BP Wealth Techno Funda recommendations from BP Equities Pvt Ltd are developed using a combination of technical and fundamental analysis, and the calls are primarily intended for institutional/ high networth individuals (HNI) investors. The recommendations are for making one-month positional trades and are based on selecting fundamentally sound stocks at the right time.

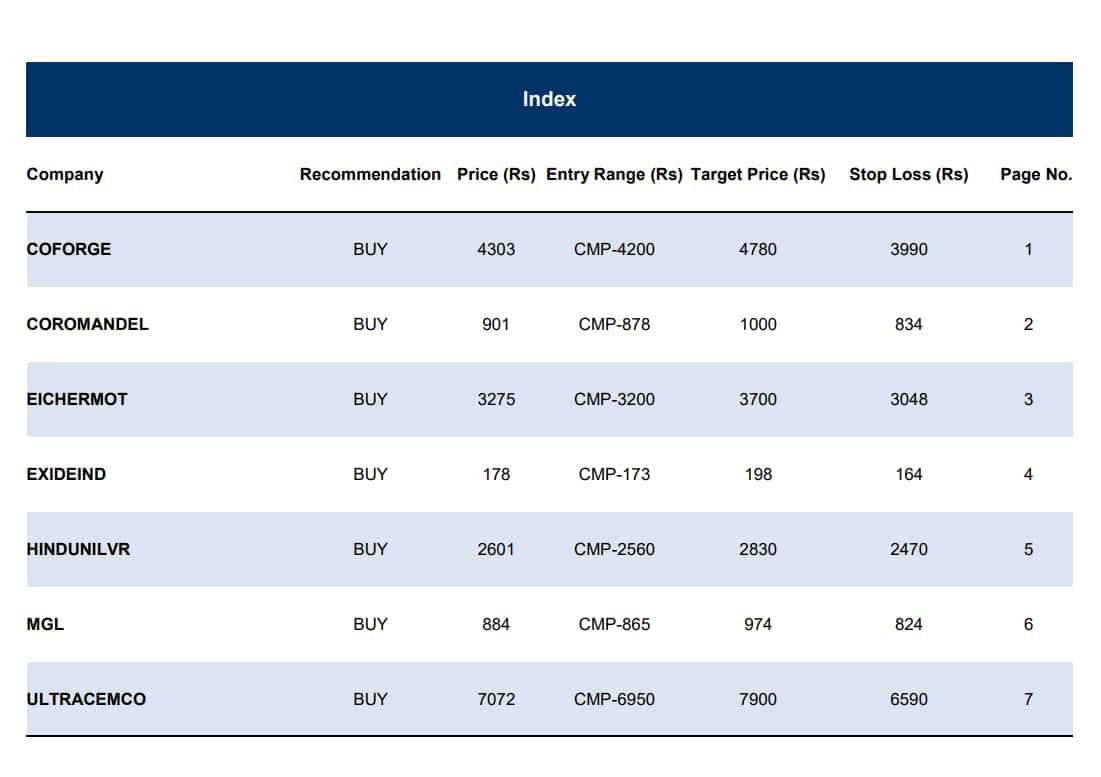

Let's take a look at its super seven picks for the month of February:

The Techno Funda technical recommendations from BP Wealth suggest that Coforge Ltd has a great relative performance compared to both its sectoral index and benchmark index. This supports the stock's further strength.

The price movement underwent a consolidation period known as stage one after correcting 48% from the all-time high (ATH) levels.

The price action witnessed a decent accumulation and attracted experienced investors.

On the fundamental front, the brokerage follows the cues offered during the third quarter of FY23, when the company signed the biggest deals in its history. Further on the back of the business' growing momentum which is probably going to continue into FY24, the brokerage is bullish on the stock.

"During Q3FY23, the operating profit grew both sequentially and annually. The key reason attributed to the improvement is the increase in the offshore revenue contribution and improvement in utilization. Also, continuous increases in the billing of graduate engineer trainees hired directly from college played a significant role in enhancing the profitability of the company," said the brokerage in its report.

There were five sizable deals in the $345 million new order book for Q3FY23. The company stated that one of the growth drivers for its strong growth, which is anticipated to continue in the upcoming quarters, is the vendor consolidation theme.

It has recommended a 'buy' rating to the stock at the current market price (CMP) of ₹4,200 for the target of ₹4,780 with a stop loss of ₹3,990 in the short term.

The brokerage is bullish on the fertilizer company's stock on the backdrop of robust Q3FY23 results as the company registered good growth in revenue and profitability.

"Record volume sales in nitrogen, phosphorus, and potassium (NPKs) and higher subsidy realisation in the nutrients business led to an increase in revenues during the quarter. In the crop protection business, domestic formulation and B2B business grew during the quarter which was partially offset by headwinds in the export market," said the brokerage in its report.

The capital expenditure (capex) budget for FY23 has been maintained by Coromandel International at ₹800-900 crores. All of the initiatives are progressing successfully and on schedule.

