An investor presentation made by AU Small Finance Bank on March 10, 2022 has left analysts split for a verdict. The bank outlined its strategy to execute growth and highlights its long-term objectives and roadmap.

Morgan Stanley and Motilal Oswal have an ‘overweight’ and 'buy' call on the stock, respectively, whereas Kotak Securities is unimpressed and has a ‘sell’ call with a target price cut as well. Market sentiment on the stock is ‘moderately positive’, according to a MintGenie poll and an average of 21 analysts has a ‘hold’ call on the stock.

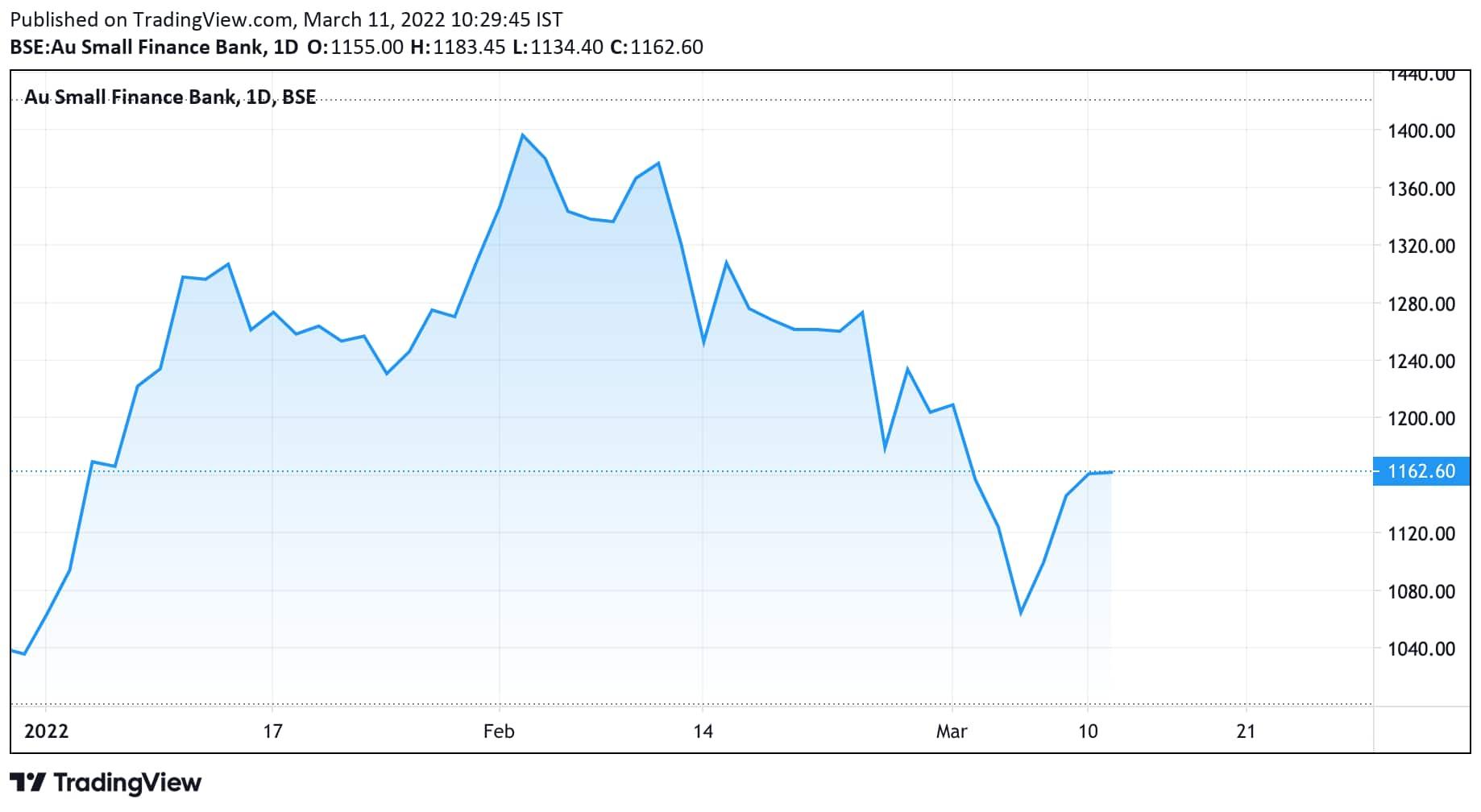

Shares of AU Small Finance Bank have jumped 12 percent in calendar year 2022 so far while the benchmark Sensex has fallen 5 percent in the same period.

