Since hitting its all-time low of ₹40.55 in July last year, the stock price of food delivery company Zomato has risen nearly 30 percent. It is now down 30 percent from its IPO price of ₹76 versus over 46 percent last year.

64% potential upside! Zomato to continue to gain market share from Swiggy, says HSBC

TL;DR.

The food delivery industry may slow down further in Q4FY23, but the brokerage expects Zomato to reclaim market share. It also believes that the ‘Gold’ loyalty program is helping it win market share from rival Swiggy.

However, the stock has fallen 34 percent in the last 1 year and 11 percent in 2023 so far. While brokerages and market experts were cautious on the stock post its listing, they have now turned bullish and expect strong upsides for the stock going ahead.

Most recently, global brokerage firm HSBC, in its report, maintained its ‘buy’ call on the stock with a target price of ₹87, indicating an upside of 64 percent.

The target price by HSBC beat the IPO price of Zomato and is almost near its all-time high of ₹88.4, hit in March 2022.

The food delivery industry may slow down further in Q4FY23, but the brokerage expects Zomato to reclaim market share. It also believes that the ‘Gold’ loyalty program is helping it win market share from rival Swiggy. HSBC further added Blinkit remains underappreciated and it believes that it can add value over the next 1-2 years.

In January, Zomato reintroduced its loyalty program with a focus on food delivery at an introductory price of ₹149 for three months. It is Zomato’s fourth iteration of its loyalty program in the last few years. Before launching Pro Plus in 2021, Zomato had introduced Pro in 2020 which replaced the original Zomato Gold membership programme.

Despite the firm reporting widening of losses in the December quarter, the outlook of the stock remained strong and most brokerages remained positive.

Earnings

In the December quarter, the company reported a consolidated net loss of ₹347 crore, on the back of higher expenses and a slowdown in the food delivery business. It had posted a consolidated net loss of ₹67.2 crore in the same quarter last fiscal. Zomato's consolidated revenue from operations during the quarter under review stood at ₹1,948.2 crore versus ₹1,112 crore in the corresponding period a year ago.

The total expenditure of the online food app jumped over 51 percent on year for the October-December quarter and stood at ₹2,485.3 crore versus ₹1,642.6 crore. Whereas, the food delivery business' gross order value (GOV) growth in Q3FY23 grew by just 0.7 percent sequentially, in an otherwise seasonally strong quarter.

"We have seen an industry-wide slowdown in the food delivery business since late October (post the festival of Diwali). This trend has been seen across the country but more so in the top eight cities," Zomato CFO Akshant Goyal said. It remains a challenging demand environment for the food delivery business, he said, however, adding, "we are seeing green shoots of demand coming back in the recent weeks, which makes us believe that the worst may be behind us."

On whether signs are emerging about a slowdown in the long-term growth in the food delivery business, Zomato founder and CEO, Deepinder Goyal said, "We believe that the long-term opportunity remains large and exciting."

Zomato has not revised its target of reaching adjusted EBITDA break-even, excluding its quick commerce business, by Q2FY24.

Investment Rationale

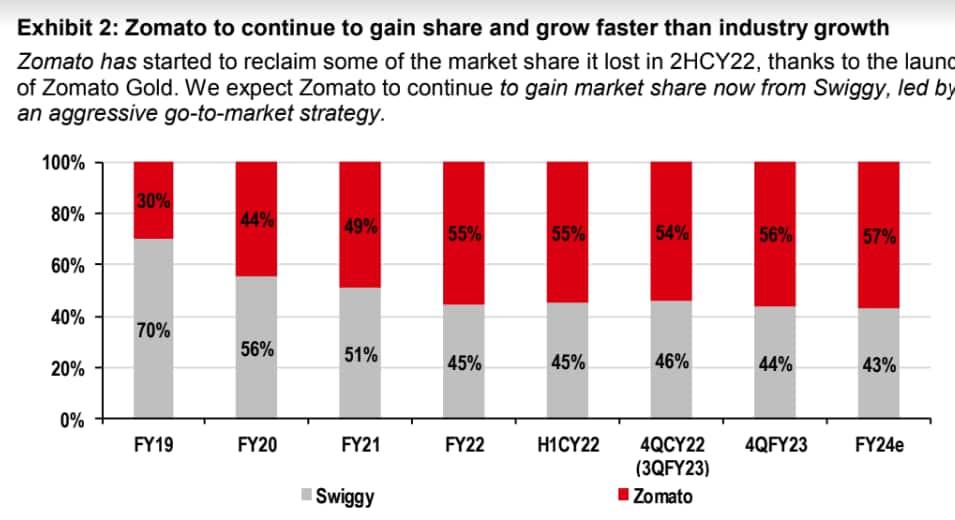

(1) Zomato’s growing market leadership: The brokerage noted that Zomato has started to reclaim some of the market shares it lost in H2CY22, thanks to the launch of Zomato Gold. It expects Zomato to continue to gain market share from Swiggy, led by an aggressive go-to-market strategy. HSBC also sees Zomato’s share improving to 57 percent in FY24. This would mean, notwithstanding the loss in 2022, that Zomato has gained 13 ppts in terms of market share from Swiggy since FY20, it added. It expects the market shares of Zomato and Swiggy to diverge to 57 percent and 43 percent, respectively, in FY24.

