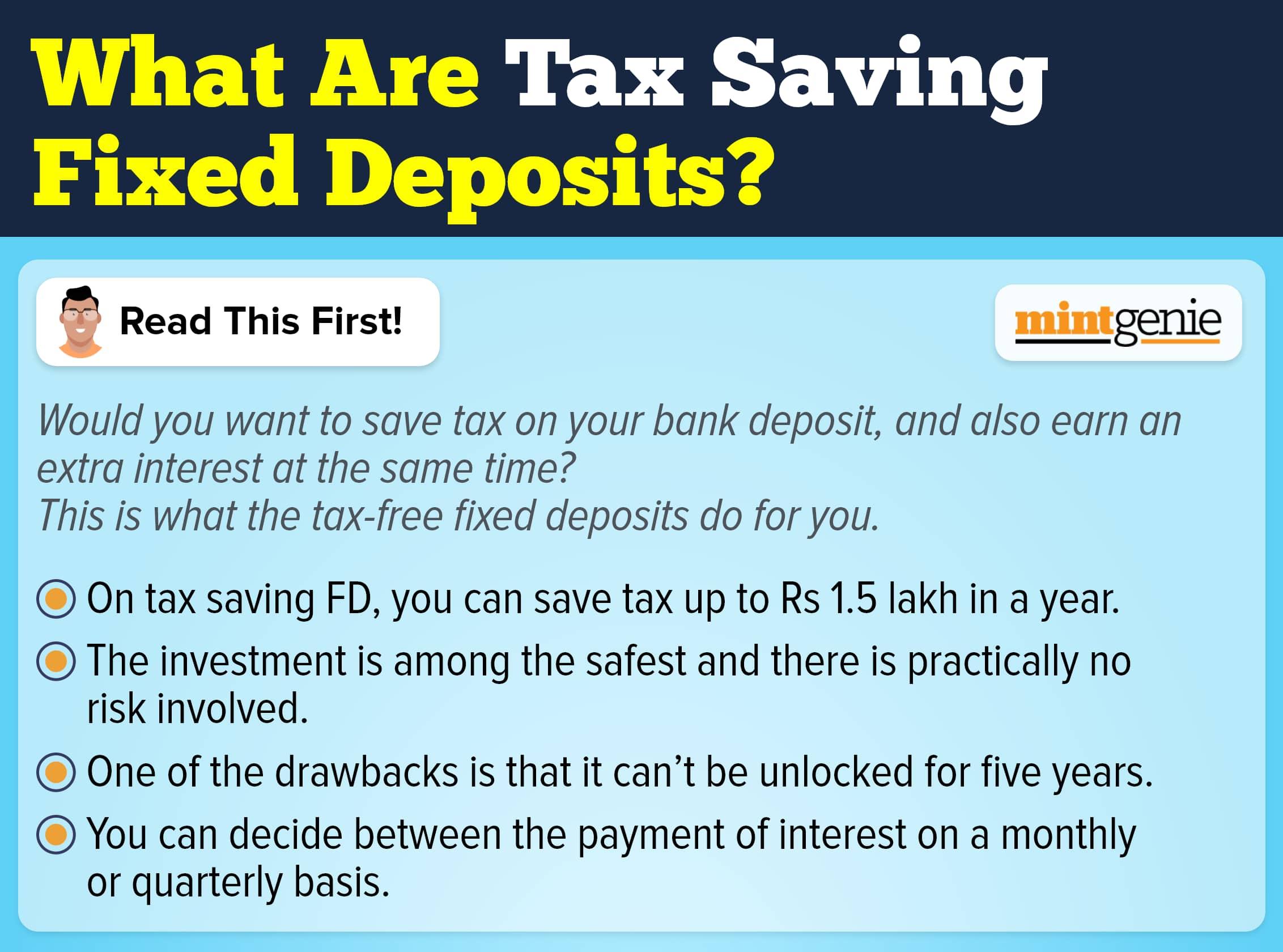

Q. I am an officer in my mid-thirties with a central government job in the Central Armed Police Force (CAPF). I wish to invest in a fixed-income instrument which could act as a safety net for the future and well-being of my family. I was planning to invest in the government-backed National Saving Certificate (NSC) which is considered risk-free and also offers tax benefits simultaneously. Could you elaborate upon the nature and some important features of the scheme?

