Asian Paints and Indigo Paints are two major paint companies in the country. However, one is quite older than the other. While Asian Paints was founded in 1942, Indigo Paints was incorporated in 2000. The latter got listed on the stock exchanges only in February last year. However, despite the recent listing, the firm has emerged as the fifth-largest player in the Indian decorative paints industry. Let's see between the classic Asian Paints and the newbie Indigo Paints, which is a better paint stock to bet on in the long term.

Asian Paints vs Indigo Paints: Which one should you buy for long term? MintGenie asks 3 analysts

TL;DR.

Asian Paints and Indigo Paints are two major paint companies in the country. However, one is quite older than the other. Let's see between the classic Asian Paints and the newbie Indigo Paints, which is a better paint stock to bet on in the long term.

Stock price trend

While Indigo Paints has shed 42 percent in the last 1 year, paint major Asian Paints is down just 1 percent in

this period. On a YTD basis, Asian Paints had shed nearly 9 percent whereas Indigo Paints has lost over 38 percent.

Indigo Paints has lost 9 percent just in November following a 4 percent decline in October and an 11 percent fall in September. However, in August the stock surged 20 percent.

Meanwhile, Asian Paints has been flat in November, down only half a percent following an 8 percent decline in October. It surged the most in July during the year, up 24 percent.

About the firms

Asian Paints together with its subsidiaries, manufactures, sells, and distributes paints and coatings for decorative and industrial use in India and internationally. It operates in Paints and Home Improvement segments. It was founded in 1942 and is headquartered in Mumbai, India.

Indigo Paints Limited engages in the manufacture and sale of decorative paints in India and internationally. It offers interior and exterior emulsions, enamels, putties and primers, and sleek wood coatings, as well as other products, including leakproof emulsions, aluminium paints, stone and tiles paints, roof paints, and stainers. The company was incorporated in 2000 and is headquartered in Pune, India.

Indigo Paints stock price trend

September quarter (Q2FY23) earnings

Asian Paints reported a 31.3 percent year-on-year (YoY) rise in consolidated net profit (after minority interest) at ₹782.71 crore in the September quarter compared with ₹595.96 crore in the corresponding quarter last year aided by price hikes. The paints maker said its consolidated sales for the quarter rose 19.8 percent to ₹8,430.60 crore from ₹7,036.51 crore in the year-ago quarter. The company's Earnings Before Interest, Taxes, Depreciation, and Amortisation, or EBITDA grew 35 percent to ₹1,227 crore as against ₹904.5 crore YoY. EBITDA margins expanded 180 basis points to 14.5 percent.

Managing Director & CEO, Amit Syngle, said: The domestic decorative business showed resilience to deliver a double-digit volume growth and healthy value growth despite subdued demand conditions, impacted by the extended monsoon. The business focus on the top line is evident from the double-digit compounded growth rates in volume and value sales for the sixth quarter in a row."

Indigo Paints' profit nearly tripled in the September quarter. The firm posted a net profit of ₹37.09 crore, up 173.73 percent year-on-year (YoY) against ₹13.55 crore in the corresponding quarter of the last year. Its net revenue from operations for Q2FY23 jumped 23.71 percent YoY to ₹242.61 crore against ₹196.11 crore in the corresponding quarter of the last year. Meanwhile, EBIDTA (excluding other income) for the quarter under review came in at ₹33.77 crore against ₹23.38 crore in Q2FY22, marking an increase of 44.47 percent YoY.

The company expects a much sharper increase in profitability parameters in future quarters with comfortable margins due to stabilising raw material prices and an aggressive growth focus. The strategy of increasing their presence in the Tier-1 and Tier-2 cities is expected to yield rich results in the upcoming quarters.

Which is a better investment?

Vinit Bolinjkar, Head of Research, at Ventura Securities believes that while Asian Paints has the highest touch points and is undoubtedly the best paint stock for the long term, one can prefer to invest in Indigo paints in the short term given the stock has corrected a lot (50 percent from 52-week high) and is available at comparatively lower valuations (33.2x FY24 v/s ~60x FY24 for Asian paints).

Indigo has also innovated in many paint categories and is 1st player to introduce metallic paint, floor paint, unique ceiling coat paint, etc, it added.

