Q1. When I die my legal heirs will naturally get my property and other assets. Why should I take the trouble and incur the expenditure related to preparing a will?

We expect and want everything to go smoothly after we die. However, disputes among those you hold dear about dividing what you have left behind can get very acrimonious. The best way to avoid this is to prepare a will that clearly states how you want your assets to be managed after you move on.

Without a will, your spouse, your children, and other relatives can claim a share of your wealth. A will is the legal way to clearly state who gets what portion of wealth or how you want your wealth to be used after your death. That leaves no room for any guesswork, arguments, or subjective interpretations about what your final wishes might have been.

The law: Laws of succession govern the distribution of assets of a deceased individual. Succession refers to the process by which someone is entitled to a property or an interest in the property of a deceased person. Intestacy is the condition of the estate of a person who dies without leaving a valid will. When a person dies without leaving a valid and enforceable will, it is called intestate succession. In this situation, the personal laws applicable to the deceased determine how the assets are distributed.

The personal laws of intestate succession are based on religion and region. Rather than letting the law call the shots by default, if you want specific persons or causes to benefit from your assets, please do write a will.

Preparing the will: You do not have to wait to be old to prepare your will. As the testator (the person who makes the will) you have the right to modify or revoke your will as often as you want during your lifetime.

You must be careful when it comes to choosing your executor, the person you authorise to execute the will. That person will be in charge of wrapping up all your affairs and responsibilities, including closure of bank accounts and liquidation of assets. Given the crucial responsibility, it must be someone capable and trustworthy. If your will does not specify an executor, the court will appoint an executor.

As a parent, you are responsible for all matters pertaining to your young children. In the event of your sudden demise, the executor will end up playing the role of a guardian as stated by you in the will. Again, if you do not specify a guardian, the court will choose a guardian and you will not be around to assess if that is the choice you would have preferred.

There are a few things you must keep in mind while writing a will to avoid any unnecessary legal issues and to avoid potential arguments among your family members.

- Make sure you start with a declaration stating your name, age, father's name, and your residential address in full (at the time of writing the will) so that it confirms your identity.

- It is important to clearly state that you are preparing the will voluntarily in a sound state of mind, without being under any duress or influence.

- Identify each asset and mention the name(s) of the individuals whom you want to receive the asset. Also include their addresses and dates of birth.

- Sign the will in front of two witnesses who must also sign the document and provide their complete identifying information.

- Review the will periodically and make the changes you think are necessary.

The earlier you prepare your will, the better it is for all. These days it is easy to download a format of a will from the Internet. You may not even need a lawyer, unless you have a large or complex estate, or contentious family dynamics.

Or you may prefer to get advice from an expert who can also help you register your will.

Q2. I am a young father with a two-year-old child. How should I go about planning for his higher education? Or is it too early?

It is never too early to plan. We are happy to know that you are planning to save for the long term.

The cost of education in India has been rising by 10% to 12% every year and is already a major outflow for every young family. Therefore, it is important for you to start saving and investing to build an education corpus as early as possible, so that you can benefit from the power of compounding.

To beat education inflation, you will need to invest in a fund that gives you a return of about 12%-15%. A monthly systematic investment plan (SIP) in equity mutual funds would be the ideal choice as it gives higher returns than debt funds in the long run. Given that you have a good 16 years before your child starts college, equity mutual funds would help you build a sizable corpus over the long term.

If your investment horizon is less than five years (say you need the money for your child’s primary education) then it is wiser to opt for investment-grade debt funds. Although their returns are less compared to equity mutual funds, these debt funds offer guaranteed returns and safety of capital.

Keep in mind, though, that your investment amount would depend on the type of education you intend on giving your child. Studying abroad would require a larger corpus than higher education in India.

