing taxpayers tax-breaks when they availed: house loan, education loan, health insurance, etc.

- The old tax system instilled in individuals the habit of saving, which is extremely useful in times of emergency. With the advent of the new tax system, saving rates are likely to decline, as many individuals anticipate opting for the new tax system.

Cons of opting the old tax regime

- Under the previous tax structure, investors were in a way compelled to invest in the prescribed tax-saving instruments regardless of performance if tax saving was the priority on their mind.

New tax regime

There are six tax brackets, each with a reduced tax rate for incomes up to Rs. 15 lakhs. Multiple exemptions and deductions which were available in the old regime are not available in the new regime.

Key highlights of the new tax regime

- According to the new tax regime, individuals with a total income between Rs. 5 lakhs and Rs. 7.50 lakhs must pay 10% tax on their income above INR 5 Lakh + INR 12,500.

- According to the new tax regime, those earning between 7.5 lakhs and 10 lakhs will be required to pay 15% tax on their income above INR 7.5 Lakh + INR 37,500.

- According to the new tax regime, those earning between 10 and 12.5 lakhs pay 20% tax on their income above INR 10 Lakh + INR 75,000.

- Individuals earning between 12.5 lakhs and 15 lakhs are required to pay 25% tax on their total income above INR 12.5 Lakh + INR 1,25,000.

- According to the new tax regime, persons with an annual income in excess of Rs. 15 lakhs pay 30% of their total income above INR 15 Lakh + INR 1,87,000.

Before opting for the new tax regime, individuals must do a detailed comparison of the old and new tax regimes based on the aforementioned tax brackets. Numerous aspects, which will be discussed below, shed light on the distinct benefits of both tax regimes.

Features of new tax regime

Lower tax rates

The new tax regime has expanded the scope of tax arbitrage by instituting seven tax brackets with tax rates ranging from 0% to 30%, with the highest tax rate applied to incomes above INR 15 lakh. In contrast to the current regime, the former regime had four tax brackets ranging from 0% to 30%, with the highest rate applicable to incomes exceeding INR 10 lakh.

Deduction and Exemption

The government is aware that the Act's numerous exemptions and deductions make compliance by taxpayers and implementation of tax rules by tax authorities arduous.

To provide relief to taxpayers, the simplified tax rate system necessitates foregoing certain tax deductions and exemptions. Therefore, it is essential to compare the impact of claimed deductions/exemptions against the advantage of lower tax rates. Among the popular tax exemptions and deductions that are no longer permitted under the new tax regime are:

- Leave Travel allowance

- House Rent allowance

- Children Education Allowance

- Standard deduction on Salary

- Deduction for Professional tax

- Interest on housing Loan

- Deduction under Section 80C of Income Tax Act

Pros of opting the new tax regime

- The new tax system lowers tax rates. Although the new tax regime features lower tax rates, the majority of deductions and exemptions that were previously accessible are no longer available. With the advent of the new tax regime, individuals are required to fill out less paperwork, and the tax filing procedure has been simplified.

- With the implementation of the new tax system, liquidity will improve, and reduced tax rates will provide individual taxpayers with greater disposable money. This would be advantageous for individuals who were previously unable to invest in particular instruments owing to higher tax rates which used to eat into their disposable income.

- The new tax structure provides greater investment customization options. As stated in the regulation, taxpayers will only be eligible for deductions if they invest in one of the specified instruments. This will limit the investment options available to taxpayers, but will also offer them a great deal of freedom to tailor their investment decisions.

Cons of opting for the new tax regime

With the implementation of the new tax system, several deductions are no longer available to taxpayers, including those listed below:

- Deductions for travel time off

- Deductions for rent allowances on the home

- Numerous special allowances, including the education allowance for children, the hostel allowance, and the uniform allowance, will no longer be subject to deductions.

- No deductions are made from MP/MLA allowances.

- No deductions would be allowed for deductions under sections 35AD or 35CCC.

- Subtractions under the family pension plan

Income tax slab rates under both regimes

| Income Tax Slab (Rs) | Old Tax Rates | New Tax Rates |

| 0 - 2,50,000 | 0% | 0% |

| 2,50,000 - 5,00,000 | 5% | 5% |

| 5,00,000 - 7,50,000 | 20% | 10% |

| 7,50,000 - 10,00,000 | 20% | 15% |

| 10,00,000 - 12,50,000 | 30% | 20% |

| 12,50,000 - 15,00,000 | 30% | 25% |

| 15,00,000 & above | 30% | 30% |

Old vs new tax regime – Which is better?

It may seem that the new tax regime is more benevolent, however, a financially literate taxpayer can avail various tax exemptions available under the old tax regime and save a higher amount of his income. Many important deductions, such as tax exemptions under Section 80 C of the Income Tax Act are not available under the new tax regime. For people confused between the two tax regimes, it is best to consult a chartered accountant or a tax advisor before deciding between the two regimes.

Kuvera is a free direct mutual fund investing platform.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.