Q. I am a working professional in my mid-thirties with a stable government job with the armed forces. I have three daughters and have been planning to invest in gold for their marriage in the future. I have heard that investment in Sovereign Gold Bonds is a much better investment option than investing in physical gold. Can you elaborate on the major differences between the two options and also tell me which category is more suited if I require physical gold in the future.

Nishant Prasad, Banswara, Rajasthan

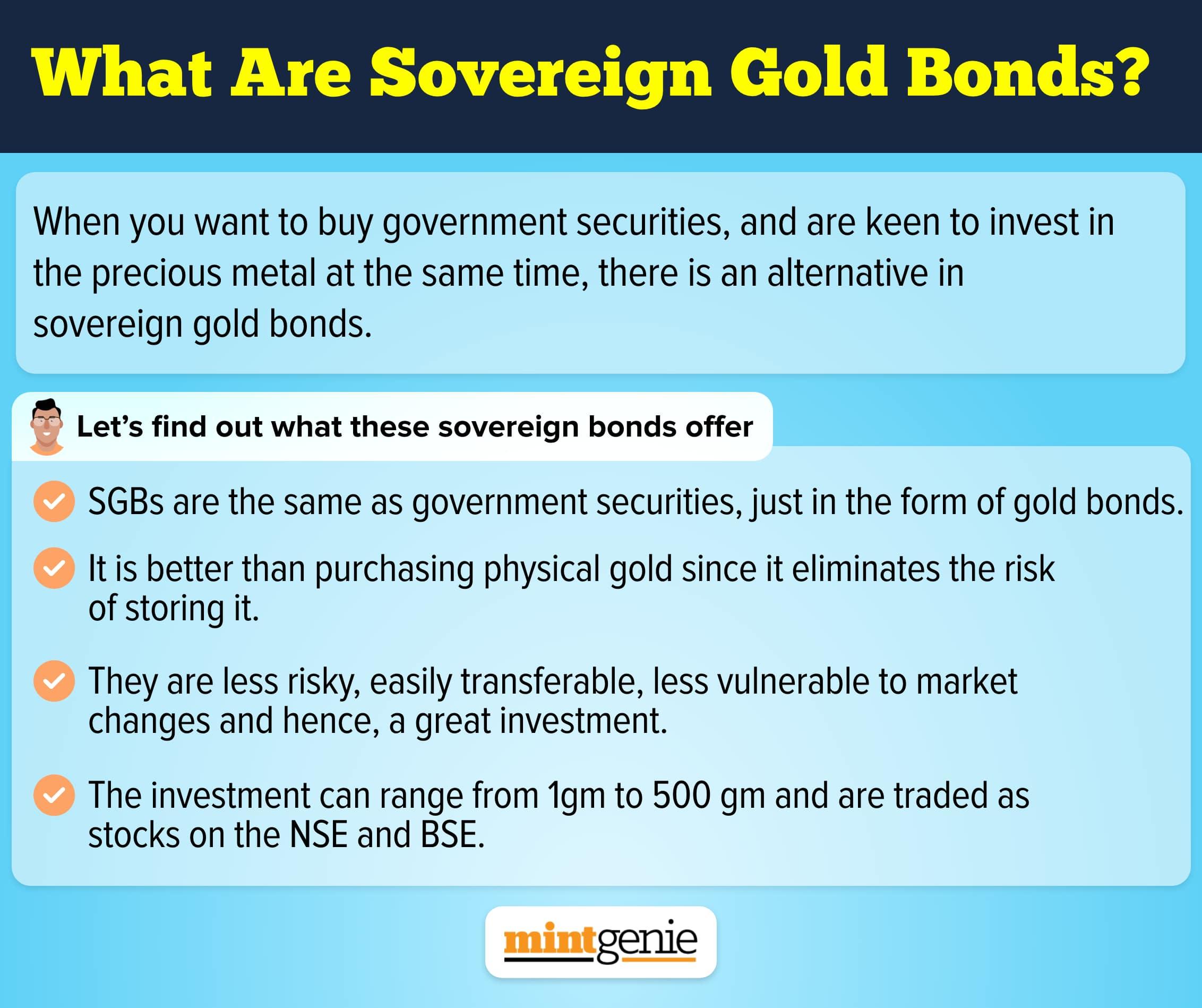

Sovereign Gold Bonds (SGBs) are government bonds that are denominated in grams of gold. They serve as alternatives to holding actual gold. These bonds must be redeemed in cash when they reach maturity, at the time of maturity your redemption amount will be directly dependent on the prevailing rate of gold at that time.

