India's 10-year bond yield, the benchmark of bond yields, on April 11 spiked to its highest level in nearly three years, following the hardening of US bonds and a hawkish tone from the Reserve Bank of India (RBI).

10-year bond yields near three-year high; What it means for equity investors?

TL;DR.

- Bond yields rose after the RBI hinted it was getting ready to tread the course of policy normalisation gradually and stated that its priority has shifted from growth to inflation which is high led by the Ukraine war.

The benchmark 10-year bond yield touched 7.19 percent in intraday trade, its highest since May 2019 against the April 8 close of 7.12 percent.

Bond yields rose after the RBI hinted it was getting ready to tread the course of policy normalisation gradually and stated that its priority has shifted from growth to inflation which is high led by the Ukraine war.

"The higher end of the yield remains cautious due to the policy normalisation, rising inflationary pressure, and the higher government-borrowing program for FY23 (highlighted in the Union Budget this year). However, with policy normalization, the yield curve is likely to become normal going forward as against steeper from the last few quarters," said Neeraj Chadawar, Head - Quantitative Equity Research, Axis Securities.

Why are benchmark bond yields rising?

Bond yields, in simple terms, are the return investors earn if they hold bonds until maturity. They are rising in India reacting to the mildly hawkish policy, revision of inflation and GDP forecasts by the RBI and the prospects of the end of easy monetary policy.

Bond yields are rising as the RBI is likely to keep a hawkish stance due to fundamental pressure like higher government borrowings, increasing crude oil prices and other commodities.

Deepak Jasani, Head of Retail Research, HDFC Securities pointed out that although HTM (held to maturity) limit has been enhanced from 22 percent to 23 percent till March 31, 2023, bond prices took a hit due to faster than expected policy normalisation from the RBI governor’s speech.

"The RBI might intervene through OMOs (open market operations) and operation twists to cap the upside to some extent. Given that RBI has started draining liquidity from the banking system, it’s unlikely to announce direct bond purchases. Faster global policy normalisation amid persistently high inflation, elevated energy prices and huge local borrowing programme are likely to keep the long-term end of the yield curve at the elevated levels," said Jasani.

"Besides, RBI governors have admitted that real yields need to be positive meaning a substantial rise in interest rates if price pressure persists. Indian bonds, if included in the global bond indices in the second half of the financial year 2022-2023 (H2FY23), would provide some respite to bond market participants (though taxation issues need to be sorted out at the earliest to smoothen the process)," Jasani added.

What should investors do?

Bond yields have a negative correlation with the equity market which means if bond yield goes up, the equity market will plunge.

Equity markets should logically underperform when interest rates are rising as the present value of future cash flows (meaning stock prices) could come down when interest rates rise. Even otherwise if bond markets seem lucrative, some portion of incremental flows and even the existing equity funds can be diverted to bond markets, Jasani pointed out.

Jasani advised investors should stick to the asset allocation plan between equity and debt and do rebalancing at regular intervals. By doing this, they would have diverted some funds to bond markets when the equity markets had gotten overheated some time back and vice versa. Investing in 10-year bonds at this stage carries the risk of MTM (mark to market) losses if the yield on it keeps rising.

Srikanth Subramanian, Head-Kotak Cherry, Kotak Investment Advisor observed while equity markets generally look at earnings growth and expectations of earnings growth in the future, the discounting factor for earnings is the prevalent rate regime.

"As rates go up, the discounted value of future earnings become that much less valuable today, and hence globally, equity markets have slowed down to absorb the impact of higher rates. The fall-off has been more prominent in hypergrowth companies, where a large part of the value is ascribed to future earnings, and hence are more susceptible to rising rates," he said.

Sector rotation, style rotation and asset allocation are the keys to making money in the market. At this juncture, the market has many headwinds and analysts advise one must shift focus to value themes amid rising inflation and looming interest rate hike.

"As we have seen historically, value themes tend to do better in rising inflation and interest rate scenarios. We could see a good allocation in value-oriented sectors in the next one-two years. Further, in the rising interest rate scenario, the banking stocks tend to do better, and the next leg of the rally in the benchmark could be driven by the BFSI space," said Chadawar.

10-year G-Secs or liquid funds?

Many investors may be wondering why to invest n liquid funds when 10-year bonds are giving returns of more than 7 percent. After all, bond yields do not move so frequently.

In fact, this makes sense as liquid funds may not match the returns on 10-year bond yields.

"Currently we may see the rising interest rate scenario in the world economy and it is advisable that investors may take some position in the longer-term G-secs bond to safeguard their investment and earning returns. Liquid funds may not be provided that much returns which bond may provide," said Rohit Gadia, Founder at CapitalVia Global Research.