Source: HSBC

Zomato’s unit economics (UE) continue to impress: As per the brokerage, Zomato continues to impress with its improvements in UE through Q3FY23 and is now EBITDA positive (adjusted) in the food delivery (FD) business.

In Q3FY23, the company reported a contribution margin (CM) of ₹21.5/order, however, from Q4FY23 onwards, there will be a negative impact from Zomato Gold in the range of ₹10-12/order, which could concern investors, it cautioned. But, HSBC believes Zomato will be able to offset this impact from its continued push for higher take-rates and lower costs.

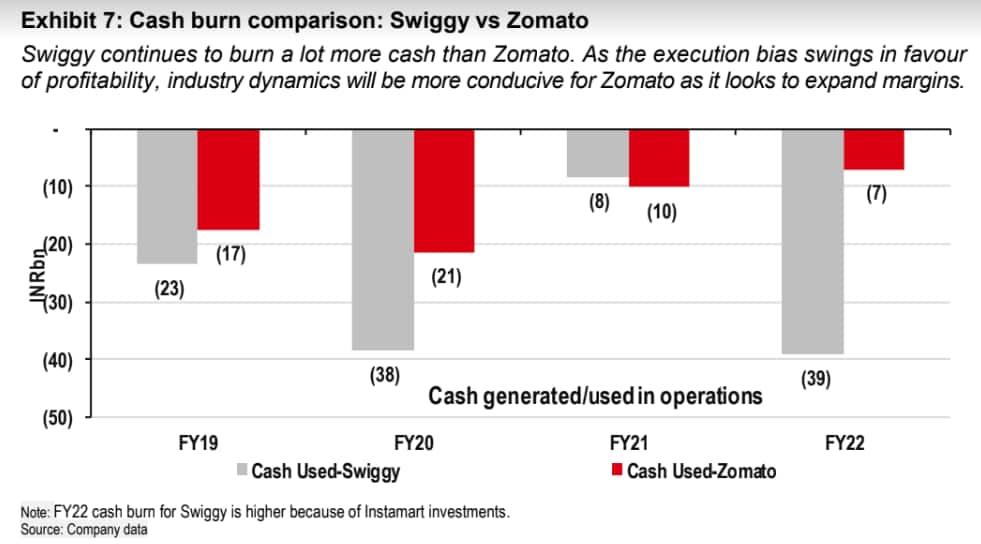

In the coming quarters, as the company absorbs the impact of Zomato Gold, EBITDA margins should continue to improve, it predicted. On top of this, Swiggy continues to burn a lot more cash than Zomato and as the execution bias swings in favour of profitability, industry dynamics will be more conducive for Zomato as it looks to expand margins, said the brokerage.

Source: HSBC

FD industry should grow over the medium to long term: While the FD industry is expected to remain weak in Q4FY23, there is no reason to assume that over the medium term (2-5 years) growth can’t be sustained at 15 percent, forecasted the brokerage. As per the brokerage, the migration of annual users to monthly users should continue with increasing awareness and per capita income. It reiterates that the FD growth in India is not so much an issue of migrating from the Food Services Industry, but rather a shift from home-cooked food.

Blinkit remains under-appreciated by the Street: As per the brokerage, Hyperlocal/Q-commerce is likely to see strong growth for a few years due to low penetration and stabilising competition. Blinkit’s current GOV (gross order value) run-rate is $1 bn, informed HSBC, adding that in FY25e, the business could easily achieve GOV of $2 bn, which even at 0.5x GOV could provide $1 bn to the stock value (20-25 percent of its current EV).

With increasing volumes, HSBC sees the potential for quite an improvement in profitability as well. Blinkit and Swiggy Instamart were almost neck-and-neck in hyperlocal GOV for H12022 but HSBC is positive on Blinkit’s growth as the opportunity is large and the company is adding new SKUs (stock keeping units).

