Q1. We have been engaged for 2 years and are getting married soon. What are the mandatory finance talks that we need to have? Or is it too early to talk about money?

Money or finance has long been known to be a source of stress and disagreements in relationships. For many couples, it is a topic that is mostly avoided. Like you, many couples think that probably it is too early to talk about money matters before getting married. And after marriage, many assume that things will fall in place and there is no need to discuss money. Sometimes, the partners (or at least one of them) are insecure about their financial situation and feel that it may become an issue if brought up.

Being on the same page when it comes to financial decisions and planning plays a major role in a healthy relationship. Each financial goal or objective demands a certain kind of planning. It is important to know if both of you have the same, similar or different financial goals and how you wish to achieve those.

For example, do you both want to have children? Want to travel twice a year? Pursue higher studies? Buy a bigger house? The goals may be different, but a discussion will help you both understand each other better, especially each other’s attitude towards money and financial habits.

The first thing that you need to discuss with your partner is your current financial situation. This is not about sharing your ATM pins or opening joint accounts. Talk about your current income, expenses, savings, investments, obligations and if you adhere to a budget.

Next, discuss your short-term and long-term goals. It could be buying a house in the next 5 years or a car in a year. Or it could be repaying a current debt or fulfilling an obligation. Remember that your goals need not be the same, but both must understand and accept each other’s goals.

The third important thing to discuss is how you plan to combine your finances. Some couples choose to have joint accounts, whereas some prefer to keep their accounts separate. The same goes for investments and obligations. You must decide who will take care of what if you do not want to set up a joint account.

These discussions will help you understand each other better in terms of money habits. The more open you are about discussing money matters, the stronger will be the foundation of your relationship.

Q2. I am 67 years old, and now planning to retire from my business. My spouse is a homemaker. All our lives, I have taken financial decisions and my spouse has never taken any interest in financial matters. Should I start talking to her about money now? What does she need to know about finances?

Whether she is a working woman or a homemaker, your spouse needs to know about various aspects of finance, like investments, obligations, insurance, etc. It is high time that you involve your spouse in financial decisions. Every woman needs to be prepared for unforeseen circumstances.

Communicate

Start having regular conversations with your spouse on various money matters. Make her aware of all your current investments. When you are planning a new investment, involve your partner in the discussion so that she is aware of and comfortable with it.

Storage of data and documents

This is very important. Your spouse needs to be aware of all documentation pertaining to the investments that are being made or have been made. From statements to receipts, make sure she is aware of the nature and location of all the records. If she is not a joint holder, check if the nomination has been updated in all investments. Make a note of bank accounts, FDs and all other investments and share that information with your spouse.

Plan your finances

Inform your spouse about all your current major expenses. Create a budget for regular expenses. Plan for future expenses. Prepare for your retirement now so that both of you can live a comfortable and financially stress-free retired life. In your absence, your partner should be able to maintain the same lifestyle.

Insurance

Make sure that you and your partner are both adequately insured—life and health insurance. Check if the nominations are in place. Let your spouse know what insurances you have and for how much you are covered. If you have an advisor who helps you with insurance, introduce them to your spouse, so that if required, she will know whom to contact for claims.

Save in spouse’s name

While you may have a joint account and you are taking care of all the expenses, have savings and investments in your spouse’s name, too. Often, while the claims are being processed or accounts are in transition, the spouse does not have access to adequate funds to meet expenses. To avoid this situation, it is better to have some investments and savings in the name of the spouse.

Estate planning

One thing that everyone ignores is writing a will. In India, if there is no Will written then the estate laws – which are based on religion – apply at the time of death. I would suggest you read about the law that is applicable to you and in case you have disagreements with the same then please do write a Will. You could look at single will or joint will, register or not. However, if you have a big family and have a high net-worth then it would be better to involve a legal party and register your will.

It is important to talk about money matters with your spouse, especially at this age. Whether your spouse has any interest in managing finances or not, she must know about the quantum and nature of investments. Of course, it would be easier for her if you are already using a financial advisor and she participates in the discussions.

Q3. What is the right time or right age to start retirement planning?

Just as there is no right age to learn new things, there is no right age to start retirement planning. As you grow older, new goals may emerge. With a good retirement plan in place, one can retain the power to fulfil one’s wishes, maintain financial freedom and enjoy peace of mind.

Retirement planning is simply preparing today for tomorrow. It involves identifying income sources, short-term and long-term goals and expenses, saving and investing and managing risk-return tradeoff to make sure that you do not have to be dependent on anyone.

Though there is no hard rule about when to start retirement planning, it is best to start at an early stage in life. The earlier you start, your investments have more time and potential to grow, even if your early savings are likely to be smaller, but you will be able to make the most of the compounding effect on investments. Your money will have ample time to outgrow inflation. The later you start, the lesser the compounding effect.

Our average life expectancy has gone up in recent times. By preparing for retirement early in life, you are preparing yourself to deal with medical emergencies, enjoy a stress-free retired life, and even leave a legacy to your children.

Start planning now! And while doing so, do not forget to give a full disclosure to your financial advisor on family health history, expected expenses and incomes, etc., to help prepare a better and sustainable plan for you.

Q4. Our children are 12 and 8, and we have been trying to teach them both about how money works. However, some of our friends feel that it is too early, and we should not give money in our children’s hands, nor should we discuss money with them. What is your opinion? What is the right age to teach our children about money and money management?