On the technical front, the brokerage believes that the relative strength (RS) line compared to the Nifty 50 is rising, and finding support at an upward sloping trendline, which indicates underlying strength in the price.

It has recommended a 'buy' rating to the stock with a target of ₹1,000 and a stop loss of ₹834 in the short term.

Brokerage BP Wealth claims that Eicher Motors Ltd will benefit from its upcoming launches in terms of performance. As per the report, its recently introduced Hunter 350 (J series engine platform) product received strong customer response, led by young and first-time buyers whose share increased from 13% to 18% post Hunter 350 launch. The cost of the Hunter 350 product was reasonable at ₹150,000.

Further, with a solid product selection, Royal Enfield has experienced a 4x increase in sales in foreign countries over the last three years.

"In most of the markets where it has a presence, the company is inching towards securing a 10% market share in the mid-segment motorcycle market (250cc - 650cc), which offers a large addressable market for the company. On the international front, demand remained strong in North America and Latin America (LATAM), while inflationary challenges have impacted demand in the European Union (EU)," said the brokerage.

On the technical front, the brokerage said that the stock recently reversed, taking support near its former resistance zone, putting polarity into play and signalling a strong price action.

It has recommended a 'buy' rating to the stock at the current market price (CMP) of ₹3,200 for the target of ₹3,700 with a stop loss of ₹3,048 in the short term.

The brokerage claims that Exide Industries Ltd's robust demand outlook provides comfort for long-term growth.

The brokerage report indicated that as the replacement market grows and original equipment manufacturer (OEM) demand increases with the easing of semiconductor supply limitations, the company's demand prospects on the automotive side continue to improve.

A good order inflow was experienced in the industrial division as a result of the general uptick in economic activity and increased spending by both the public and private sectors.

"Due to the positive outlook, the company has been setting up a lithium-ion cell manufacturing plant to cater to the electric vehicle (EV) industry. The recent budget announcement will help the company to compete with global players," said the brokerage in its report.

In terms of technical analysis, the stock is presently trading at the polarity support, which corresponds with the short-term (20) and medium-term (89) weekly exponential moving averages, indicating a large demand zone for the price.

It has recommended a 'buy' rating to the stock at the current market price (CMP) ₹173 for the target of ₹198 with a stop loss of ₹164 in the short term.

The brokerage claims that HUL's strong performance in the main operating segments and the expansion of its market share will pave the way for its future expansion.

HUL kept up its growing pace by turning in a successful third quarter of FY23. Due to pricing hikes and efficient market development strategies, the company's homecare and fabric wash sectors experienced double-digit growth. Skin care did well in the beauty and personal care sector because palm oil prices have decreased. Additionally, the foods & refreshment section saw consistent growth driven by food, coffee, and ice cream, while the non-winter portfolio experienced double-digit growth.

On the other side, the company’s recent strategic investments in OZiva and Wellbeing Nutrition aim to increase its market share in this category in the long run.

On the technical front, the brokerage said that the volatility over the last 20 weeks trades at lower end and hence any unruly move is less likely. The stock also has improving relative strength against the benchmark index.

It has recommended a 'buy' rating to the stock at the current market price (CMP) of ₹2,560 for the target of ₹2,830 with a stop loss of ₹2,470 in the short term.

The brokerage believes that India has a lower per capita energy consumption than the rest of the globe, which suggests that the country's oil and gas and energy sectors have tremendous room to grow. By 2030, the government wants to boost natural gas's share in the primary energy mix from the current 6% to 15%. As a result, Mahanagar Gas has a sizable window of opportunity to capitalise on this expanding market and take action by expanding its activities outside of Mumbai and Maharashtra.

On the technical front, according to the brokerage, the stock had registered breakout from double bottom price pattern which is considered as bullish reversal pattern in nature and hence highlights reversal in trend from bearish to bullish.

"Relative Strength Indicator is trading at 52 week high reading and has entered into bullish territory after more than 2 year indicates inherent strength in price and relative strength against benchmark index," said the brokerage.

It has recommended a 'buy' rating to the stock at the current market price (CMP) of ₹865 for the target of ₹974 with a stop loss of ₹824 in the short term.

Infrastructure development continues to be a crucial factor in advancing India's position on the world stage. Accordingly, the Union Budget 2023–24 proposed an increase in capital spending for infrastructure development of 33% to Rs. 10 lakh crores. This presents a significant opportunity for established businesses like UltraTech Cement to grow, believes the brokerage.

Further, on the back of robust Q3FY23 earnings of the company, the brokerage expects the situation to improve going forward.

According to the report, in Q3FY23, the company reported a revenue growth of about 20% on year, led by significant volume growth of its domestic grey cement business. Additionally, there was a notable improvement in its capacity utilisation to 83% as against 75% in Q2FY23, and moving forward, the management expects it to increase further.

On the technical front, as per the brokerage, in November 2022, the stock registered a breakout from inverse head & shoulder pattern which is bullish reversal signal and highlights bullish bias in price for medium term trend. Post breakout, price has been consolidating in the tight range around the neckline of pattern with positive bias.