Risks

1. Growth in FD transacting users may be slower than expected.

2. Zomato's equity investments in start-ups may not generate value.

3. Competition in grocery and other hyperlocal areas may outperform Zomato and its investee companies such as Blinkit.

Estimates

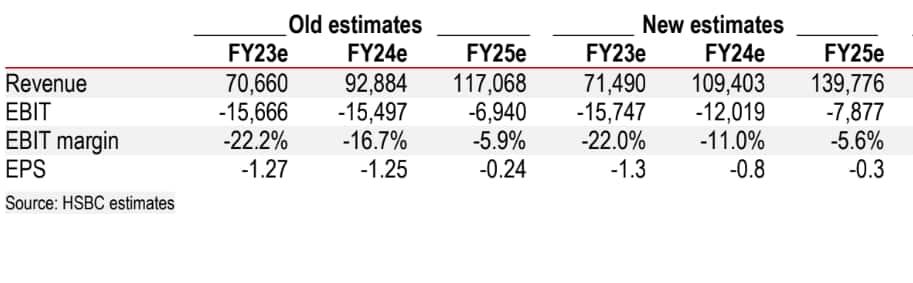

The brokerage said that its revenue estimates have changed as it factored in higher revenues for Blinkit and Hyperpure. It expects both these verticals to grow at a much faster pace over the short term.

Source: HSBC

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

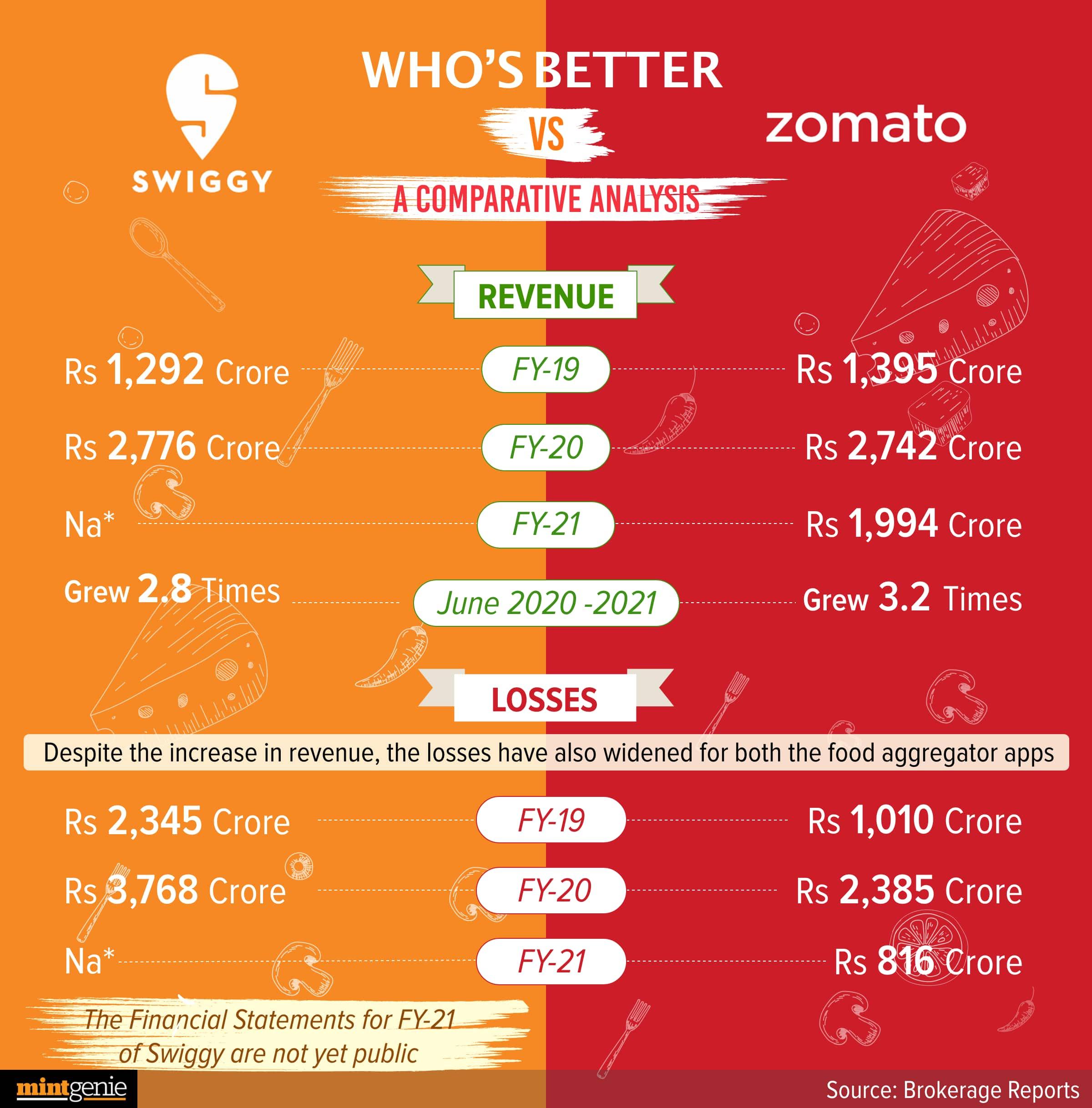

Who's better: Swiggy vs Zomato

First Published: 22 Mar 2023, 02:35 PM IST