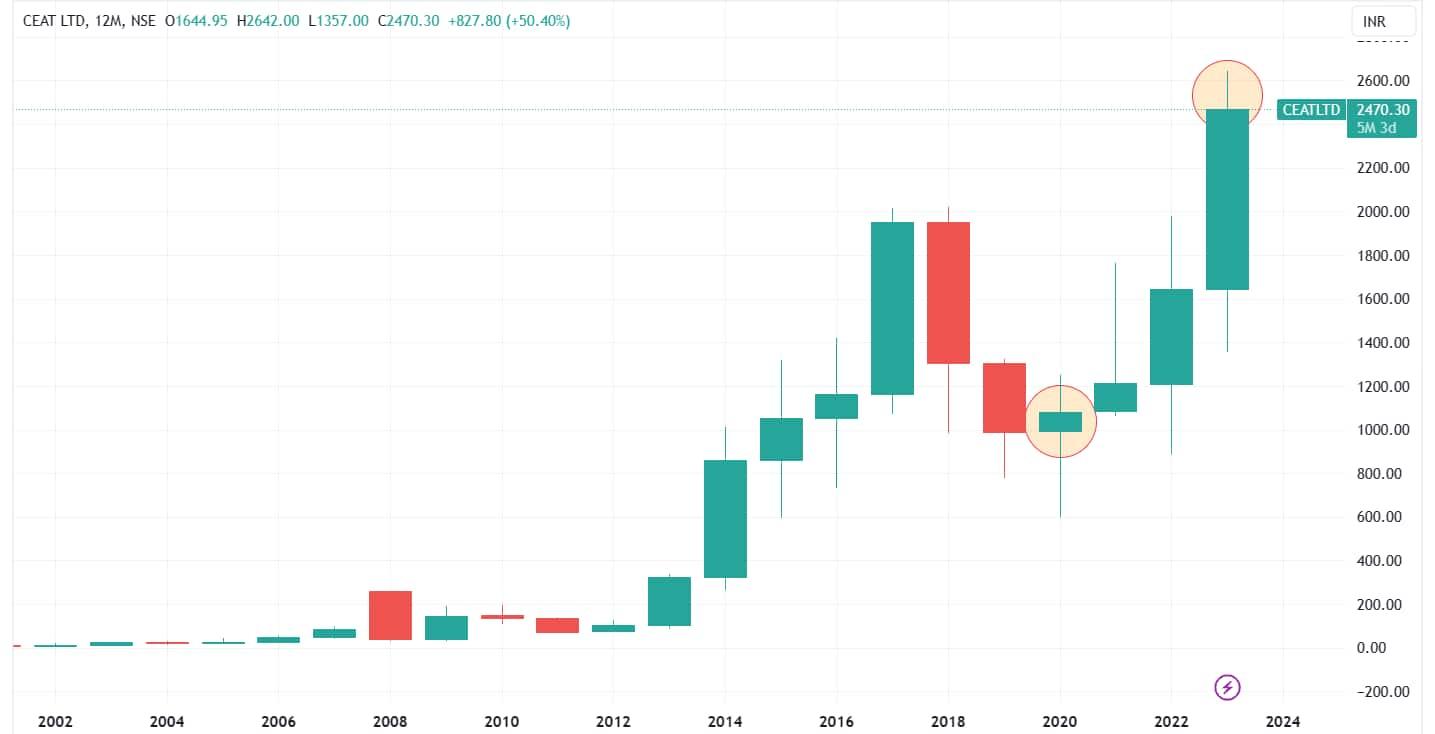

In a remarkable display of consistent growth, CEAT shares have continued their positive trajectory for the fourth consecutive year, rewarding investors with handsome returns. In the current year so far, the stock has zoomed by 52%.

Looking back over the last three years, CEAT shares have consistently delivered strong returns to shareholders. In CY22, the stock recorded a return of 35.16%, and the preceding year, it witnessed a decent rally of 12.5%. Even in CY20, amidst challenging market conditions, the shares gained a commendable 9.31%.

Over the last ten years, the stock has displayed exceptional resilience, closing only two years with marginal declines. During CY13, the stock skyrocketed by 207%, and the following year, CY14, it rewarded investors with a multi-bagger return of 167%.

Zooming out to encompass the entire decade, CEAT shares have yielded an astonishing 1865% return, exhibiting a substantial climb from ₹127 apiece to the current trading level of ₹2,495.

Founded in 1958, CEAT is one of India’s leading tyre brands and the flagship company of the RPG Group. CEAT offers the widest range of tyres to all segments and manufactures world-class radials for heavy-duty trucks and buses, light commercial vehicles, earthmovers, forklifts, tractors, trailers, cars, motorcycles, and scooters, as well as auto-rickshaws, as per the company website.

For the June-ending quarter, CEAT reported another strong performance, with its net profit reaching ₹144 crore. This marks a significant turnaround compared to the net profit of ₹8.69 crore reported in the same quarter of the previous year.

It witnessed a 4.1% YoY growth in operating revenue to ₹2,935 crore in Q1FY24. Although the revenue growth showed a marginal increase, CEAT managed to improve its margins, primarily due to softened raw material costs.

During the quarter, the company's raw material expenses dropped to ₹1,729.6 crore, representing a 10.2% drop compared to the ₹1,925 crore recorded in the corresponding period last year. This helped the company to expand its gross margin by 938 basis points YoY to 41.1% and by 97 basis points QoQ.

While employee costs declined due to higher retirals and incentives (down 80 basis points QoQ as a percentage of sales), they were offset by higher other expenses (up 150 basis points YoY and 140 basis points QoQ as a percentage of sales). The increase in other expenses was primarily attributed to higher ad spend (up 40 basis points QoQ) and other costs. Consequently, the EBITDA margin expanded by 703 basis points.

The operating profit increased to ₹384 crore, a surge of 124.5% YoY and 2.5% QoQ. The company's debt declined by ₹100 crore QoQ to reach ₹2000 crore, mainly due to healthy cash generation in 1QFY24.

Following the company's Q1 performance, domestic brokerage firm Motilal Oswal raised its FY24 and FY25 EPS estimates by 11% and 9%, respectively, factoring in lower volume and realisation growth in key categories, better gross margins, higher interest costs, and a lower tax rate.

In light of CEAT's focus on capital allocation and the resulting increase in capital efficiency, Motilal Oswal raised its target multiple for the company to 15x from 13x., maintained a 'buy' rating with a target price of ₹3,000 per share (based on 15x Sep’25E EPS).

19 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.