Preeyam Tolia, Senior Research Analyst, Axis Securities has also picked Asian Paints between the two.

"Asian Paints is well placed amongst its competition, as its recent initiatives of transitioning from 'share of surface' to 'share of space' and backward integrating critical raw material coupled with its strong distribution network makes it stronger in the long term, despite new players such as Grasim and JSW paint entering into the paint industry. We expect the entering of new players will impact smaller and regional players such as Indigo more, compared to the large players such as Asian Paints," explained the brokerage.

Tolia noted that Asian Paints is in the right direction to foolproof the next leg of growth and protect the market share in the long run. Moreover, its recent acquisition of Weatherseal (Doors & Windows) and White Teak (Lighting), along with its presence in ESS ESS (bath) and Sleek (Kitchen), makes Asian Paints a clear leader in the Home space category in the long term, Tolia added.

"Although scaling up of new Home Decor business and strengthening the backend will take time to bear fruits in the near term, on a long-term basis, we expect Asian Paints will get out stronger than its peers," added the market expert.

Deepak Jasani, Head of Retail Research at HDFC Securities had also picked Asian Paints between the two.

"Asian Paints plans to invest ₹6750 crore over next three years in expanding production capacity, backward integration of white cement as well as acquisitions like Weatherseal, White Teak and Harind, a nano-technology company in surface coatings. The savings from backward integration (additional 400 bps gross margin) will likely allow Asian Paints to price its products competitively as well as offer better products. We believe most smaller players will not be able to invest in backward integration and it should allow Asian Paints to retain/gain market share," he rationaled.

He, however, added that even though Indigo Paints is expected to outperform the industry in FY23-24E, he remains cautious on the company’s long-term growth trajectory and values it at a discount to the likes of Asian Paints and Berger, owing to the uncertainty arising from Grasim’s launch, starting from FY25E. Additionally, Indigo derives a significant portion of its revenue from the state of Kerala, which contributed 28 percent to FY22 revenues. Thus, it is significantly exposed to any crisis in Kerala unlike Asian Paints which has a strong pan-India presence, he further cautioned.

"We believe that (1) the rise in competitive intensity poses risk to Indigo’s industry-leading gross margins and that (2) smaller players are more vulnerable to Grasim’s market entry and the resultant aggression from Asian Paints. This could potentially lead to lower trading multiples for Indigo. On the other hand, we believe that valuation for Asian Paints will always be at a premium to other consumer peers, as it has consistently delivered strong volume-led growth, maintained market leadership, continuously generated robust cash flows, sustained a healthy dividend payout ratio, maintained decent ratios and is now making big investments on capacity expansion and backward integration," Jasani noted.

Asian Paints stock price trend

Outlook of the sector

Going ahead, Tolia believes there will be some challenges to profitability across the industry despite a fall in key raw material prices, as rupee depreciation will likely have an impact on the margins in the short term. Moreover, the entering of new players in the paint segment will increase the overall competitive intensity, which will have initial hiccups on both the top line and bottom across the industry, he added.

Bolinjkar, on the other hand, noted that the paint sector has mostly been an oligopoly market with the top 4 players cornering more than 80 percent market share. The players have also behaved rationally and there had been any instances of a price war in the past, however, with new players like JSW, Grasim, JK Cement and Astral entering the market, there could be a price war going ahead and hence margins can come down for the existing players, he warned.

In terms of outlook, Bolinjkar is bullish on the sector and expects an 11.2 percent CAGR in revenues of organized players over FY22-31 with decorative paints expected to grow at 11 percent CAGR (7.5 percent volume growth and 3.5 percent price/mix).

Finally, Jasani remains cautious on the sector. "As the industry presents significant entry barriers, the Indian decorative paints industry has historically been dominated by the top-4 players. However, strong volume-led growth potential, improving profitability/return ratios and rich valuations have attracted new competition (Grasim, JSW, JK Cement and Astral) in the recent past. With the entry of new players with deep pockets and massive commitments on investments, the overall industry may see a shift in demand and margin structure due to heightened competition. We remain cautious as the sector may not enjoy the higher multiples of the past," he said.