The Ones Who Like The Story

Global financial firm Morgan Stanley has maintained an 'overweight' call on the stock after the investor presentation, highlighting the management's confident tone on growth, spreads and asset quality.

As per CNBC-TV18, Morgan Stanley has a target price of ₹1,675 on the stock, which is a 44 percent upside from the stock's March 10 closing of ₹1,161.60 on BSE.

The bank's presentation was focussed on two aspects- wheels, which was about the automobile industry, and home loan, which was about the bank's loan book.

Under the wheels segment, the bank highlighted that a strong push from the government for roads and other wheels-related infrastructure in Budget 2022 is a major positive for the segment. Besides, nearly five lakh electric cars sales are expected in FY27. Two-wheelers are leading the segment in electric vehicles sales while commercial vehicles and passenger vehicles will also grow.

The trend of assets under management (AUM) and gross non-performing assets (GNPA) for the wheels segment shows GNPA, at 3.4 percent, is well within range in even industry downturn while GNPA is gliding back to pre-Covid levels, said the company in its presentation. In the home loan segment, non-performing asset (NPA) stands at 0.61 percent.

Domestic brokerage firm Motilal Oswal Financial Services, which has a ‘buy’ call on the stock with a target price of ₹1,550, said in a report that the bank has been reporting a strong operating performance and robust business growth while asset quality has been particularly resilient amid a challenging economic environment.

"With an improvement in economic activity (as reflected by key economic indicators – GST collections, GDP growth, and PMI), the bank appears on track to deliver superior growth while retail deposit mix continues to improve supporting the margin profile," Motilal Oswal said.

"Collection efficiency stands healthy at 106 percent and the bank carries contingent reserves of ₹300 crore (75bp of loans), which provides further comfort. We estimate the bank to deliver nearly 35 percent earnings CAGR over FY22-24, while return on assets (RoA) and return on equity (RoE) improve to 2.1 percent and 20.4 percent, respectively, in FY24E," said the brokerage.

Brokerage firm IIFL Securities has upgraded the stock to 'add' with a target price of ₹1,320.

"Overall, we remain positive on the bank’s growth momentum going forward as well. Post recent correction and rollover of target price to FY24, we upgrade the recommendation to 'add'," IIFL said

The brokerage firm said the bank remains bullish on strong growth prospects in both auto and home loan segments with low penetration levels, increasing geographical presence and untapped opportunities in the existing markets as well. Thrust on digitalisation remains high to accelerate growth, improve efficiencies and risk management practices.

In the Wheels segment, the bank has a presence across the product spectrum; however, market share in states other than Rajasthan is low, indicating a long growth runway. In the housing loan segment, growth would be driven by deeper penetration in existing geographies (8 states) and expansion into other states where the bank already has a presence (7 states), IIFL Securities observed.

The One That Doesn't Buy The Story

However, Kotak Securities does not look convinced with the bank's growth outlook as the brokerage firm has given a 'sell' call on the stock and even cut the target price to ₹1,050 from ₹1,100.

Kotak highlighted that round two of the bank’s analyst meet focused on vehicles (nearly 40 percent of loans) and home loans (about 5 percent of loans) and largely reaffirmed the bank’s strong credit and collections-based approach towards building asset businesses.

"The underlying crux of the presentation was a re-iteration of AU’s strengths in credit and collections across both businesses, and hence probably already well-understood and appreciated, in our view. However, we do note that AU’s approach of geographic expansion beyond core markets (wheels, liabilities), penetrating deeper within the existing markets (home loans) and introducing new products (credit cards, QR) can generate long-term benefits if executed well," Kotak said.

"There is no change in view on AU’s excellent performance on growth and asset quality across cycles, however, valuations remain a constraint. Further, there are fresh near-term headwinds around crude oil/inflation and its potential impact on the vehicle book and overall growth environment (supply or demand-driven). We cut fair value to ₹1,050 (from ₹1,100) and retain our sell rating," Kotak said.