Many parents prefer not to discuss money with their young children. Why should they know about money, when the parents are there to take care of them? Some parents do not prefer to discuss money matters even with their grown-up children! Then there are wise parents who not only talk about money with their children but also give them an idea about investments and how they work.

Like swimming or cycling, money management is a basic life skill which should be taught to children. Right from a young age, start teaching them how money works, or how money helps us buy things we need and want. However, how much information to give is in your hands and at your discretion. For example, while some parents do not mind telling their teenagers how much they earn, they avoid discussing this with their younger children.

Start by teaching your children the very concept of money. Introduce them to various currency denominations. Whenever you make a purchase with cash, let them know that you are buying something with money. If you are making a purchase through a debit or credit card or buying online, explain that to them.

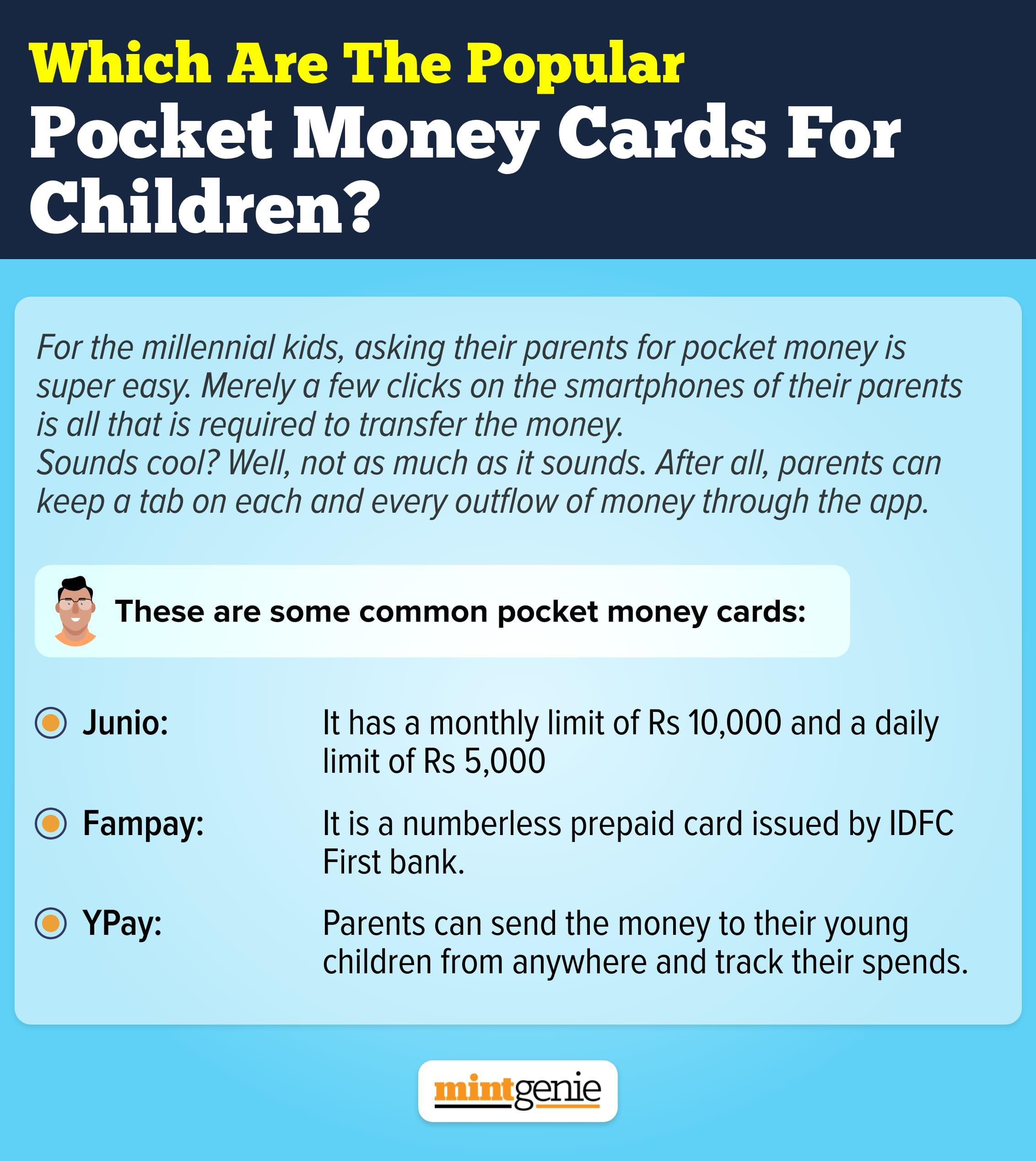

Pocket money or weekly/monthly allowance is another wonderful tool to teach your children about money as well as budgeting. Try associating the pocket money with the household chores that your children do. This will help them understand how money is earned in exchange for service.

Encourage them to keep a record of their earnings (allowances) and expenses. Similarly, when the children ask for a toy or a game, ask them to keep a certain sum of money aside every week or month. This will teach them about savings and budgeting.

Open savings accounts for your children. Give them a debit card associated with that account and set a withdrawal limit on the cards. Get your children to deposit their savings in this account and help them see the money grow. This will teach them two things: savings and the basics of investments.

When you start at an early age your children will understand finances better. However, to repeat, how much money knowledge to feed them at what age is up to you as parents.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

International Money Matters Pvt Ltd is a SEBI registered personal finance firm.