Following the Q1FY24 performance of Bank of Baroda, a leading PSU bank, domestic brokerage firms kept their positive outlook on the stock.

On August 5, the bank reported an 88% jump in its net profit to ₹4,070 crore, driven by a significant surge in other income. The bank's other income came in at ₹3,322 crore as compared to ₹1,182 crore reported in the same period of last year, a surge of 181%.

Net interest income (NII), which is the difference between the interest earned from lending activities and the interest paid to depositors, came in at ₹10,997 crore, an increase of 24% YoY. The bank's net interest margin improved to 3.27% in Q1FY24 from 3.02% in Q1FY23.

The pre-provision operating profit (PPOP) stood at ₹7,824 crore for the June 2023 quarter, showing a growth of 72.8% YoY. The bank's provisions rose by 15.5% to ₹1,946 crore from ₹1,685 crore in Q1 FY23.

Its gross non-performing assets (NPA) came down by 275 basis points to 3.51% from 6.26% in Q1FY23. Similarly, net NPA dropped by 111 basis points to 0.78% from 1.58% in the year-ago quarter.

The total advances of the bank grew by a robust 18% YoY to ₹9,90,988 crore. As against this, domestic advances grew at a lower 16.8% to ₹8,12,626 crore, taking the total business to ₹21,90,896 crore, which was 17% more than the year-ago period.

As for deposits, there was a 15.5% YoY growth in domestic deposits to ₹10,50,306 crore, while international deposits grew by 21% YoY to ₹1,49,602 crore, taking global deposits to ₹11,99,908 crore, an increase of 16.2% YoY.

"BOB reported a mixed quarter with healthy treasury gains offsetting the pressure on NII, thus enabling the bank to deliver an annualised RoA/RoE of 1.1%/20.0%."

"Higher other income and lower opex thus drove earnings, while margins witnessed a decline to 3.27%. Business growth was healthy at 21% YoY, aided by strong traction across segments while the CASA mix moderated. Asset quality continues to improve, with the NNPA at 0.78%. A lower SMA book and controlled restructuring provided further comfort on asset quality," said domestic brokerage firm Motilal Oswal.

Motilal Oswal retained its earnings estimates, projecting FY25E RoA/RoE at 1.2%/16.9%. The brokerage valued the stock at ₹240 (based on 1.1x FY25E ABV) and reiterated their 'buy' rating on the stock.

Similarly, global brokerage firm JM Financial also kept its 'buy' call on the stock after Q1 performance. The brokerage has a target price of ₹235 apiece.

JM Financial anticipates an average RoA/RoE of 1.01%/16% by FY25E, driven by higher credit growth, portfolio rebalancing, and sustained asset quality.

Prabhudas Lilladher also reiterates its ‘buy’ recommendation, with an unchanged target price of ₹235 per share.

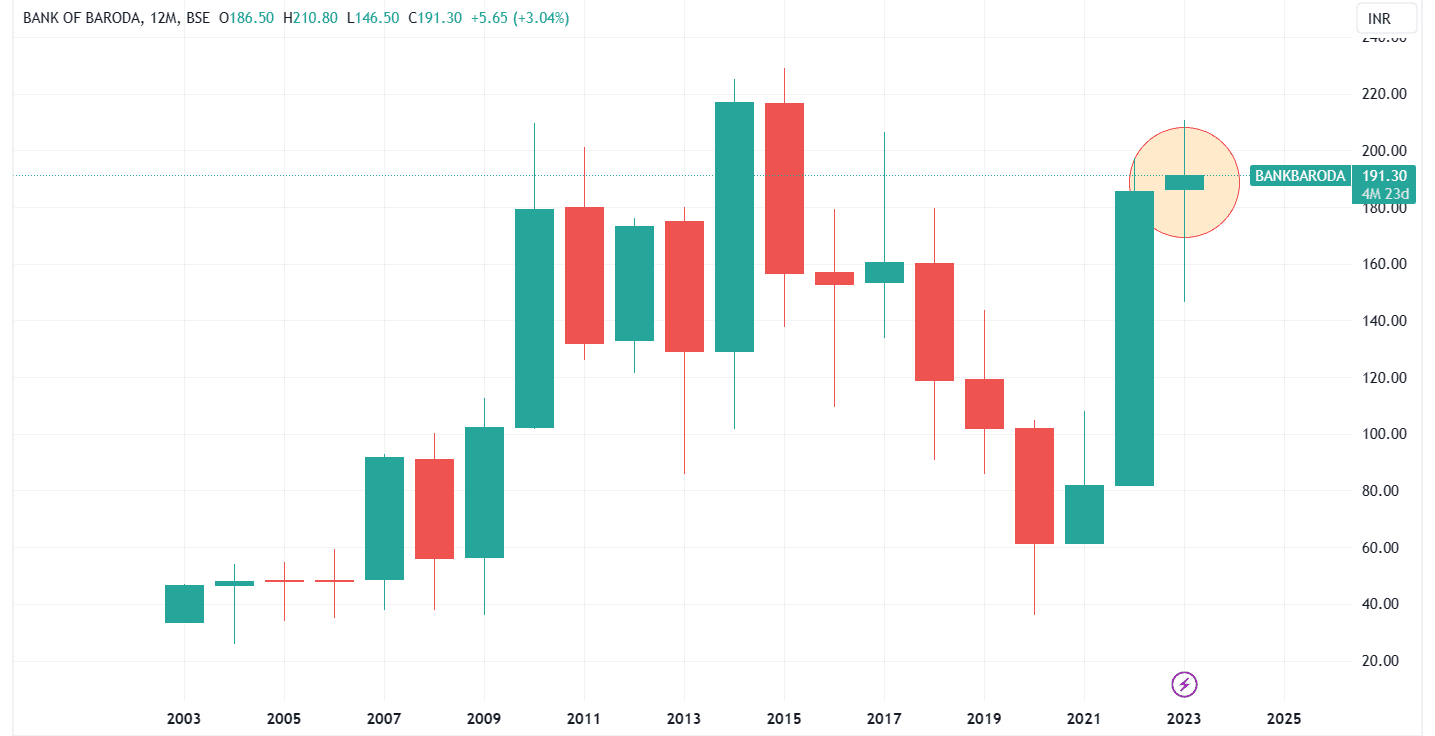

Meanwhile, the shares of the state-owned bank have gained modestly by 3.37% in the current year so far. In CY22, the stock delivered a multi-bagger return of 126.54%, and in the year before that, it gained 33.35%.

30 analysts polled by MintGenie on average have a 'strong buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie