Last week, Adani Group completed the acquisition of the cement major Ambuja Cements and its subsidiary ACC. Both these stocks surged on Monday jumping 11 percent and 4 percent, respectively. They were also up around 2-3 percent in today's trade, extending gains from their previous session. The sentiment was also lifted on reports that Adani Group also plans to infuse ₹20,000 crore into the firm to accelerate growth.

Despite that, foreign brokerage house Morgan Stanley maintained its underweight rating on both stocks. As per the brokerage, there is still no clarity around the end-use of the fund infusion.

"This will drive near-term volatility for the industry, but is net positive in the medium term,” it said.

The brokerage, in its latest report, discussed the implications of the fund infusion announcement for both Ambuja Cmenets as well as ACC and the overall cement industry. It remains underweight on both Ambuja and ACC till more details are in.

Adani Group has bought Swiss major Holcim’s stake in Ambuja Cements for $6.4 billion. The combined market capitalization of Ambuja Cements and ACC is $19 billion as on date. With this acquisition, Adani is now India's second largest cement manufacturer. The new promoters also plan to infuse ₹20,000 crore more in Ambuja Cements through preferential allotment of warrants.

As per the filing, Ambuja Cements has sought approval for allotment of preferential allotment of 47.74 crore warrants at a price band of ₹418.87 to Harmonia Trade and Investment Ltd, a promoter group entity, totaling ₹20,001 crore in one or more tranches.

Post the acquisition, Adani Group's stake in Ambuja is at 63.2 percent ACC while ACC is at 56.7 percent. Both companies have also changed their management post the acquisition. Gautam Adani took over as chairman of Ambuja Cements’ board, while his elder son Karan was appointed chairman and non-executive director at ACC.

Implications of the capital raise

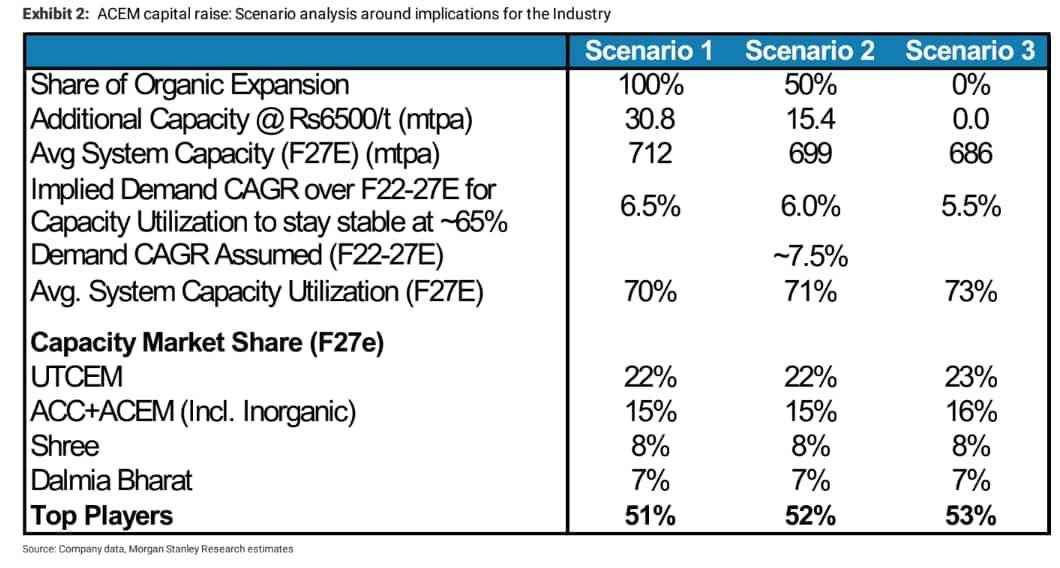

As per the brokerage, ACC + Ambuja Cements have a combined capacity of 68 mtpa, which should move to 80 mtpa by F24, assuming current expansion plans are on track. Deals over the past few years have materialized at an average of ₹6,500/ton – assuming the same cost of setting up a new plant/deal value going forward; ₹20,000 crore capital could drive 31mtpa additional capacity, taking their combined capacity to 111 mtpa”.

However, the brokerage warned that the commissioning of new capacity and normalization of utilization levels from new capacity takes time (overall 4-5 years), and hence there would be a limited impact on industry utilization rates in the medium term.

It further said that as per estimates, ACC + Ambuja could add another ₹10,000 crore free cash flow (FCF) over CY2022-24, implying another 15 mtpa expansion opportunity, which would take overall capacity to 125 mtpa. The brokerage noted that it doesn’t yet have clarity with respect to organic/inorganic expansion plans, but it looks at various scenarios that could play out:

Scenario 1: Using 100 percent capital infusion for organic expansion – This scenario would be relatively negative for the industry as it would add 31 mtpa capacity over time, and would imply a 6.5 percent demand CAGR over the next 5 years to sustain capacity utilization levels at current levels, it estimated.