He sees India’s organized decorative paints industry is likely to register a revenue CAGR of 11 percent over FY2022-31E, driven by 7.5 percent/3.5 percent CAGR in volume (ex-putty)/price mix. The key long-term growth drivers are: (1) demographic-led rise in housing stock, (2) conversion of kutcha houses to pucca ones, (3) shortening of the repainting cycle, led by aspirations and rental housing, and (4) unorganized-to-organized shift, he added.

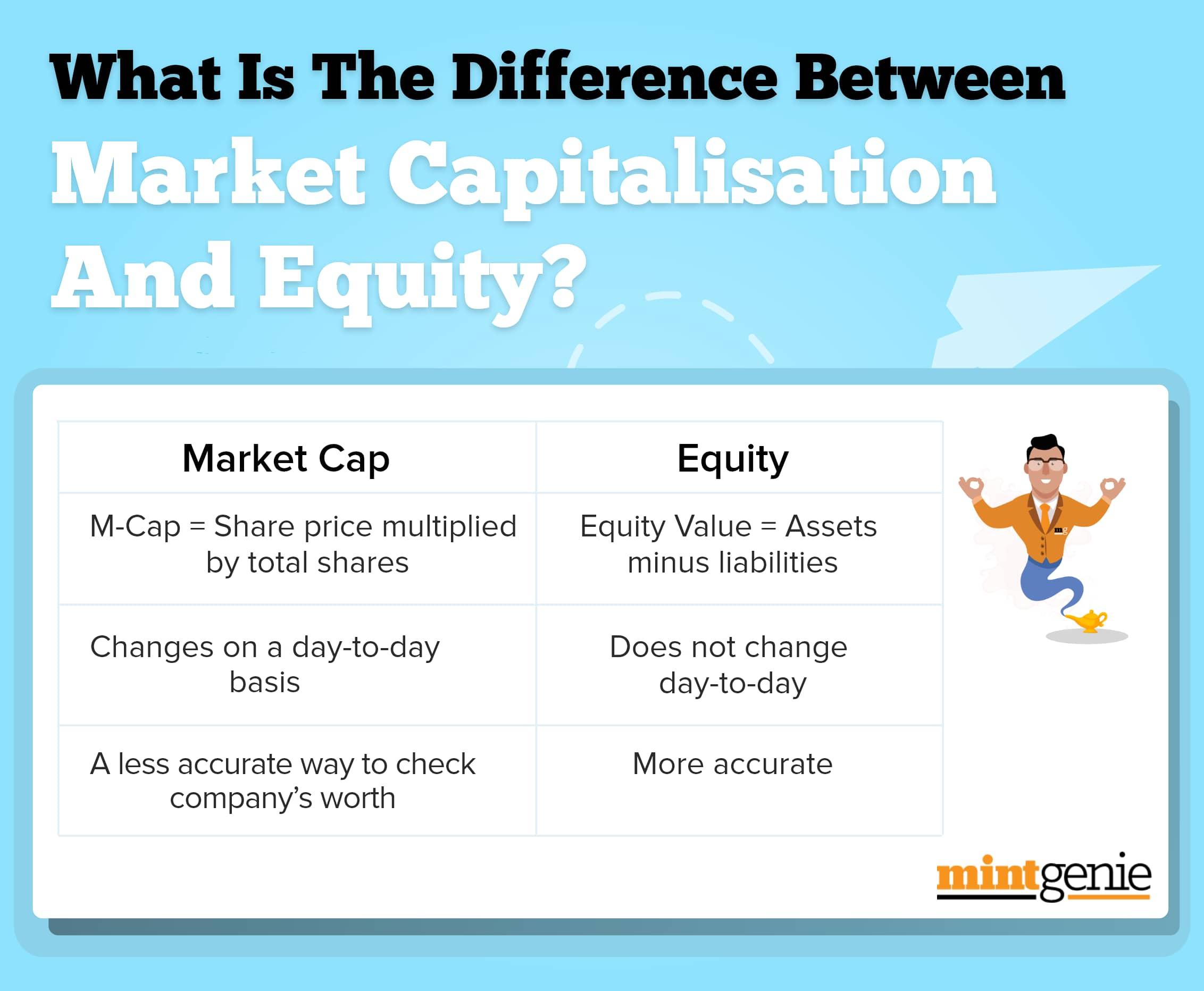

Market cap vs equity

First Published: 25 Nov 2022, 01:59 PM IST