Mr. Vinay Singh, Ujjain

The Indian government has introduced a number of schemes to encourage people to save money and make investments. Many such schemes allow you to invest small amounts and gain a good corpus later. One such scheme is the National Savings Certificate (NSC).

What is a NSC?

The government-backed National Savings Certificate (NSC) is an investment scheme that combines guaranteed returns with tax benefits. The National Savings Certificate is considered one of the most commonly used saving instruments. It is available at post offices for easy accessibility by investors. NSC is a low-risk investment option that conservative investors looking for a stable income can take into consideration.

In addition, the interest rate on the National Savings Certificate is fixed and guaranteed. The interest rate is evaluated by the government every quarter and is subject to change. There is no maximum investment amount in this scheme. Since investors can claim a deduction on the amount invested in NSCs under Section 80C, the highest deduction they can claim is ₹1.5 lakh, which is the Section 80C limit.

Who can invest in the NSC?

All individuals, including minors above 10 years of age, and legal guardians or parents on behalf of a minor, can make an investment in a National Savings Certificate. One can earn assured returns at the prevailing interest rate in NSC.

What are the features of the NSC?

The National Savings Certificate has various attractive features, which have contributed to its popularity among the general public. Here are a few of the features:

Small investments - The investment required in this scheme is extremely small. It starts at Rs. 1,000 and in multiples of Rs. 100. It has no maximum limit.

Lucrative interest rates - Although NSC functions similarly to an FD, its interest rates are unquestionably higher than an FD, making it a preferable option for many investments.

Fixed income: You may expect steady and stable returns. The interest rate on National Savings Certificates right now is 6.8% per annum. Additionally, the Government updates the rates every three months.

Nomination: The investor has the option of nominating a family member or a minor. This makes sure that, in the event of the investor's passing, the nominee will be able to inherit the funds.

Convenient: You can invest in National Savings Certificates by visiting any post office or other designated institutions. You only need to provide the necessary KYC documentation. The entire procedure is simple and easy.

Guaranteed returns: With this programme, you will receive guaranteed returns at the conclusion of your five-year maturity period. This includes the principal as well as interest generated over the years.

Tax advantage with NSC: Investments made towards the National Savings Certificate are eligible for a deduction under Section 80C up to a maximum limit of Rs. 1.5 lakhs in a financial year. Thus you can enjoy tax benefits on your investments.

Easy transfer: It is very simple to transfer your NSC from one post office to another. Similarly, you can also transfer your NSC from one person to another. In this case, the name of the original owner will be rounded off and the name of the new owner will be added.

Premature withdrawal: Normally, premature withdrawal from the National Savings Certificate is not permitted. However, under special circumstances, it may be allowed. These include a court order or the demise of the actual investor.

Modes & types of NSC

Here are the different modes by which investors can hold a National Savings Certificate:

Single holder type certificate: As the name implies, single holder certificates are issued to single individuals only. He or she may nominate an applicant for the certification. The original holder, however, retains the authority to make decisions. Additionally, these certificates may be issued to a minor's legal guardian.

Joint 'A' type certificate: Joint 'A' type certificates are issued to joint holders, i.e., up to three adults. The proceeds of the certificate are paid to these joint holders when it matures. All people are involved in making decisions. The signature of all joint holders is necessary in order to appoint a nominee, cancel the nomination, or transfer the nominee.

Joint 'B' type certificate: This type of National Savings Certificate is also issued to up to three adults. However, the primary distinction between type "A" and type "B" is that the latter is paid to any one of the joint holders. The decision-making and nomination powers in type "B" are identical to those in type "A."

Tax benefits of NSC

The main tax benefit of NSC is provided by Section 80C of the Income Tax Act. This lets investors take advantage of the Section 80C tax deduction of up to Rs. 1.5 lakh every financial year.

Additionally, the interest earned on the certificates annually for the first 4 years is deemed to be reinvested (i.e., added back to the initial investment) and, hence, is also eligible for a tax break, subject to the overall annual limit of 1.5 lakh. But the interest earned in the fifth year is not re-invested, so it is taxed at the investor's slab rate.

Conclusion

We have plenty of options when it comes to investments. Depending on your financial objectives, you can select any of them. One of these choices is the National Savings Certificate, or NSC, a post office savings product. This is generally considered a secure and low-risk product for risk-averse investors.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.