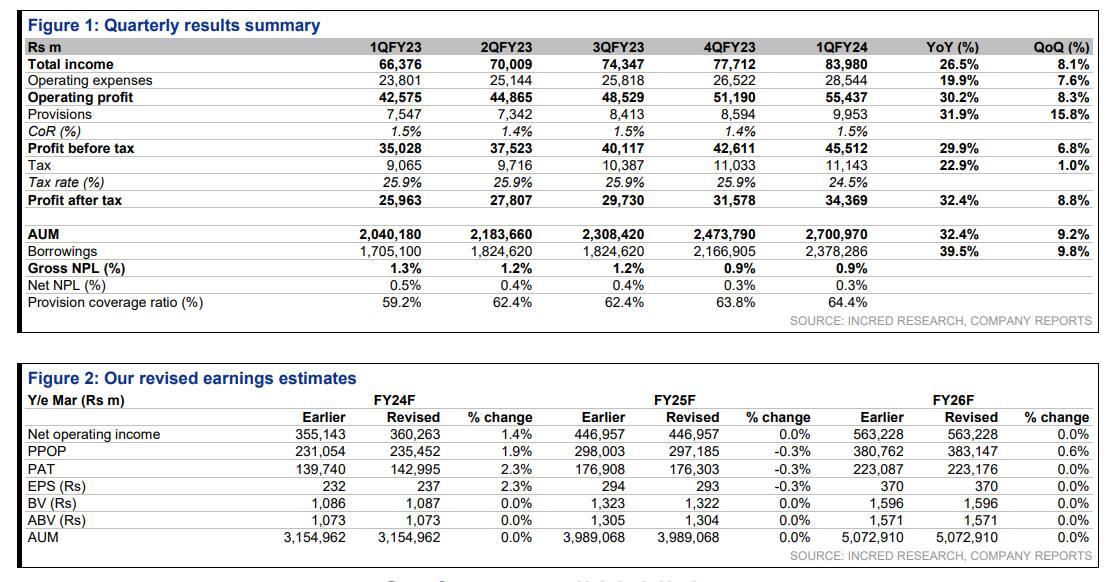

NBFC major Bajaj Finance posted better-than-expected June quarter results (Q1FY24) on most fronts. Its profit jumped 32.4 percent YoY at ₹3,437 crore compared to ₹2,596 crore in the same quarter last year. This was driven by strong growth in the company's assets under management (AUM).

Bajaj Finance Q1 earnings review: Brokerages bullish on the stock; see up to 30% upside

TL;DR.

After the earnings, most brokerages reiterated their bullish view on the firm due to strong business updates, robust loan growth, and healthy new customer acquisition.

The NBFC delivered its highest-ever AUM growth of ₹22,718 crore in the June quarter, with 99.4 lakh new loans and 38.4 lakh new customers.

Its net interest income (NII) for the quarter also rose 26 percent YoY to ₹8,398 crore versus ₹6,640 crore in the corresponding quarter last year.

After the earnings, most brokerages reiterated their bullish view on the firm due to strong business updates, robust loan growth, and healthy new customer acquisition. Some even upgraded the recommendations and target prices for the stock. The target prices for Bajaj Finance are in the range of ₹8,550-9,650 range, implying up to 30 percent upside.

Brokerage views

CLSA: The brokerage upgraded the stock to ‘buy’ from outperform and raised its target price to ₹9,000 from ₹6,000 earlier, indicating an upside of 21 percent. As per the brokerage, Bajaj Finance’s loan growth beat estimates and its valuation offered further upside.

“Bajaj Finance reported very strong pre-quarterly numbers for 1QFY24. While we expected 6-7 percent QoQ AUM growth, the company delivered 9 percent QoQ growth, taking the YoY tally to 32 percent. This is extraordinary for an NBFC of its size," it said. Moreover, new customer acquisition was healthy and volume growth in disbursements was a strong 34 percent YoY, it added. This gives the brokerage comfort that loan growth was not just ticket-size led.

JM Financial: The brokerage has a ‘buy’ call on the NBFC with a target price of ₹9,500, indicating an upside of almost 28 percent.

Bajaj Finance (BAF) continued its strong all-round performance with RoA at 5.4 percent (6th consecutive qtr of over 5 percent RoA), said the brokerage. BAF has persistently delivered strong profitability metrics in a competitive space, it has started looking forward by identifying the next leg of growth. After building up its digital capabilities, JM believes it remains well-placed to drive growth and industry-leading profitability metrics. Asp er the brokerage, BAF remains well positioned given its long-standing track record in unsecured loans, strong cross-sell customer franchise, superior risk model and diversified product portfolio. BAF has raised its long-term RoA (return on assets) guidance to 4.6-4.8 percent (from 4-4.5 percent earlier) and RoE (return on equity) guidance to 21-23 percent (from 19-21 percent earlier), it noted.