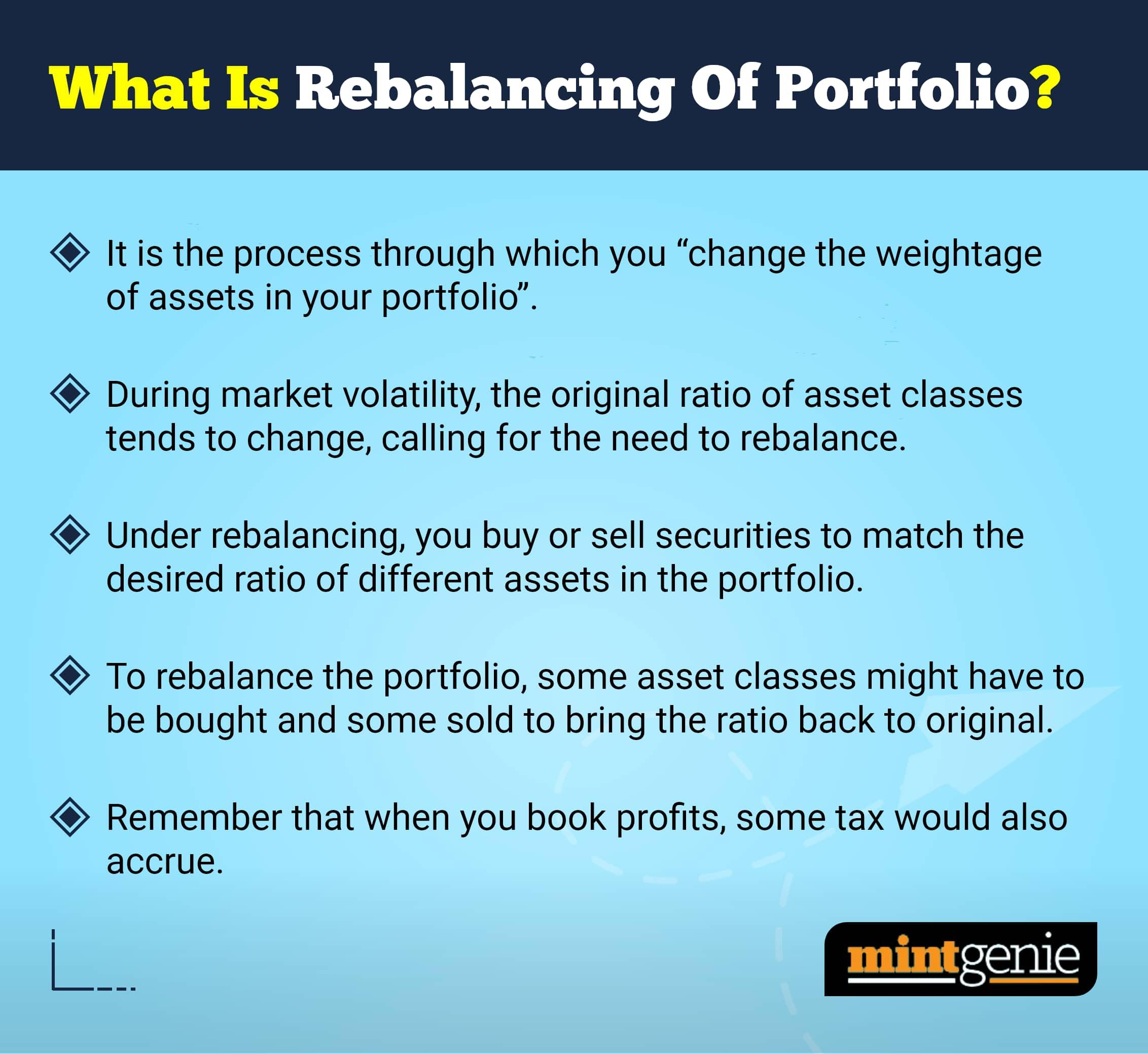

Q3. I had invested in certain assets after careful consideration. Now my financial planner is suggesting a change in allocation after a review. Why go through the exercise again?

As life moves on, there are bound to be changes in your goals and the distance to each goal. It is important to relook at the portfolio allocations, to keep up with these changes.

Time-horizon investing is all about planning. Take a fresh look at your goals periodically. Once you have done that, allot your funds based on how long you will need to keep funding to attain a specific goal. It might have been a long-term goal when you started. As you near the goal, the term gets short. Now, you will want to shift the assigned assets to a more conservative investment. This will reduce the risk of market-related losses derailing your strategy.

Investments made to fund a goal must be monitored regularly. Towards the end, you should switch from growth assets to liquid assets so that the funds can be easily accessed when required. Plan for the switch. Do it over a period so that there is some protection from volatility in the value of growth assets. Over time, the low-price points will be balanced by the high price tranches.

Q4. My father has just retired and is keen on investing his benefits in a fixed deposit. How do I convince him that a systematic investment plan may be a more rewarding option?

Fixed Deposit (FD) is an investment option offered by banks and post offices. You deposit an amount once for a fixed duration. You may choose to have the interest transferred to you periodically or to reinvest it, thus adding to the capital. You get back your investment amount at the end of the tenure. If you break the FD during its tenure, you will need to pay some charges to the bank.

Systematic Investment Plan (SIP) is a mutual fund investment option that allows people to invest a small amount at regular intervals.

Based on current life expectancy, if the retirement is at 60 yrs then the corpus built should be able to provide for expenses post retirement for a good 25 to 35yrs. To ensure that the retirement corpus supports him for his lifetime and provides returns that beat inflation, some allocation to equity (15%-20% at least) is required.

A bit of equity will give a little boost to the portfolio, generating slightly higher returns without adding to too much to the risk. A combination of some lumpsum and SIP in a low-cost index fund can be a good starting point to achieve this allocation.

The following comparison should help you talk to your father about the relative merits of FD and SIP.

| FEATURE | FD | SIP |

| Investment frequency | Once. | Monthly |

| Returns | Pre-fixed by the bank or post office. | 10%-12% over the long term, assuming large cap fund but can vary based on category. |

| Tenure | Medium or long term (usually 1 to 5 years). | Ideally 5 years +. Longer the tenure, better the equity compounding. |

| Risk | Low, but inflation-adjusted returns can be low or even negative. | Depends on the type of fund and tenure. For the long term, risk is lower. |

| Liquidity | High. However, there can be a penalty for premature withdrawals. | High. Usually, 1% exit load if you exit before 1 year. Nil after a year. |

| Tax | According to the investor’s slab rate. | Equity funds: More than 1 year 10% tax; less than 1 year 15% flat tax. Debt: More than 3 years 20% with indexation benefit; less than 3 years as per slab rate. |

| Compounding benefit | Low, due to lower rates and higher taxes. | High. As investing happens through market ups and downs, it allows rupee-cost averaging. Better compounding over the long term. Possibility of better post tax and post inflation returns. |

International Money Matters Pvt Ltd is a SEBI registered investment advisory firm. If you have any personal finance queries, click here to talk to advisors from IMMPL.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.