India's fourth largest private sector lender Axis Bank posted stable earnings for the June quarter (Q1FY24). The sentiment also remained positive after most brokerages retained their bullish calls on the stock.

Axis Bank: Brokerages remain bullish after Q1 results but see volatility in near term

TL;DR.

Most brokerages remained bullish on Axis Bank due to its stable performance in the Q1 despite a fall in margins. They believe that FY24 would be a relatively tough period for the lender, however, its long-term growth outlook remains strong.

In the June quarter, the private sector lender posted a 41 percent year-on-year (YoY) rise in its net profit at ₹5,797 crore versus ₹4,125 crore in the same period last year. The rise in profit was driven by higher net interest income and fee income.

Its net interest income (NII) also jumped 27 percent to ₹11,958 crore in Q4FY24 as against ₹9,384 crore in the year-ago period. Meanwhile, net interest margin (NIM) declined 12 bps to 4.1 percent from 4.22 percent sequentially. On a YoY basis, NIM rose 50 bps.

Asset quality also recovered. The gross non-performing assets (GNPA) of the bank declined to 1.96 percent as compared with 2.76 percent last year. Also, the net non-performing assets (NNPAs) of the bank fell to 0.41 percent compared with 0.64 percent last year.

What do brokerages say?

Most brokerages remained bullish on the stock due to its stable performance in the Q1 despite a fall in margins. Most experts believe that FY24 would be a relatively tough period for the lender as Citi’s cost of integration would weigh on the cost ratios, however, its long-term growth outlook remains strong.

JM Financial: The brokerage has retained its ‘buy’ call on the private sector lender but cut its target price to ₹1,040 ( ₹1,075 earlier), indicating an upside of 6.5 percent. Axis Q1FY24 earnings were aided by strong fee income and trading gains even as underlying growth trends remained a tad soft – deposits were flat QoQ and loans grew only 1.6 percent QoQ, noted the brokerage. NIMs, meanwhile, declined lesser than JM's estimates even as it expects further moderation given the continued uptick in the cost of funds.

While initial signs of success are visible, it believes it is some time away from closing the gap with larger private sector peers. Meanwhile, ability to successfully balance growth vs NIMs will lead to meaningful valuation upsides for Axis Bank, added JM. Given the long-term measures undertaken to improve the liability franchise and portfolio granularity, it now expects ROA/ROE of 1.7 percent/ 17.6 percent in FY25E.

While Axis Bank’s transformation is in the right direction, meaningful improvement in liability franchise while balancing its investment initiatives and growth ambitions will need strong execution. This, in turn, could lead to meaningful compression of the valuation gap vs larger private sector peers, said the brokerage.

Prabhudas Lilladher: The brokerage reiterated its ‘buy’ call on the stock but raised its target price to ₹1,170 ( ₹1,140 earlier), indicating an upside of around 20 percent.

Axis saw a good quarter, although core PAT was a miss due to higher opex, NII was 3 percent ahead of PLe leading to NIM at 4.17 percent, noted the brokerage. NIM boost was driven by (1) strong QoQ growth in higher margin segments (2) a deliberate slowdown in housing (3) 6 percent QoQ fall in LCR and (4) lower deposit growth of 0.6 percent QoQ, it explained.

Balance sheet construct is being calibrated towards higher margin segments and granular deposits which could slightly affect loan growth, stated PL, however, this should bode well over the medium term from a profitability perspective. CITI integration costs and business investments would also keep opex elevated, it added. For FY24/25E, the brokerage raised NIM and opex while reducing provisions resulting in ~3 percent PAT upgrade. With a likely RoA of 1.7 percent for FY25E, the valuation discount to ICICIB (27 percent) should also narrow, said PL.

Motilal Oswal: The brokerage has retained its ‘buy’ call on the stock with a target price of ₹1,150, implying an upside of 18 percent. Axis reported a PAT of ₹5,797 crore largely driven by robust ‘other income’. NII growth was healthy while margins moderated 12bp QoQ to 4.1 percent, it said.