But one must keep in mind that government securities (G-Sec) and liquid funds are two very different products and G-Sec have their own risks. Besides, liquid funds are short-term investment tools and have low risk compared to long-term bonds.

"Both G-Secs and liquid funds are two very different products and buying G-Sec exposes investors to duration risk, i.e. risk that value of their holdings may fall as rates move higher, so in that sense, these are more suitable for investors who are comfortable taking the volatility and risk associated with rates going up," said Subramanian.

"Liquid funds are purely vehicles for parking short-term cash, till such time investors find a more durable investment option. While returns from liquid funds are very low, there is an extremely low probability of capital getting eroded," Subramanian added.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

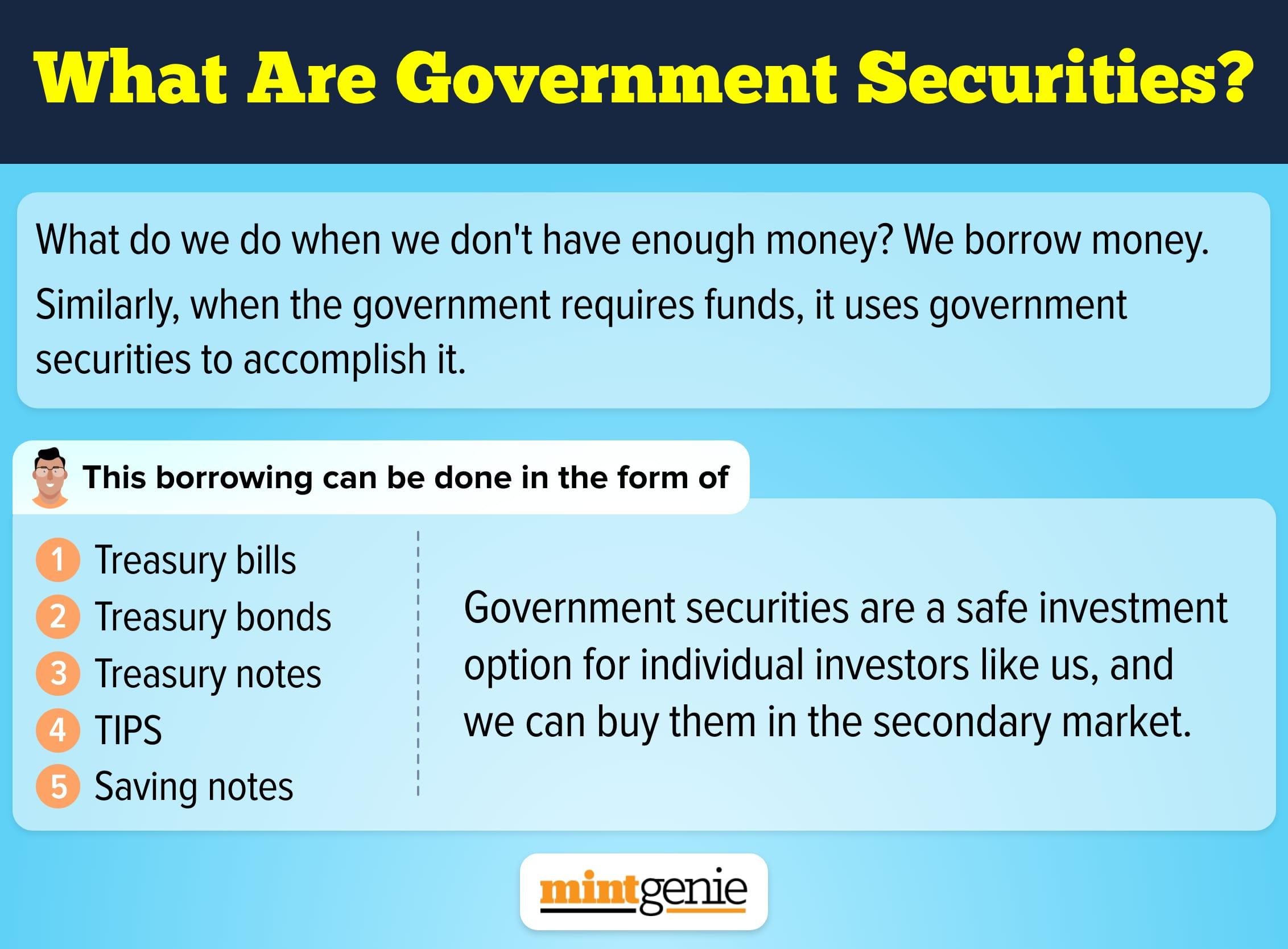

Government securities are tradable debt instruments that the government offers in the form of bonds, treasury bills, or notes.

First Published: 12 Apr 2022, 12:32 PM IST