Q1. I'm a 25 yo product manager working at a software company. I’m planning to buy a health cover for my parents. My father has type 2 diabetes, my mother has no severe issues as such. I was thinking of getting a floater policy. What are my options?

-Joy D'Souza, Goa

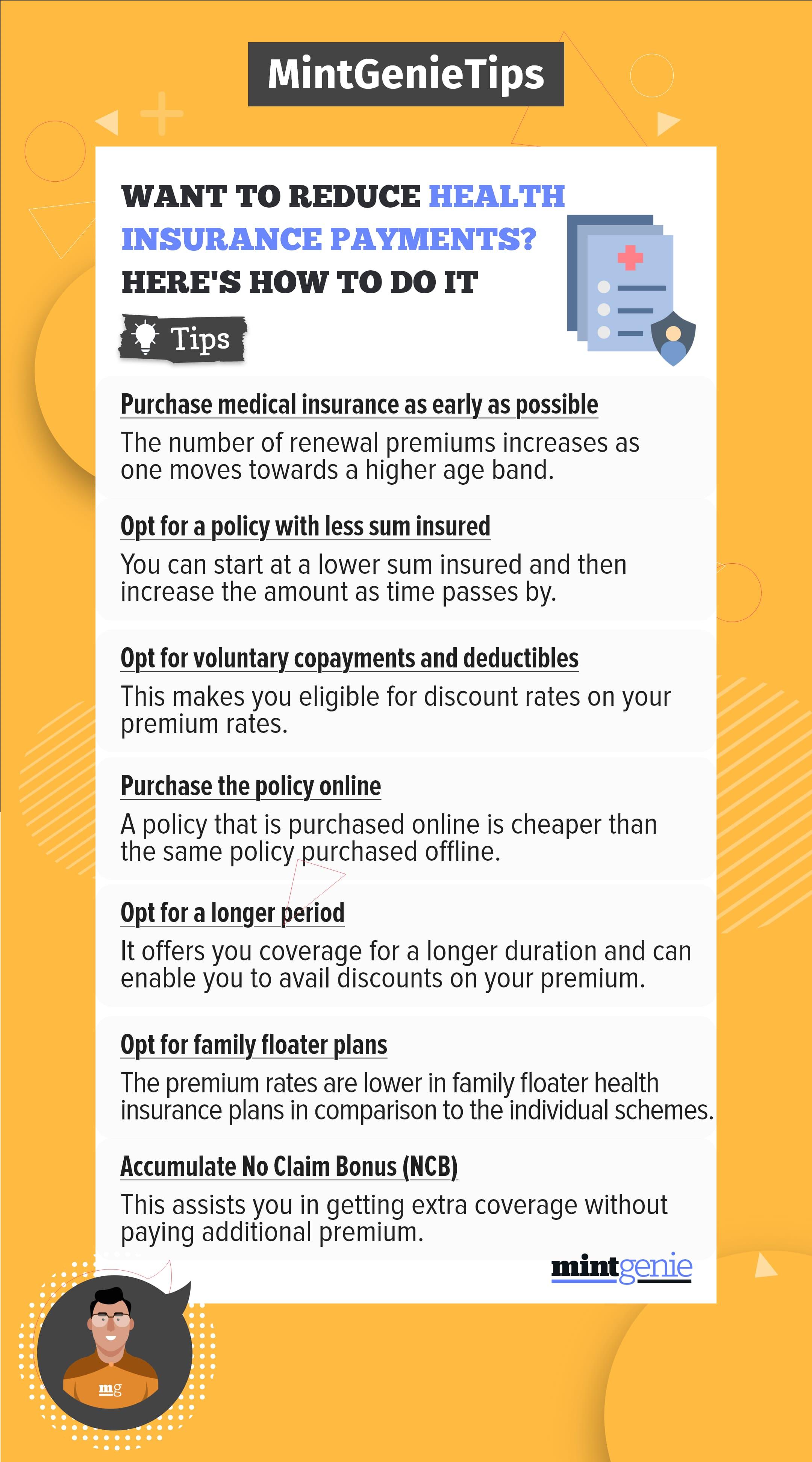

If you do a little more research, you’d realize that most standard health policies do not cover pre-existing diseases like diabetes or the complications arising from it. There are special policies that cover diabetic people on an individual or family floater basis, but they consider an additional premium. So you might as well explore the option of getting separate covers for your parents. Especially if your parents are senior citizens, avoid family floaters.

1. Before going ahead, make a list of all the pre-existing diseases specific to the person being insured and factor in the waiting period for those specific diseases.

2. Avoid Co-pay. Many policies nowadays offer low premiums with a co-payment clause, and you don’t realize it until an unfortunate event happens and you are asked to make partial payments for it.

3. Check if the coverage includes benefits like medicines, diagnostic tests, and doctors’ consultation fees.

4. Remember that your company’s group health cover is not enough.

5. Avoid policies with caps on room rent.

6. Additionally, some policies also provide a cumulative bonus for every claim-free year. So your SI (Sum Insured) increases with the renewal of the policy.

Now, how do you decide how much coverage you need?

Consider a few things before deciding on the coverage:

1. LifeStage: The cover should be sufficient to accommodate natural additions if any. Say if you decide to get one for yourself or your spouse later. You can increase the cover subject to the insurer’s approval.

2. Inflation: A routine procedure costing ₹1L today will cost ₹20L more after 15Y. A cover that seems sufficient today will become inadequate with rising costs.

3. Lifestyle: A knee replacement cost will vary from Govt to a private hospital. One should check the average price of a room in their preferred hospital. Hospital charges are anchored based on the room a patient takes.

There is no ideal health cover, but generally, most advisors consider:

1. Health cover should be at least 50% of your annual income.

2. Coverage should be able to cover the cost of a Heart transplant in a hospital of your choice. Usually costs ₹5-8 lakh.

Remember to ask as many questions as you can think and compare your options before going ahead.

READ MORE: Why health insurance is a necessity for young mothers

Q2. I’m a 30 yo homemaker. I ended up saving some petty cash every month and thought of saving it somewhere more profitable but easy to withdraw in case of emergencies. A friend suggested opening a recurring deposit over FD for flexibility. Can you help me understand how RDs are different from FDs?

-Vidya Prabhala, Chennai

Recurring deposits aka RDs are a great way of securing your emergency savings and earning decent returns. You can also easily open, manage and withdraw your RD online.

Unlike FDs, RD doesn’t require you to deposit a large amount and lets you save anywhere between 6 months to 10 years. The minimum amount to invest varies across different banks. Typically, individuals can begin investing in RD schemes with as little as Rs. 1,000.

Compared to savings accounts, recurring deposit interest rates are higher and close to fixed deposit accounts. Depending upon your tenure, RDs can offer up to 4.00% to 6.50% p.a interest. Generally nationalized banks tend to offer higher interest rates. However, the interest rate can also depend on your age and the scheme of your deposit, etc.

READ MORE: From Savings to Recurring: We explain the different types of bank accounts

Individuals can make deposits for a minimum of 6 months to 10 years with no provision for premature withdrawals. However, some banks may allow early closure of the RD account, but it is conditional.

Some banks accept standing instructions to credit one’s RD account periodically from their savings or current account. However, there are certain limitations, depending on the bank’s RD policies.

Like any other investment option, recurring deposit accounts attract taxes; their returns are subject to a 10% TDS deduction.

Recurring deposits carry no risk or very little at all, as long as the bank is credible so your money won’t be affected by market fluctuations.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.