In the December quarter of FY23 (Q3FY23), the slowdown in staples moderated while it intensified in discretionary, an earnings review report by global brokerage house Nomura stated. For the first time in many (normal) quarters, the brokerage said that it noticed a stark difference in the trends within staples and discretionary.

The revenue and EBITDA for staples in the quarter under review rose 12 percent and 9 percent YoY, respectively. Meanwhile, the sales growth in the discretionary stocks came in at 10 percent and the EBITDA declined 13 percent on a YoY basis.

As per the report, while staples' revenue growth was in line with its historical average, discretionary revenue growth was materially lower.

Weakness in demand was seen across subcategories such as quick service restaurants (QSR), footwear and paints, while a sharp sales decline in the apparel/inners category was most surprising in a seasonally strong quarter (festive/wedding season), it noted.

The brokerage further illustrated that overall in the December quarter, staples volumes remained at low to mid-single-digit growth due to linear price increases and tepid rural demand. However, it added that demand was better in the September quarter.

In contrast, the brokerage mentioned that discretionary volumes reported flat-to-high single-digit volume decline across sub-categories (paints, jewelry, QSR, apparel and footwear) due to a shorter festive season, pent-up base/high-channel inventory and sharp price hikes taken earlier impacting demand.

Nomura also pointed out that Q3FY23 was the first quarter (after many quarters) of no material price increases. Staples GPM/OPM expanded QoQ (+190bp/+100bp) on moderation in input costs, while discretionary GPM/OPM contracted QoQ (-100bp/-10bp) on negative operating leverage.

Nomura also has listed the top hits and misses for the December quarter. Let's take a look:

Q3FY23 hits

Britannia: Volume growth continued (low single-digit YoY) despite another round of strong price increases (mid-teens YoY).

HUL: Outperformance to market continued with over 5 percent YoY volume growth (vs -4 percent YoY industry volume for its categories).

Godrej consumer: Volumes reported growth (+3 percent YoY), after a few quarters of decline, despite a challenging business environment; strong sequential improvement in GPM (+330bp QoQ) and OPM (+420bp QoQ) on the back of lower input costs.

ITC: Strong recovery in cigarettes (+15 percent YoY volume growth); three-year CAGR improved to 6 percent in Q3 vs 4 percent in Q2. FMCG revenue, up 18 percent YoY, was also better than peers.

Tata Consumer: Despite strong price increases (+23 percent YoY) in the salt business, volumes grew 4 percent YoY.

Q3FY23 misses

Colgate: Lacklustre growth in core brands (overall volume growth of -2.5 percent YoY).

Dabur: Sluggish volume growth (-3 percent YoY) driven by delayed onset of winter and downtrading in rural markets.

Marico: Value growth in Parachute coconut hair oil/ value-added hair oil continued to remain sluggish (-6 percent/-3 percent YoY).

Tata Consumer: Tea business volumes declined 5 percent YoY as demand in north India was impacted. It also witnessed increased competitive intensity from unorganized players (on tea prices being deflationary).

Paints: Extended monsoon (in October), shorter festive season and pent-up/high inventory in the channel (in the base quarter) impacted volume growth across paint players in 3Q23. However, the latter half of December and January witnessed an improvement in demand with the outlook for Q4FY23F positive on favourable seasonality (exterior coating high margin business coming back).

Earnings estimates

Nomura expects FY24F momentum to be driven by a recovery in rural demand (on the stable macro scenario and favourable acreage) and steady improvement in urban demand (on premiumization, increase in the working population and upward mobility in incomes).

Pricing-led growth will be absent/minimal in FY24F, as it sees the companies driving volumes with softening / range-bound raw material prices. Competitive intensity should increase (A&P normalized and back at pre-COVID levels) with players making strong investments in market development and brand-building activities, it added.

The brokerage estimates 11.5 percent YoY revenue growth for the sector in FY24F.

It also forecasts FY24F to be a year of margin recovery with stable/range-bound input cost prices along with scale benefits on improving volume throughput. “We model in +110bp/+120bp YoY GPM/OPM improvement in FY24F,” said Nomura.

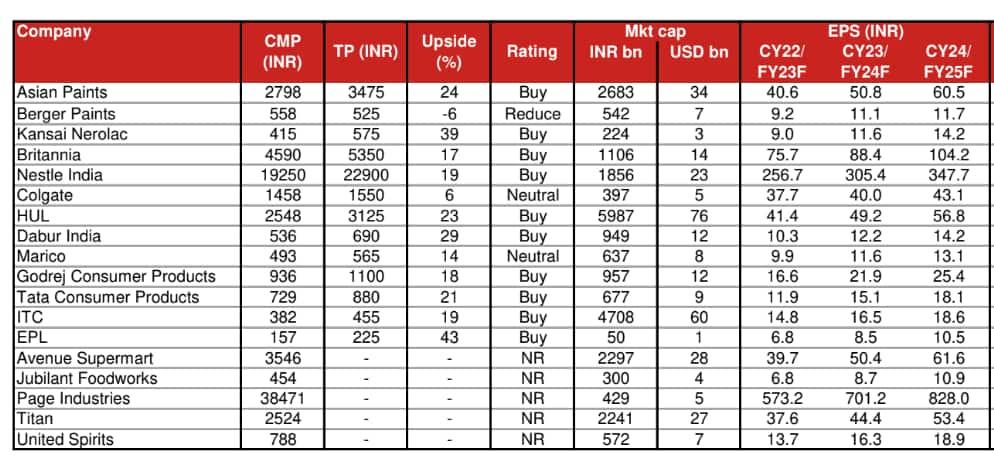

Top Picks

Nomura prefers companies that are demonstrating pockets of strength in the form of (1) superior growth (in volumes/pricing) trajectory than peers/industry (such as Britannia and HUL); (2) investments in distribution, digitization and R&D capabilities to support innovative new launches (such as Britannia, Godrej Consumer and HUL); (3) witnessing structural tailwinds despite volatile macros (such as ITC, Britannia and Godrej Consumer); and (4) having a leaner/efficient business model (such as HUL).

Its top picks in the sector are Britannia, Godrej Consumer, ITC, and HUL.