Additionally, SGBs holders receive interest at a rate of 2.5 percent annually, payable every six months. Interest earned on the SGBs is taxable as per the tax rate applicable to your tax slab. However, it is important to note that at the time of redemption you need not pay capital gains tax since the government has specifically exempted payment of capital gains tax at the time of maturity for SGBs. The Reserve Bank of India (RBI) issues the SGBs on behalf of the Government of India.

Eligibility

Indian citizens as specified under the Foreign Exchange Management Act, 1999 are eligible to invest in SGBs. Individuals, HUFs, trusts, universities, and nonprofit organisations are all examples of eligible investors.

How to apply

You can invest in SGBs either by physically filing an application with approved Post offices, SHCIL (Share Holding Corporation of India Limited) offices, banks, and agents, etc., or you can invest online through your bank’s app or through investment apps such as Kuvera.

Issuance price

The nominal value of SGBs shall be based on the simple average of the closing price of 999-purity gold for the final three business days of the week prior to the subscription period as announced by the India Bullion and Jewellers Association Limited.

Maximum and minimum investment limit

The SGBs are offered in multiples of one gramme of gold. The minimum investment in the SGBs is one gramme, and the maximum subscription limit shall be four kilograms for individuals, four kilograms for Hindu Undivided Families (HUF), and twenty kilograms for trusts and other similar institutions. The annual ceiling will cover both bonds obtained at the time of primary issuance and any purchase made from the secondary market.

Evidence of investment

On the date of the SGB issuance, ‘certificates of holding’ will be provided to the investor. If an email address has been provided on the application form, you will receive a certificate of holding directly from RBI via email. For other cases, the certificate of holding can be picked up from the issuing banks, SHCIL offices, Post Offices, designated stock exchanges, or agents.

Premature redemption

Although the SGBs have an 8-year term, early encashment or redemption is permitted on interest payment dates after the fifth year from the date of issue. Additionally, if stored in demat form, the SGBs can be traded on stock exchange at any point in time.

Procedure for premature redemption

Investors can contact the concerned bank, SHCIL offices, Post office, or agent, thirty days prior to the interest payment date in the event of early redemption. The customer's bank account, which was provided when applying for the bond, will be credited with the proceeds.

Collateral

Use of SGBs as security for obtaining loans (including gold loans) from banks, financial institutions, and non-banking financial companies is permissible. Banks and financial institutions treat SGBs just like gold. The ‘loan to value ratio’ will be the same as that which is appropriate for regular gold loans as set forth from time to time by RBI. Loans secured by SGBs would be subject to the bank's or financing agency's decision and could not be assumed to be a matter of right.

Redemption on maturity

When the SGBs mature, they must be redeemed in Indian Rupees, you cannot request for physical gold at the time of redemption. The redemption price is determined by the simple average of the closing price of 999-purity gold over the previous three business days as announced by the India Bullion and Jewellers Association Limited.

Current issue of SGBs

The second public issue of the SGBs for the financial year 2022-23 opened on 22nd August the issue is open till 26th August. The bonds will be issued on 30th August. The price of SGBs at the time of the issuance will be INR 5,197 per gram. If the investor pays using digital means, there is a discount of INR 50 per gram.

Conclusion

SGBs are definitely a better investment option than investing in physical gold, they are a more tax-efficient investment and if purchased in demat form can be traded on the stock exchange at any point in time conveniently. However, at the time of redemption, you will not be getting physical gold but cash equivalent of your SBG holdings at the prevalent market price.

Investors who wish to invest in gold with the intention of using the gold at the time of the marriage of their kids can invest in SGBs and use the cash they receive at the time of redemption for the purposes of purchase of jewellery.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.