Vedant Fashions Ltd. (VFL) founded by Kolkata-based first-generation entrepreneur Ravi Modi is a play on the branded Indian wedding and celebration wear (IWCW) market, which seems relatively less price-sensitive. Its flagship brand Manyavar commands dominant position in the branded IWCW market and has emerged as a ‘category leader’ and a ‘brand of first recall’.

Amid Diwali season, Vedant Fashions set to grab a pie in the large untapped branded apparel market

TL;DR.

Currently, VFL operates through 595 franchisee-led EBOs (including 55 shop-in-shops) across 223 cities and towns in India and 12 overseas EBOs with retail footprint of over 1.3mnsqft. Read further to know more

First-mover advantage, scale efficiencies and no discounts on Manyavar allows VFL to enjoy significantly higher gross margin (75% on net end-customer sales) vs most other listed brands (which operate at 45-60%). This is the key differentiation enjoyed by VFL vs peers, which in turn results in higher profitability (>30% EBITDA margins pre-Ind AS116), >40% RoIC / RoCE and superior FCF generation.

Largest company in India in men’s Indian wedding & celebration wear by Revenue, OPBDIT1 & PAT. Commands dominant position in conventionally unorganized market Manyavar brand is category leader in branded Indian wedding & celebration wear market with pan-India presence.

Growing presence in women’s Indian wedding & celebration wear with Mohey - Largest brand by number of stores with pan-India presence. Retail footprint (Q1 FY23) of 1.3 mn sq. ft. across India (590 EBOs2 in 228 cities & towns in India) and Overseas (13 EBOs in USA, Canada & UAE).

Company's diversified brand portfolio

Company's diversified brand portfolio

The business risk profile is underpinned by the company’s strong brand in the ethnic wear segment and large retail footprint through more than 595 exclusive brand outlets (EBOs) across the country. This enabled the company to generate turnover of ₹1,008 crore in fiscal 2022 despite the second and third waves of the pandemic. Demand for kurtas and sherwanis was sustained during the festival and marriage seasons even during the pandemic.

Smart business model

VFL aims to deliver a uniform country-wide experience to customers through a combination of its strong retailing proposition supported by its omni-channel network and the strength of its brands. Given the company’s seasonagnostic designs and aspirational brand appeal, it employs consistent pricing for its products across India.

It has not offered any end-of-season sales or discounts for its Manyavar brand. Besides enhancing its leadership position in Manyavar, the company intends to upsell Twamev, cross-sell Mohey and target a sizable number of midmarket weddings and other celebrations via Manthan.

Large growing Indian wedding and celebration wear market

This market is driven by 9.5mn-10mn weddings each year. Multi-day and multi-event wedding celebrations, increasing tendency of wearing-appropriate celebration wear for festive events, shift from tailored to ready-to-wear celebration apparels, addition of Indo-western wear, increased penetration in tiers-2&3 cities, etc. are other growth drivers.

VFL aims to expand it footprint in India

Currently, VFL operates through 595 franchisee-led EBOs (including 55 shop-in-shops) across 223 cities and towns in India and 12 overseas EBOs with retail footprint of over 1.3mnsqft. Through its cluster-based expansion strategy, the company intends to add EBOs in both its existing geographies as well as new geographies (identified 150 new towns / cities) and aims to double its national footprint over the next few years.

Key trackable indicators

Network expansion, SSSG, gross margin (on end-customer sales), OCF or OCF to EBITDA, RoCE

Like-to-like financial comparison in apparel retail is becoming relatively difficult, as different companies follow diverse business models like COCO, COFO, FOFO, etc. coupled with varying accounting treatments such as outright sales or ‘sale on return’ (SOR) basis and Ind-AS116 treatment.

For example, VFL follows the outright sales model for its sales made to franchisees (and not when actual sales happen with end-customers). This may result in higher receivables days and timing difference on profitability (which eventually nullifies over a period), especially for the new stores opened during the year.

