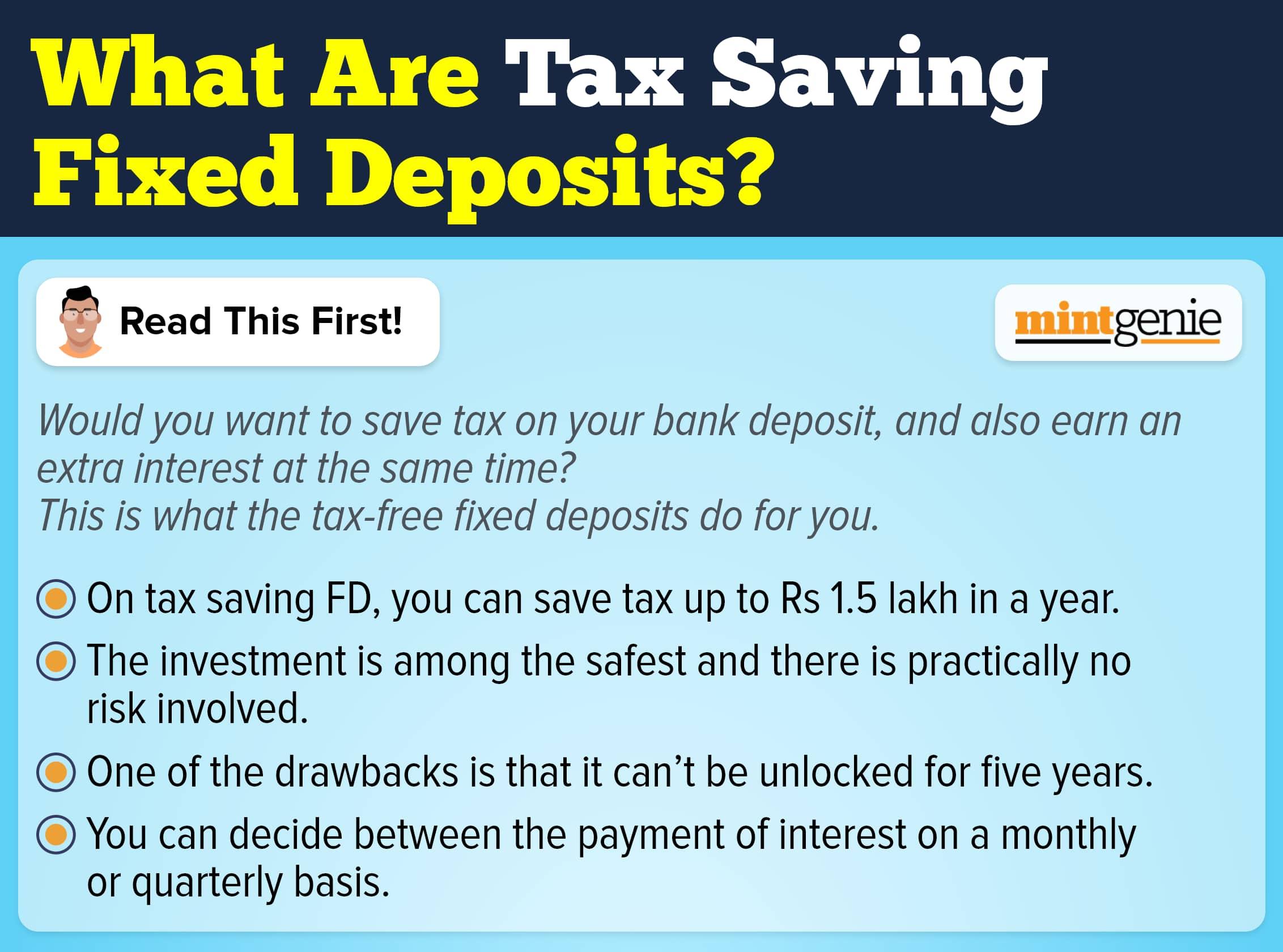

Q. I am a 32-year-old housewife. My husband is a luxury car salesperson in Gurugram. Our family has been investing in various financial products offered by banks such as recurring deposits, sweep-in accounts, and fixed deposits (FD). I recently came across advertisements from various companies offering fixed deposits at a rate higher than that offered by my bank. Are these NBFC FDs safe, and how are these NBFCs able to provide an interest rate which is typically higher than the one offered by banks. Please also elaborate on the points which one should check before opening an NBFC FD.

