Bajaj Finance, a leading Indian non-banking financial company (NBFC), has seen a drop of 9.33% in the value of its shares in 2023 so far. The stock started to plummet after hitting a 52-week high of ₹7,778 apiece in September last year, and it has since tumbled by over 23.36% to ₹5,961.

Bajaj Finance shares plunged 23% since September; Investec sees further decline – key challenges

TL;DR.

BAF's primary strength has been the unsecured segment, but there has been an increase in competitive intensity. Multiple private sector banks and PSU banks are increasing their focus on the personal loan segment, and several NBFCs have announced plans to scale unsecured loans.

But according to recent projections made by the brokerage house Investec, the stock will continue its downward trend going forward. It sees the stock falling another 19.47% from the current market price to ₹4,800 apiece, maintaining a 'sell' call on the stock.

The brokerage has expressed concerns about Bajaj Finance's (BAF) performance in the current decade despite its impeccable execution over the past decade (2010–2020) in terms of growth, asset quality, and profitability.

Investec has highlighted several challenges, including BAF's size, which is a constraint with around 15% market share in active customers in India. It says that the competition is increasing in unsecured credit and the barriers to entry in this sector are shrinking, leaving Bajaj Finance losing its competitive edge over the unsecured loan segment.

Investec believes that BAF's supernormal profits in the unsecured sector may not be sustainable, and incremental capital allocation is happening in a lower return on equity (RoE) segments, it said.

Additionally, the brokerage has also identified technical factors such as the listing of its subsidiary Bajaj Housing and the possibility of a regulatory push to transition to a bank that could spur a de-rating.

Despite a 90% premium over large private banks, Investec believes that BAF's valuation does not accurately reflect these risks.

Let's look at each of the challenges listed by the brokerage in detail.

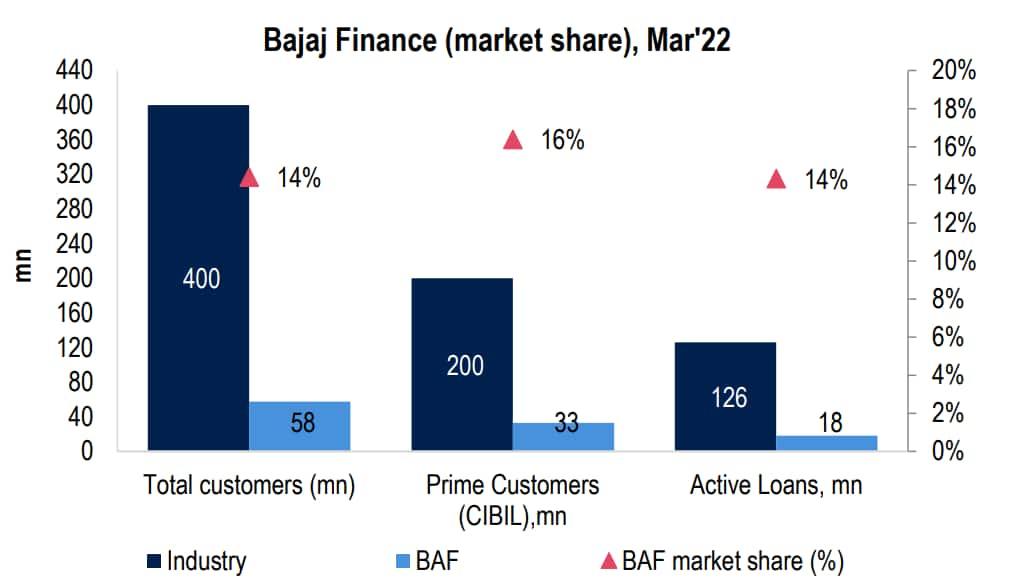

Size to become a constraint

“We estimate BAF is serving 15% of customers in India, which is evident from multiple data points including BAF’s customer franchise, BAF’s cross-sale franchise and BAF’s active loans.”

“We view 15% market share as an upper cap in a competitive market like lending. This cap is visible in multiple segments: housing loans, gold loans, microfinance, and auto loans. In only two segments, players have crossed 15% market share: Bajaj Finance in consumer durables; HDFC Bank in credit cards; and SBI in unsecured personal loans,” said Investec.

Bajaj Finance is serving 15 percent of India’s customers.

Bajaj Finance has a high market share in high yielding segments like consumer loans, personal loans, and 2-wheeler loans. In low-yielding products like house loans and LAP, its market share is modest, it noted.

Competition picking up in unsecured credit

BAF’s key strength has been the unsecured segment but here the competitive intensity has been increasing. Multiple private sector banks and PSU banks are increasing their focus on the personal loan segment, and several NBFCs have announced plans to scale unsecured loans, according to Investec.

Investec believes that all banks are now in a strong position, with a robust capital position and improved asset quality, which enhances their willingness to compete in the unsecured segment.