JM estimates assets under management (AUM) CAGR of 29 percent over FY23-25E with RoA/RoE of 4.8 percent/25 percent, respectively, in FY25E. In this light, current valuations at P/BV of 5.4x on FY25E BVPS and P/E of 23.5x FY25E EPS, it believes are reasonable for a quality franchise as BAF.

Motilal Oswal: The brokerage has a ‘buy’ call on the stock with a target price of ₹8,800, implying an 18 percent upside.

Bajaj Finance (BAF)’s Q1FY24 reported PAT was in line with estimates. The good operational performance was driven by: a) healthy run-rate in customer additions/new loans disbursed, b) further asset quality improvement, and c) YoY moderation in cost-income ratios during the quarter, said MOSL. NIM was stable QoQ at 13 percent in Q1FY24 even as reported NII declined 10 bps QoQ, added the brokerage. It expects a NIM compression of 25 bps in FY24E due to the expected rise in the cost of borrowings and difficulty in passing on interest rate hikes to customers. It estimates an AUM/PAT CAGR of 29 percent/26 percent over FY23-FY25 and expects BAF to deliver an RoA/RoE of 4.6 percent/25 percent in FY25.

Customer acquisitions and the new loan trajectory have been strong. The momentum will only get stronger ahead, with the digital ecosystem – app, web platform, and full-stack payment offerings – in place, it stated. BAF should be able to offset the NIM compression in FY24 with lower operating cost ratios and credit costs. However, MOSL cut its FY25E EPS by 2 percent to factor in higher credit costs.

YES Securities: The brokerage retained its ‘buy’ call on the stock but raised its target price to ₹8,550, indicating an upside of 15 percent.

"Bajaj Finance has exhibited resilience in growth and profitability through various phases of competition, economic cycles/events and liquidity, underpinned by a dominant market position in focused segments, agile business approach and addition of new growth segments. Development of new product lines like Gold Loans, Auto loans, CV finance, Tractor loans, Microfinance and Emerging Corporate loans would support long-term franchise growth. Retain BUY with increased 12m target of ₹8,550," it said.

Meanwhile, it also noted that the raising of AUM growth assumptions and a marginal downward adjustment in tax rate by Bajaj Finance caused a 4 percent upgrade in its FY25 profit estimate. The stock is trading at a shade above its long-term mean valuation and there is headroom for re-rating with the persistence of robust growth and RoE delivery, added the brokerage.

Anand Rathi: The brokerage has a ‘buy’ call on the stock with a target price of ₹9,650, indicating an upside of 30 percent.

"Driven by strong, 32 percent YoY, AUM growth, Bajaj Finance’s Q1 FY24 net profit rose 32.4 percent (above expectations). With many levers (loan growth, high NIMs and steady asset quality), we reiterate our Buy. Despite premium valuations, we retain a Buy," it said.

The focus for the coming year will be deepening penetration in payments. BAF launched car finance in the quarter. A widening product base, strong online presence and deepening penetration in rural markets are likely to aid the expansion of loans at a 28.5 percent CAGR over FY23-FY25, further stated the brokerage. Calculated NIM on AUM (14.2 percent) during the quarter held up despite the increase in interest rates. The brokerage factors in a 30 bps moderation in NIM from these levels. At 34 percent, cost income has improved by 160 bps YoY. It builds in a cost-assets of 3.9 percent over FY24-25 as the omnipresence strategy scales up.

InCred Capital: The brokerage retained its ‘add’ call on the stock with a target price of ₹9000, implying a potential upside of 21 percent.

Bajaj Finance posted consolidated Q1FY24 AUM growth of 32.4 percent YoY, with consistency in AUM break-up. BAF is heading towards a granular AUM growth mix against seasonal momentum, led by diversified assets. NII growth was relatively weaker as the company has been facing margin headwinds, but steady operating leverage further aided profitability, it said. The brokerage believes that improving operating leverage along with low credit cost is key to profitability. It has built-in a 25 percent CAGR in PAT over FY23-26F with best-in-class RoA of 4.5 percent and RoE of 24.5 percent. BAF is a pure-play retail-lending franchise equipped with a diversified funding mix and a strong capital base. The stock is currently available at ~5.8x BV/24x EPS for FY25F (PEG ratio >1), offering an attractive risk-reward ratio, it added.

Source: Incred

First Published: 27 Jul 2023, 02:53 PM IST

Related Stories

Explain Like I am 5

markets

What are the investing mistakes retail investors make and how to avoid them?

Manik Kumar Malakar