After the stock crashed over 61 percent from its peak and around 35 percent in the last one year, brokerage house Motilal Oswal has turned positive on Teamlease Services (TEAM) on attractive valuations and long-term growth outlook.

The brokerage has upgraded the stock to ‘buy’ with a target price of ₹2,890, indicating an upside of 34 percent from its current market price of ₹2,149 (as on June 6, 2023).

"With current valuations focused on near-term challenges, we see scope for a re-rating in the stock as these challenges ease out. With healthy long-term growth prospects, margin recovery, closure of EPF issues and attractive share price, we see a good upside to current valuations and upgrade the stock to BUY with a target price of ₹2,890," it said.

The brokerage also stated that the staffing industry remains under-penetrated and is set to deliver consistent growth on account of formalisation and the implementation of labor law reforms over the medium term. But due to concerns about growth moderation, especially in the specialised staffing vertical, and margin pressure, the stock has seen significant de-rating, it noted.

The stock hit its all-time high of ₹5,550.00 in October 2021. It tanked almost 64 percent from its record high to its 52-week low of ₹2,012, hit in May this year (2023).

The stock is also down over 31 percent from its 52-week high of ₹3,816, hit in July 2022.

It has also shed 34 percent in the last 1 year and 15 percent in 2023 YTD, giving negative returns in 3 of the 6 months in the current calendar year.

The stock shed the most this year in March, down 11 percent and gained the most this year in Feb, up 9 percent.

However, from its COVID-low of ₹1,415.35, hit in March 2020, the stock has surged 71 percent to date.

Investment Rationale

Strong structural tailwinds: As per the brokerage, low flexi staffing penetration in India (0.6 percent) compared to developed economies like the US (3.4 percent) offers good headroom for growth. It also pointed out that progressive reforms and regulations will lead to formalisation and increased penetration for staffing companies in India. The formal workforce is expected to almost double by CY30 at 40 percent. Further, as both the central and state governments look to liberalise and formalise the labor market, TEAM should be among the biggest direct beneficiaries in the medium term, predicted MOSL.

Easing macro to revive growth: The brokerage noted that the staffing industry faced growth headwinds due to high inflation in FY23.

"While we see a slowdown in technology staffing (specialized staffing) and few parts of general staffing, the long-term outlook for the sector is robust. Inflation is easing, which should support growth in the near term. However, specialized staffing continues to face challenges due to a slowdown in IT Services, which is expected to see a recovery in 2HFY24, leading to a strong bounce-back for specialized staffing in FY25," it stated.

With a strong track-record of growth, easing inflation, an anticipated pickup in specialised staffing and structural tailwinds in place, MOSL expects TEAM to deliver a strong 17 percent revenue CAGR over FY23-25.

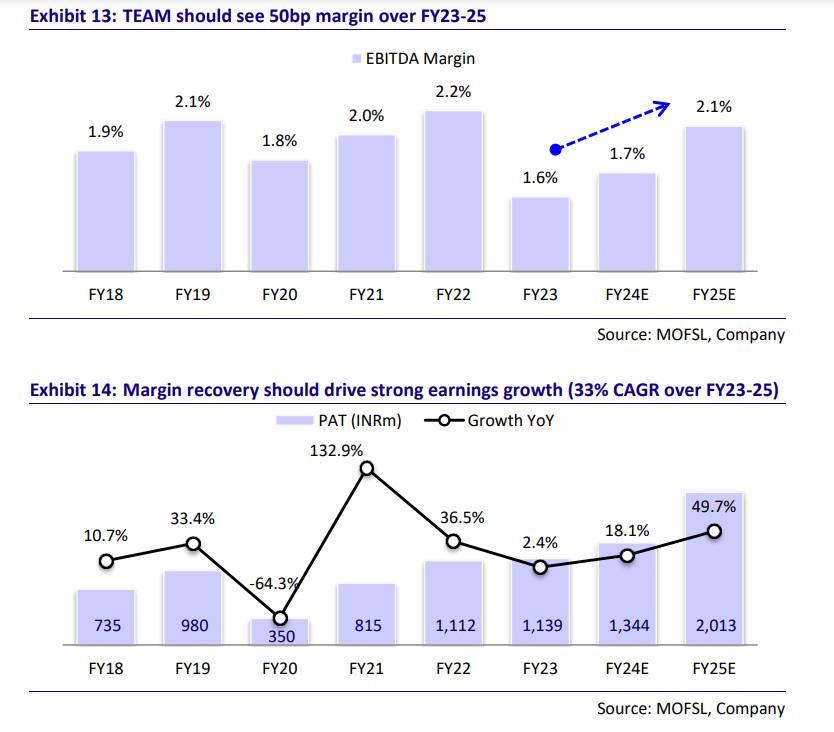

Strong margin recovery expected: The brokerage pointed out that TEAM has seen a 60 bps drop in profitability to 1.6 percent in FY23 due to wage increases in its general staffing vertical, but, the management continues to focus on improving productivity to bring cost efficiencies and re-negotiating contracts to boost PAPM (Profitability and Performance Management).

Along with the efficiency gains, revival in specialised staffing and increasing contribution from HR services (both high margin) should boost margins going forward, it predicted. MOSL views the current margin (1.6 percent for FY23) as the trough margin for TEAM and expects the company to gradually improve profitability over next few years (+50 bps over FY23 by FY25).

Valuations

Due to concerns about growth moderation and margin pressure, the stock has seen a significant de-rating and now the brokerage believes that valuations have bottomed out and already factor in near-term downsides.

It sees strong growth and expected margin recovery to help TEAM deliver a 33 percent earnings CAGR over FY23-25E, which should drive a significant re-rating in the stock.

With healthy growth prospects, EPF issues behind, margin recovery in place, and a sharp correction in the stock price, MOSL upgraded TEAM to BUY with a TP of ₹2,890, implying 25x FY25E EPS, a 10 percent discount to its 5-year median P/E (2-yr forward) on account of slow normalization of profitability.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.