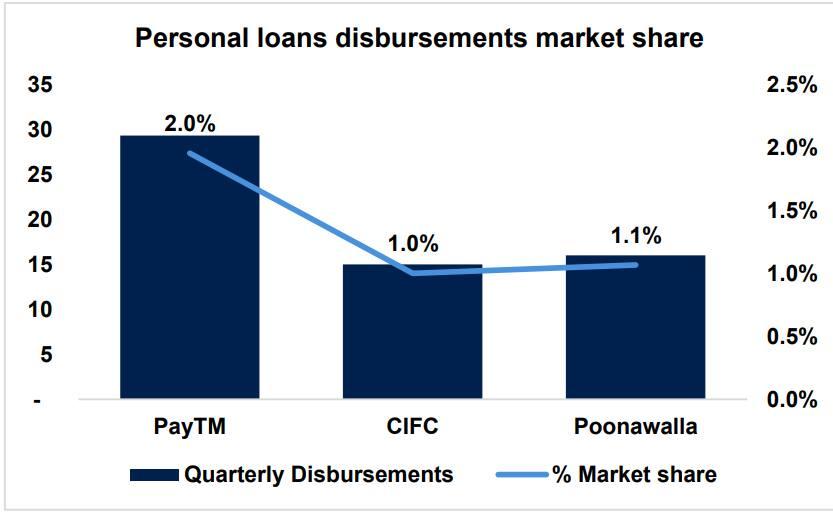

The brokerage notes that new entrants have scaled unsecured loans to 1%–2% incremental market share in a short period of time, indicating that barriers to entry in unsecured segments may have reduced due to the advent of digital lending and data availability.

New entrants have scaled to 1%+ market share in a short span of time.

The underwriting process has been simplified, and customers' creditworthiness can be accessed via credit scores, Aadhar-linked accounts, and digital account statements.

The unsecured segment is witnessing competition from various players, including almost all banks, including PSU banks and small banks. Additionally, multiple NBFCs are planning to scale their unsecured loan offerings, including Chola Finance, Poonawalla Fincorp, Aditya Birla Capital, Piramal Capital, and Mahindra Finance, among others.

Banks operate in higher ticket and low-yield segments, while NBFCs operate in relatively small ticket size and high-yielding segments. The verdict is still out on how these new entrants will manage collections, the brokerage said.

Era of super normal profits coming to an end?

The brokerage has estimated that BAF's yield in the PL/SME segments at approximately 18.5%, considering lending to prime customers with a CIBIL score of 750 or higher. This has kept credit costs low in the past, but the brokerage believes that it is not sustainable and expects competition to disrupt the company's profits and growth.

As a result, Investec predicts that BAF's growth and profitability will moderate, with an estimated AUM and PAT CAGR of 23% and 20%, respectively, from FY23E-FY26E. These estimates for FY25E AUM and PAT are approximately 3% and 5% lower than consensus estimates.

Potential listing of Bajaj Housing Finance

Bajaj Housing Finance has been categorized as an NBFC-upper layer entity as of September 30, 2022, and is required to be listed within three years of this identification, i.e., by September 2025, said Investec.

Bajaj Housing is registered as non-deposit taking HFC. Its return ratios are low, including an RoA of 1.7% and a RoE of 11% for FY22. As it operates in a competitive housing finance segment, its RoEs are likely to remain below 15%.

The company's loan mix is already optimized, with housing loans accounting for 62% of its assets as of December 22. A housing finance company should have 60% of its assets comprising housing loans and at least 50% comprising individual housing loans.

Considering these fundamental factors of the housing finance business, Investec expects that the street will assign a 2x to 3x one-year forward multiple for Bajaj Housing. This will be sharply lower than the consolidated P/B multiple of Bajaj Finance at 5.4x FY24E P/B.

Return ratios to reduce, leading to lower incremental RoE

BAF is expected to report RoA and RoE of 4.9% and 23.5% in FY23, which is its all-time high RoA and RoE.

The brokerage holds the view that these are not sustainable for Bajaj Finance, and the RoA and RoE will decrease in the FY2024 as margins decline, the recovery of written-off accounts normalizes, and credit costs return to normal levels, it added.

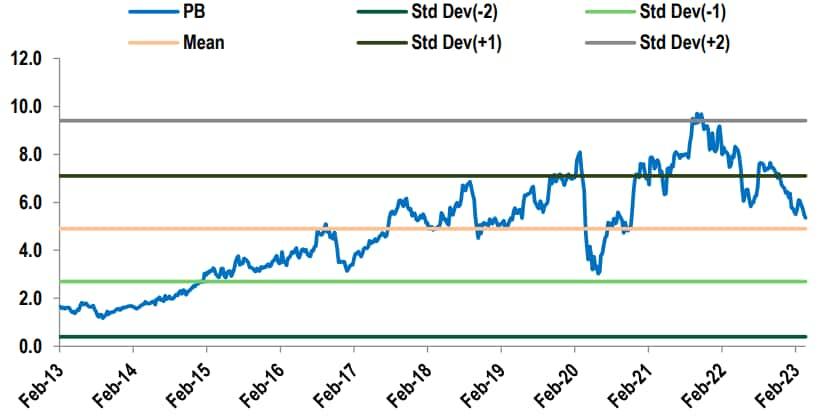

BAF trades near its historical mean valuations

BAF de-rated in the last 12 months and now trades at near its historical mean valuations. In comparison to other well-run private sector banks like HDFC Bank and Kotak Mahindra Bank, BAF's valuation is currently at a premium of around 90%. This premium is in line with BAF's average premium over HDFC Bank and Kotak Bank since April 2016.

Bajaj Finance trades near its historical mean valuations.

“We believe BAF’s valuation premium over HDFC Bank and Kotak will shrink as we expect its growth differential over these banks to narrow down,” the brokerage stated.

30 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

A scheme with a higher standard deviation usually has greater volatility.

First Published: 18 Apr 2023, 08:24 AM IST

Topics to follow

Related Stories

markets

Tata Technologies IPO: Here's how the public issue will impact Tata Motors

Dhanya Nagasundaram