On the back of a cooling inflation, strong earnings growth, steady returns over the years and expanding EBITDA, domestic brokerage house Anand Rathi has initiated coverage on the FMCG sector with 4 ‘buy’ calls and 2 ‘hold’ calls.

Anand Rathi initiates coverage on FMCG with 4 'buy' calls; explains impact of RIL's entry

TL;DR.

On the back of a cooling inflation, strong earnings growth, steady returns over the years and expanding EBITDA, domestic brokerage house Anand Rathi has initiated coverage on the FMCG sector with 4 ‘buy’ calls and 2 ‘hold’ calls.

"We believe FMCG companies will continue to deliver steady returns in coming years. This will be driven, however, by earnings growth rather than multiple expansions in most cases. We like structural growth stories in mid-caps such as Zydus Wellness and Emami where valuations are reassuring, with strong earnings growth potential. Given the sharp fall in input costs, however, we expect a strong earnings rebound in the next one year for companies with links to crude or palm oil. Thus, HUL and Godrej Consumer could offer good returns in a year. We recommend Buys on Zydus Wellness and Emami in mid-caps, and on HUL and Godrej Consumer in large-caps. We have a Hold rating on Marico and Dabur," said the brokerage.

Investment Rationale

Steady growth momentum: The brokerage observed that volume growth in the FMCG sector, over the last 10-15 years, has slowed to mid-single digits in FY15-22, from double-digit in FY10-15. While the shift toward the formal market, post-GST and de-monetization, has aided FMCG companies, it believes market development across many categories has been interrupted by macro slowdowns and a lack of initiatives by FMCG companies.

However, EBITDA margins have continued to rise aided by operating leverage, cost-efficiency measures, premiumisation and consolidation of market share with larger players, it added. It expects such mid-single-digit volume growth momentum to endure while EBITDA margins could expand (despite being near peaks) as inflation cools and cost-saving benefits arise.

Rural upswing: The brokerage further stated that it expects some swelling in demand aided by the generally good monsoon last year, higher crop prices, government schemes and spending during the coming election. Also, the negative base of the last 6-8 quarters helps toward higher rural growth, it added.

Reliance entry: According to Anand Rathi, Reliance entry, similar to Patanjali entry, could have implications for FMCG volume and revenue growth. It informed that at the peak of the Patanjali-driven consumer shift, FMCG volumes decelerated to low single digits or negative (vs. mid-to-high single digits earlier).

Reliance’s current organic and inorganic portfolio is tilted towards value-added commodities (staples), foods and home care, thus, initially, the brunt of its entry is likely to be borne by these categories, which are likely to provide some protection to large listed FMCG companies (Dabur, Emami, Marico, GCP, Nestle) in personal care, technology/regulatory intensive and premium portfolios, cautioned the brokerage.

It also warned that 50 percent of HUL's portfolio could be directly impacted; a large part of its soaps & detergents portfolio straddles the mid and premium segments. It expects a limited implication initially, but this could turn out to be a cause of concern as Reliance Consumer scales up operations, especially in soaps & detergents.

It also sees FMCG brand stickiness, especially in premium and technology-driven categories, limiting the impact, with most leaders in their categories retaining their position over the next 5-10 years.

To explain the same, the brokerage has cited ITC’s entry into several categories such as soaps, biscuits, noodles, etc. between 2003 and 2010. Similar to Reliance’s entry now with deep pockets, ITC’s entry hadn’t had a significant effect on the sector, with just a minor effect on volumes, revenues or market shares of large FMCG companies. Today, after 12-20 years, ITC hasn’t dislodged leaders in FMCG categories.

In fact, it had to restrict its operations in personal care due to heavy losses and little acceptance, it pointed out.

"Thus, we infer from both the ITC and Patanjali episodes that brand stickiness in FMCG is strong, and it is difficult to dislodge leaders in any category. Hence, we believe the entry of Reliance could, in the short to medium term, shift the balance in FMCG in volumes and revenue momentum. It is unlikely, however, in the next 5-10 years to dislodge category leaders," it explained.

Valuations

FMCG companies have reported more than a 10x jump in market cap (or a 16.8 percent CAGR) over the last 15 years. The strong returns have been aided by 11 percent revenue and 12.5 percent profit CAGRs. The rest of the upside could be attributed to the re-rating of multiples, said the brokerage.