"Axis delivered a stable performance in 1QFY24, with earnings driven by higher ‘other income’ even as margins compressed on expected lines. Business growth was healthy, led by traction across segments. Asset quality remains broadly stable with an increase in fresh slippages. The restructured book was well managed and coupled with a higher provisioning buffer, it provides comfort on credit costs," noted MOSL. The brokerage has made slight adjustments to its estimates and expects Axis to deliver RoA/RoE of 1.9 percent/17.7 percent in FY25.

InCred Capital: The brokerage has a ‘hold’ call on the stock with a target price of ₹1,030, indicating an upside of just 5.5 percent. It said that it prefers to remain skeptical of the bank’s growth, margin and asset quality trajectory in the near term.

"Axis Bank reported growth in advances by 22.4 percent yoy/1.6 percent QoQ in 1QFY24, which is weak compared to most peers. The bank’s struggle to manage quality growth at a price has been a challenge for the past several quarters. Retail assets of the bank grew by 2 percent QoQ, which was mainly driven by credit cards and small business financing whereas the mortgage portfolio continues to decline sequentially. Deposits during the quarter grew by 17.2 percent yoy but declined by 0.6 percent sequentially. Axis Bank has reported a sequential decline in its margins by 12 bps amid a sharp surge in the cost of funds. The stretched CD ratio (91.2 percent) requires faster deposit augmentation. This, coupled with a gradual repricing of the deposit base, will exert pressure on its margins. Accordingly, we are building in 30 bps compression in margins for FY24E," it said.

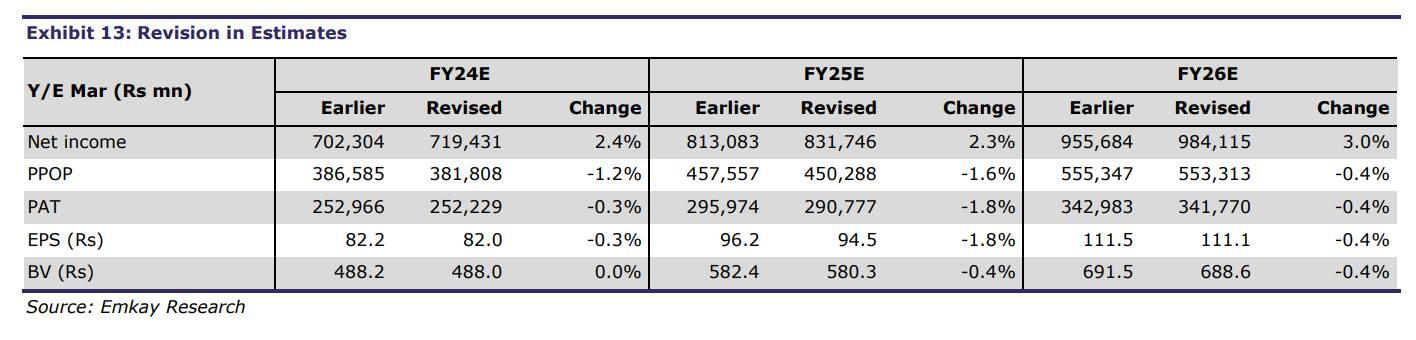

Emkay: The brokerage has maintained its ‘buy’ call on Axis Bank with a target price of ₹1,260, indicating a potential upside of 29 percent.

"Despite lower margins yet again and rigidly higher opex, Axis Bank is back in the black, given in-line PAT mainly on higher treasury gains. Similar to 4Q, Bank logged better than expected credit growth, at 18 percent YoY but the margin slipped again with a cumulative contraction of 16 bps to 4.1 percent in the past 2Qs. Fresh slippages were higher but the GNPA ratio improved QoQ to 1.9 percent. We expect Axis Bank to clock 1.8 percent RoA and 18 percent RoE on a merged basis over FY24-26E," said the brokerage.

Source: Emkay

First Published: 27 Jul 2023, 01:56 PM IST