Global brokerage house Jefferies, in a recent note, said India had its Credit Suisse-like AT-1 bond issue around Covid when YES Bank wrote down AT-1 bonds. As such, the domestic bond market investors are not really concerned over the Indian stocks following the latest episode surrounding Credit Suisse, the brokerage noted.

"Indian financials have also borne the rub-off effect of global dislocations but they are better placed with a higher share of the retail deposit, limited ALM (asset liability management) gap & MTM (mark to market), limited dependence on AT-1 bonds & lower exposure to riskier segments like promoter/ acquisition finance. While equities and global bonds saw pressure of late, the local bond market is stable," stated the brokerage.

"The market has become polarised towards larger/ quality banks. Among banks, the top-3 issuers are SBI, HDFC Bank and Canara Bank with PSU banks having higher contributions from this. Interestingly, smaller banks have a lower contribution from AT-1 bonds," informed the brokerage.

A higher share of retail deposits and lower ALM gaps

This is another key positive for Indian banks, as per Jefferies. It pointed out that the deposit profile of Indian banks is highly dependent on household/retail deposits that form over 60 percent of total sector deposits. It further noted that the banks have also been increasing their focus on this segment to granularise deposits. ALM (asset and liability management) gaps, as measured by the share of <1yr liabilities vs. share of <1yr assets, are also limited. Even NBFCs have been watching this aspect much more closely post the debacle of IL&FS a few years before Covid, it added.

Interestingly on the bond side, while the prices of overseas bonds (issued by Indian issuers) have seen a correction, Jefferies noted that local bond experts/corporates indicate that the local market is fairly stable and price action will be a function of rate actions.

The lower risk from MTM and asset quality

Another point to keep in mind is that on the assets side of banks, loans form 65 percent and investments form 25 percent, mentioned the brokerage. Further, HTM (held-to-maturity) is allowed on GSecs and forms 80 percent of that and 15 percent of assets, it added.

On a 4-5 year duration, Jefferies observed that the impact of MTM (Mark To Market) loss on the HTM portfolio is 6 percent of net worth for private banks and 15 percent for state-owned banks, which is far lesser than what SVB has suffered. Indian banks are well placed, it said.

Asset quality trends were strong, with slippages during Q3FY23 at a multiyear low of 1.6 percent and recoveries from past NPLs helping to keep credit costs low at 1 percent of average loans, it added.

Valuations

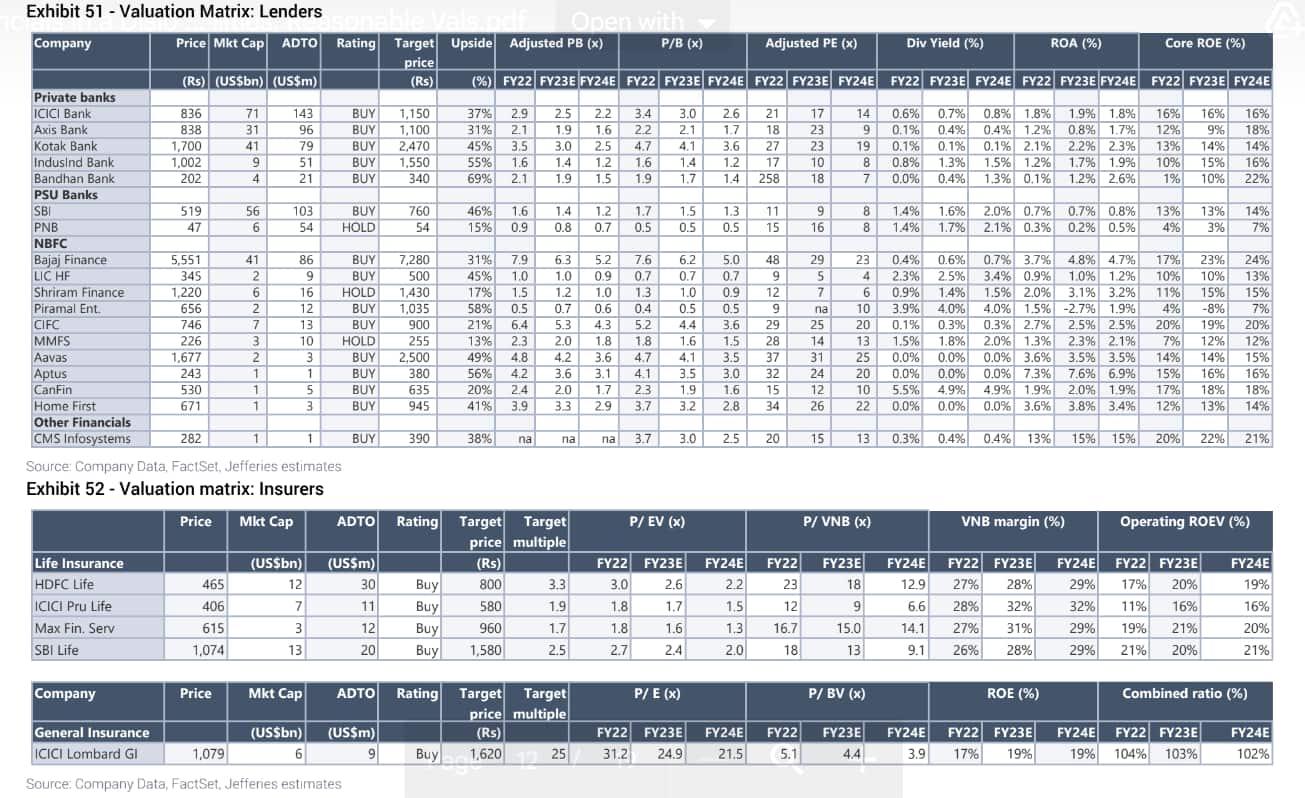

While the global events, especially in the financial sector, have stirred confidence and increased COE (cost on equity), the brokerage noted that the valuation of Indian banks is looking fairly attractive and in some cases, stocks trade below the levels during the height of Covid risk. Stocks above $5 billion in market cap that are trading below the Covid-low valuations are Kotak Bank, ICICI Prudential Life, ICICI General Insurance and HDFC Life, highlighted the brokerage.

ICICI Bank, IndusInd Bank, and SBI are its top bank picks; Bajaj Finance, and Chola are among the NBFCs. Life insurers are also attractive (and below Covid lows) but clarity on taxation of insurance policies will be key to rerating, it added.