After a massive rout in Adani Group stocks post the Hindenburg report, domestic brokerage house JM Financial has initiated coverage on Adani Ports and Special Economic Zone (APSEZ) with a ‘buy’ call and a target price of ₹800, implying a potential upside of 15 percent.

The stock fell 25 percent in the month of February after Hindenburg Research, on January 24, 2023, claimed that the Indian giant had participated in a clear stock manipulation and accounting fraud scheme over decades. However, it has recovered, rising over 17 percent in March till date.

The brokerage pointed out that APSEZ has delivered supreme market share gains in India in the past decade (at least 10 percentage points (ppt) gain in total share at 24 percent and over 16 ppt gain in container cargo to 43 percent market share) and is expected to sustain that in future with organic and inorganic growth.

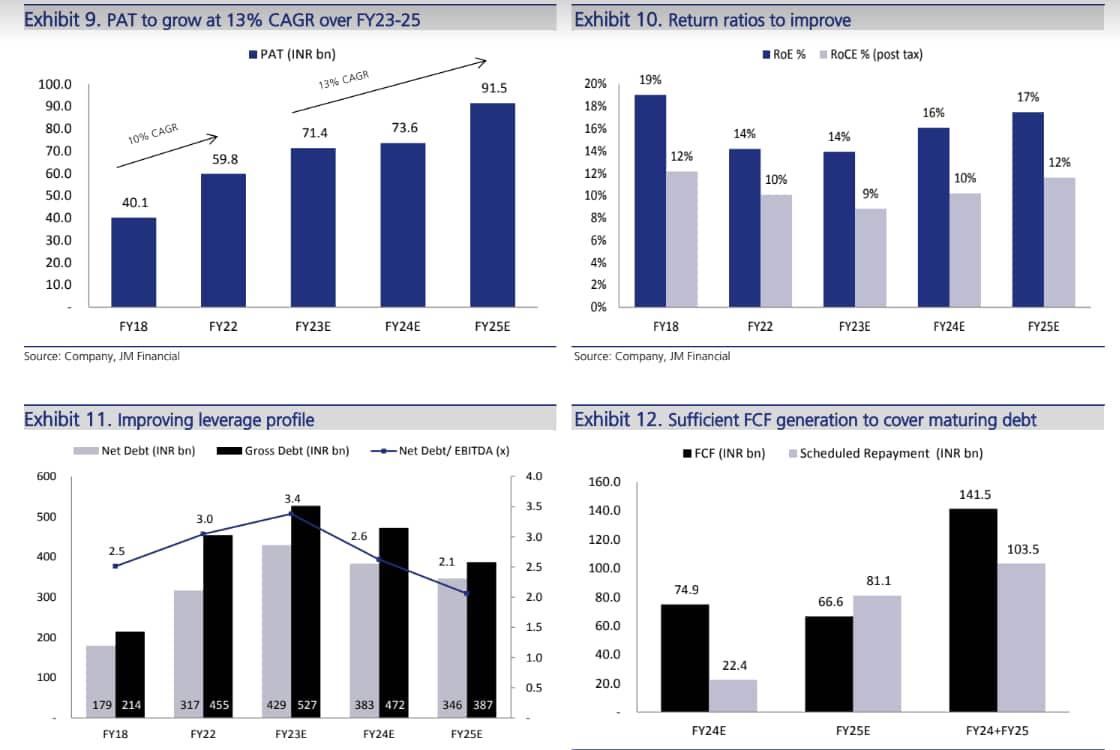

It estimates APSEZ to post 16 percent CAGR in volume (445 mnt in FY25 vs management guidance of 500mnt), translating into revenue, EBITDA and PAT CAGR of 18 percent, 15 percent, and 13 percent, respectively in FY23-25.

"We estimate APSEZ to generate cumulative operating cash flow of ₹26100 crore in FY24-25 and have a capex of ₹12000 crore, resulting in ₹14000 crore of free cash flow, substantially higher than its debt-repayment obligations ( ₹11000 crore). We specifically call out the following: a) strong balance sheet (net debt/EBITDA of less than 2.1x in FY25; net debt/equity of less than 0.7x in FY25), b) adequate debt/service coverage ratios, and c) over 90 percent of APSEZ’s forex debt being fixed coupon (thus protected from market volatility) and more than covered by its foreign currency revenue," it further stated.