Scenario 2: Using 50 percent capital infusion for organic expansion and 50 percent for inorganic opportunities – This scenario would be relatively neutral for the industry as it would add 15 mtpa capacity to the industry over time, and would imply a 6 percent demand CAGR over the next 5 years to sustain capacity utilization at current levels, predicted the brokerage. Based on our demand estimates, capacity utilization would move to 71 percent by F27 under this scenario, it added.

Scenario 3: Using 100 percent capital infusion for inorganic opportunities – This scenario would be relatively positive for the industry as it wouldn’t add any capacity and would imply a 5.5 percent demand CAGR over the next 5 years to sustain capacity utilization levels at current levels, forecasted the brokerage. Under this scenario, industry capacity utilization would improve at a much faster pace to 73 percent by F27, it added.

As for the implications of the fund infusion plan, Morgan Stanley noted that the change in promoters and organic/inorganic expansion could pave the way for improved margins over time, led by various cost synergies and operating leverage opportunities. But we need to wait and see how that plays out, it added.

"Over the next couple of years, however, ACC+ACEM's volume growth will lag larger peers given the high starting point of capacity utilization rates for them. Moreover, current cost structures for both ACC and ACEM will keep medium-term profitability in check”.

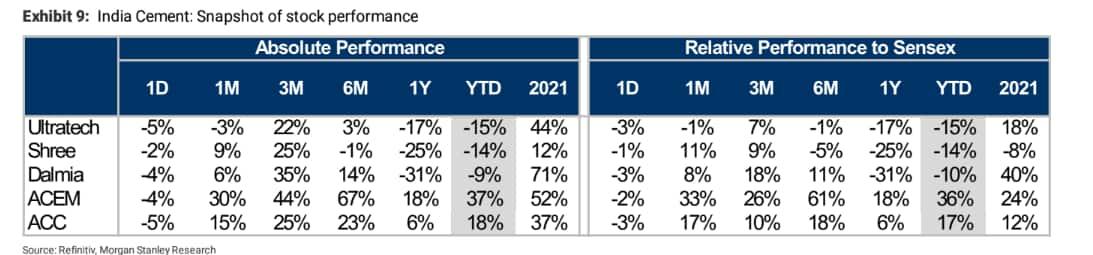

Morgan Stanley further added that ACC and Ambuja shares have outperformed peers YTD and current valuations are not cheap relative to peers, limiting any re-rating triggers and hence upside potential.

On a YTD basis, Ambuja Cement has jumped the most among peers, up 37 percent followed by ACC, up 18 percent. Meanwhile, UltraTech Cements, Shree Cements and Dalmia Bharat have given negative returns in this period.

Analysing the effects of this on the sector as a whole, Morgan Stanley said that it is a net positive on the industry in the medium term. The firm adds that unlike in the earlier upcycle of 2010, this time capacity addition is largely concentrated with larger players.

"This lowers the risk of unjustified capacity additions in this cycle, in our view, and thereby lowers the risk of a price war. This should drive steady improvement in utilization rates, which should translate into higher profitability. However, Ambuja now has the power to drive industry dynamics, and any announcement could create volatility for peers in the near-term," it said.

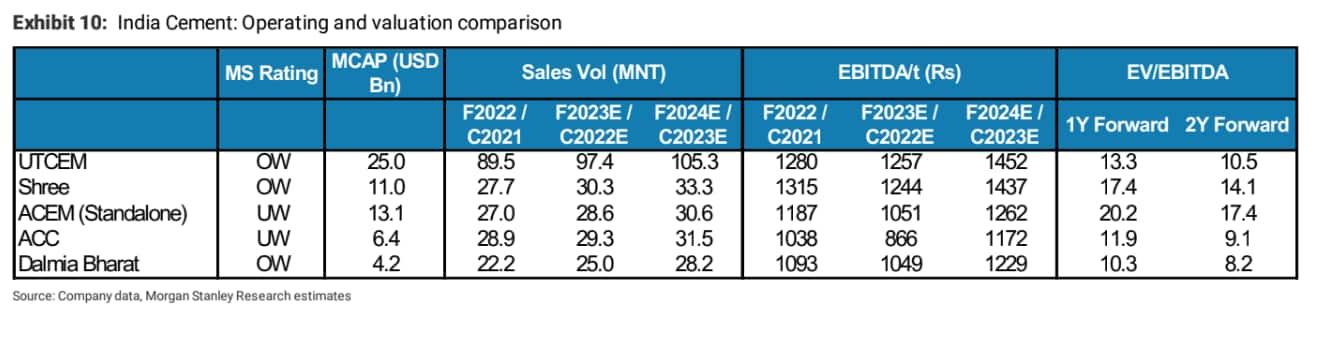

However, in the sector, MS is underweight only on Ambuja and ACC. It remains overweight on UltraTech, Shree and Dalmia Bharat.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.