Global Scenerio

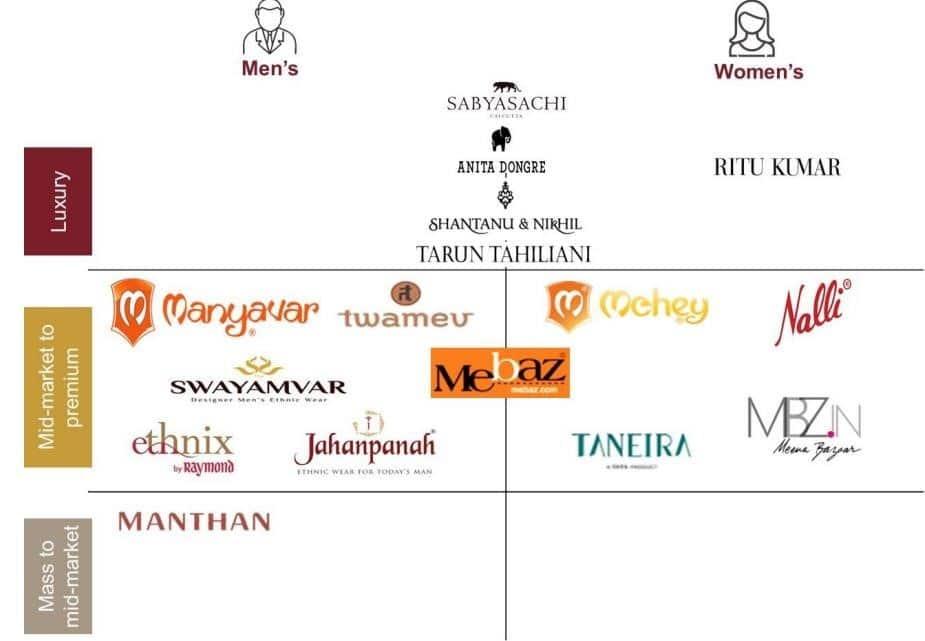

The share of branded apparel retailers within Indian wedding and celebration wear market is currently low, at approximately 15% to 20%, indicating huge potential for branded players. Players, such as Vedant Fashions Limited (VFL) with its brands Manyavar, Mohey, Twamev, Manthan and Mebaz, and brands such as Nalli’s, Jahanpanah, Ritu Kumar, and Neerus command a dominant position due to their broad variety, latest designs, better fitting and trial services and better overall purchase experience. Given low penetration levels, there is huge potential for branded players beyond metros and tier-I cities, along with scope for new brands.

For both men’s and women’s Indian wedding and celebration wear, the branded section grows at differential rates, with the branded market expected to grow at a faster rate due to an increase in availability of various pan-India and regional brands providing consistent quality merchandise with attractive and contemporary designs at uniform pricing along with superior customer experience.

Hence, the branded segment is set to grow at a CAGR of 18% to 20% between FY20 and FY25 and account for 28% to 32% of the Indian wedding and celebration wear market, as per CRISIL.

Branded players to continue to gain market share in the long-term. Considering the longer term trends for Indian wedding and celebration wear market, branded players have better recognition, they remain at the edge of fashion trends and give a premium experience to the consumers.

Branded players have expanded their footprint beyond tier-II cities. Players such as VFL, with their brands Manyavar and Mohey, are also present pan-India with a popular brand portfolio, enabling major brands to gain market share.

Key brands predominant in Indian wedding and celebration wear and their offerings across segments

Key brands predominant in Indian wedding and celebration wear and their offerings across segments

Shuchi Nahar is a Certified Research Analyst. She can be found on Twitter at @shuchi_nahar

Note: This article is for informational purposes only. Please speak to a SEBI-registered investment advisor before making any investment relatedinvestment-related decision.

Impact of bond yields on stock markets

First Published: 12 Oct 2022, 01:56 PM IST