Investment Rationale

Port additions: Starting with Mundra port in 1999, APSEZ has grown from being a single port operator to India’s largest port developer and operator today with 13 ports and terminals with 610 million tonnes (mnt) of operating capacity. It offers a wide range of services such as ports, port infrastructure (including marine services such as anchorage, pilotage, tug pulling, berthing), SEZs, and logistics under one umbrella, noted JM.

It's India’s largest private port company and is determined to become the world’s largest private-sector port by 2030. It has demonstrated its ability to successfully construct /acquire assets in India and create significant value for stakeholders. On the back of aggressive expansion in logistics (container/bulk/warehousing), APSEZ is transforming into India’s largest integrated transport utility, providing end-to-end logistics solutions to its enormous customer base, added JM.

As per the brokerage, its CMP does not fully capture APSEZ’s market leadership and transport utility characteristics.

Consistently gained cargo market share: The brokerage further pointed out that APSEZ has consistently outpaced all-India cargo growth rates by growing at a CAGR of 12 percent over FY15-22 vs the all-India growth rate of 3 percent. Consequently, its market share has increased from 14 percent to 24 percent during this period, it added.

Even on the container cargo side, APSEZ has grown at a CAGR of 16 percent vs the all-India growth of 7 percent over FY15-22, leading to its market share rising from 24 percent to 43 percent.

APSEZ remains on track to achieving its guided all-India market share of 25 percent. While Mundra port’s cargo market share has risen modestly at the aggregate level, container market share has soared by 10 ppt over FY16 to 34 percent in FY22, observed the brokerage.

Strong volume growth: After commencing its operations at Mundra in 1999, it took 14 years for APSEZ to cross 100mt of annual cargo volume. But it was able to double that to 200mt in only 6 years and increase cargo volume by another 100mt in a mere 3 years on the back of best-in-class assets and the integrated nature of the business (such as providing end-to-end services) and strategic acquisitions, informed JM. In the past decade, APSEZ’s cargo volume has grown at a CAGR of 18 percent (+15 percent over FY18-22). The brokerage estimates APSEZ to repeat the same feat in just over 2 years.

A significant contribution from sticky cargo: "Over the years, APSEZ has focused on improving the stickiness of cargo through long-term contracts, cargo diversification, and by bringing together shipping lines. This has enabled it to deliver stable industry-leading cargo growth. As per the management, sticky cargo is cargo that has high repeat visibility and something that cannot be taken away easily. Liquids and coal are prime examples of sticky cargo; certain container routes too are classified as sticky," explained JM.

Over FY17-18, APSEZ boasted over 60 percent sticky cargo in its overall mix. Of the sticky cargo volume, Mundra port contributed over 80 percent. With the addition of new assets (especially over the past 2-3 years), the sticky cargo volume mix has been trending downwards. However, as these assets mature, there will be an increase in sticky cargo volume from these assets, believes the brokerage.

Strong track record: The brokerage further pointed out that APSEZ has time and again demonstrated its capability to turn around an asset post acquisition by putting in place a strong operating process. This is evident from the increase in EBITDA margin at a) Dhamra Port - 67 percent in FY22 (45 percent on acquisition in 2015), and b) Krishnapatnam port – 69 percent in FY22 (55 percent on acquisition), said JM.

Strong operational cash flow: APSEZ has consistently generated strong operating cash flows in FY18-22 (CAGR of 15 percent), highlighted JM. It further noted that during this period, APSEZ had embarked on an acquisition spree. Going ahead, APSEZ is likely to focus on sweating the acquired assets, which will sustain strong cash flows in the coming years as well. It estimates cash flow from operations to grow at 32 percent CAGR over FY23-25.

"This, we believe, will be used to fund capex and reduce debt. APSEZ continues to be on the lookout for opportunities outside India via the joint venture (JV) mode with a strong local partner, either in South Asia, Southeast Asia, Middle East, and Africa," said the report.

Improving ratio profile: Although absolute debt has gone up (for funding acquisitions), return profile has also improved, highlighting the company’s strong execution capabilities, mentioned JM. Net Debt/EBITDA has been fairly stable at 3-3.3x while FFO (Fund From Operations) ratios have improved. FFO/Gross Debt has improved from 17 percent in FY17 to 22 percent as on 9MFY23 while FFO/Net Debt has improved from 19 percent to 22 percent in the same period, stated the brokerage.

However, key risks include any significant slowdown in India and adverse developments in group companies, warned the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.