It expects the six FMCG companies – Hindustan Unilever, Dabur, Marico, Godrej Consumer, Emami, and Zydus Wellness – to average 10 percent/14.7 percent revenue/earnings CAGRs over FY23-25.

Stocks

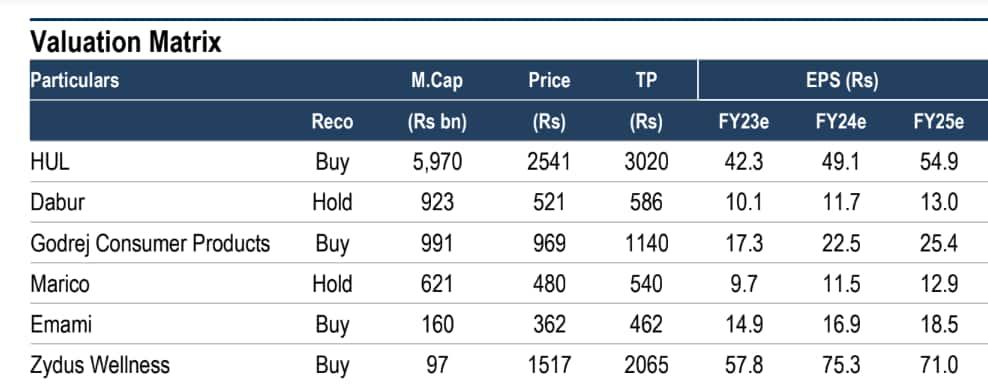

HUL: Over the last 10 years, it has delivered 8.5 percent/13.8 percent revenue/EBITDA CAGRs, driving an 18.4 percent returns CAGR, said Anand Rathi. With consistent investment in digitisation, products and with a future-ready organisation, it expects HUL's industry-leading growth to endure. It has initiated coverage on the stock with a Buy and a 12-month TP of ₹3,020, indicating an upside of 19 percent.

Dabur: As per the brokerage, Dabur’s natural & herbal positioning has helped it diversify to beauty and baby care, however, this has diluted its focus even as it provides resilience in slowdowns (Covid-19). This reflects in its 7.5 percent/10.1 percent revenue/EBITDA CAGRs over the last 10 years, driving a 17.7 percent CAGR in its market cap, said the brokerage. It has re-initiated coverage on the stock with a Hold recommendation, at a 12-month TP of ₹586, indicating an upside of 12 percent.

Godrej Consumer: Godrej Consumer has begun the transformation to a lean and agile organization, focusing on customers, said the brokerage, adding that simplification of its organisation structure across regions, digitisation and cost-efficiencies should raise its revenue and margins. Also, the recent fall in input costs should aid currently depressed margins and boost earnings. It believes the firm is a good tactical bet from a 12-18 month perspective due to potential earnings. It recommends Buy with a 12-month TP of ₹1,140, indicating a 17 percent upside.

Marico: Having transitioned from a mere edible oil manufacturer to a multi-product company over the years, Marico is focusing on four “D”s (Diversification, Distribution, Digital, Diversity) for its next leg of growth, said the brokerage. Its consistent emphasis on volume growth ahead of margins has delivered steady 9.7 percent/ 13 percent revenue/EBITDA CAGRs over the last 10 years. Consequently, investors have been rewarded with a 20 percent returns CAGR, it added. The brokerage has re-initiated coverage on the company with a Hold and a 12-month TP of ₹540, implying a 12 percent upside.

Emami: As per the brokerage, Emami’s niche portfolio and leading position afford it an enviable gross margin in the industry. While Covid-19 hurt its mass personal-care products, Anand Rathi expects a swift recovery aided by a rural revival. Further, its efforts in distribution, D2C brands, digital venture and cost-saving steps should give it steady 9.6 percent/15.2 percent revenue/EBITDA CAGRs over FY23-25, it forecasted. It has re-initiated coverage on Emami with a 12-month TP of ₹462, indicating an upside of 27 percent.

Zydus Wellness: The brokerage has initiated coverage on the stock with a target price of ₹2,065, indicating an upside of 36 percent.

Source: Anand Rathi

First Published: 03 May 2023, 03:54 PM IST