Sarika Godara, Gurugram, Haryana

An NBFC is a company which is registered under the Companies Act of 1956 or 2013 that engages in the business of (a) loans and advances or (b) acquisition of shares/stocks/bonds/debentures/securities issued by the government or a local authority or other marketable securities of a like nature, or (c) leasing, hire-purchase, insurance business, or (d) chit business.

An NBFC may also receive deposits from the public if it has a license for the same. Said license is provided by the Reserve Bank of India (RBI). All NBFCs have to follow various rules and regulations made specifically for them by the RBI.

NBFCs essentially are finance companies offering financial services and products such as fixed deposits to consumers, especially to those consumers whom banks are unable to reach.

How are NBFC FDs different from FDs offered by bank FDs?

It's crucial to comprehend the distinctions between bank FDs and NBFC FDs when deciding whether to invest in one or the other. Here are the two main distinctions:

- Depositors have access to a deposit insurance option through DIGC (Deposit Insurance and Credit Guarantee Corporation). This choice is not available in the case of NBFC.

- Banks may offer a number of other banking services along with the FD like, offering overdraft facilities, offering saving accounts linked with fixed deposits etc. However, NBFCs are prohibited under the law from offering any banking service to their FD customers.

Should you select a bank FD or NBFC FD?

It's crucial to choose the correct financier if you want to grow your savings with a fixed deposit. Here is a thorough comparison of NBFC FD Vs Bank FD to assist you in making the right choice:

Interest rate being offered

NBFCs typically offer interest rates that are greater than the interest rate on bank fixed deposits. This is because NBFCs are known for their "credit risk." Both NBFCs and banks use the money raised from the public through fixed deposits for on-lending for their loan business.

However, banks being larger in size and because of having access to money deposited in their savings account by the public, find it much easier to raise funds than NBFCs. NBFS are prohibited under law to raise money through on demand savings account, therefore they have

Risk that is involved

Bank FDs are generally perceived as being much safer than NBFC FDs, particularly after the Union Budget 2020 announced an increased insurance cover of Rs. 5 lakh for bank deposits. NBFCs FDs do not provide any such coverage.

However, typically both NBFCs and bank FDs receive credit ratings from credit rating agencies like CRISIL and ICRA based on their creditworthiness. These credit ratings help individuals in determining the creditworthiness of these banks and NBFCs the same way Cibil score helps banks and NBFCs in determining the creditworthiness of Individuals. We have reproduced the credit rating scale of ICRA for the perusal of the readers below:

AAA Instruments with this rating are considered to have the highest degree of safety regarding timely servicing of financial obligations. Such instruments carry the lowest credit risk.

AA Instruments with this rating are considered to have a high degree of safety regarding timely servicing of financial obligations. Such instruments carry very low credit risk.

A Instruments with this rating are considered to have adequate degree of safety regarding timely servicing of financial obligations. Such instruments carry low credit risk.

BBB Instruments with this rating are considered to have moderate degree of safety regarding timely servicing of financial obligations. Such instruments carry moderate credit risk.

BB Instruments with this rating are considered to have moderate risk of default regarding timely servicing of financial obligations.

B Instruments with this rating are considered to have high risk of default regarding timely servicing of financial obligations.

C Instruments with this rating are considered to have very high risk of default regarding timely servicing of financial obligations.

D Instruments with this rating are in default or are expected to be in default soon.”

Bundle Products

Banks often bundle multiple financial products, for example, a bank may allow the opening of a fixed deposit through their internet banking facility. Many banks offer certain credit cards against the fixed deposit maintained with them. This bundling of services is offered by NBFCs to a lower extent.

Convenience

NBFCs are generally more agile and more attuned to the needs of the customers than banks. If ease of convenience is an important factor in determining your FD choice you should opt for FDs being offered by NBFCs. You can effortlessly expand your savings with the help of the end-to-end online depositing experiences that many NBFCs provide. Additionally, with just a click of a button NBFCs will allow you to obtain a loan against FD through a paperless process.

Conclusion

It's crucial to take your individual objectives into account while arranging your savings. Make sure you do careful study and pick a plan that satisfies your needs whether you're taking out a bank FD or an NBFCs. If you are opting for an FD from an NBFC, make sure it has a decent credit rating.

Kuvera is a free direct mutual fund investing platform.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.