As the digital penetration rises in India and more and more companies turn towards the internet to help support their businesses and increase demand, domestic brokerage house Elara Capital has initiated coverage on the space with ‘buy’ calls on IndiaMart InterMESH and Just Dial.

Elara initiates coverage in internet space; lists Justdial and IndiaMart as top picks; here's why

TL;DR.

Amid the rising digital penetration in India, brokerage Elara Capital has initiated coverage on the internet space with ‘buy’ calls on IndiaMart InterMESH and Just Dial.

With more and more Indian businesses turning digital, the percentage of online MSMEs (Micro, Small & Medium Enterprises) has risen from 32 percent in FY16 to 55 percent in FY20, the brokerage revealed quoting data from RedSeer. However, it added that this lags far behind other countries. To compare, in the US, 54 percent of small businesses used emails in 2017 and in China, 89 percent of the MSMEs were already digitally connected by 2015.

As per the brokerage, this indicates significant growth headroom in terms of digital connections in India alone.

It also noted that currently, only 4 percent of the MSMEs in India are truly digitally engaged. As per RedSeer, India's MSME digital services market is set to grow 6x in the next five years, taking the market opportunity from $1.5 billion to $9 billion by FY25, at a CAGR of 43 percent. About 73 percent of the growth is estimated to come from a surge in the number of digital businesses and 27 percent from higher average spending on digital services, it added.

"MSME business dynamics are seeing a paradigm shift, led by nuanced policy support and post-Covid recovery. Improving MSME credit growth, manufacturing revival, supportive government/RBI policies and rural demand traction enable a prolific seedbed for MSMEs. Moreover, a crest emerging off of Covid was the fast MSME digital adoption, add to which the Open Network for Digital Commerce (ONDC) variable may hasten MSME digital adoption," Elara believes.

For UPI too, transactions picked pace slowly initially but grew exponentially since 2020, or four years post the launch (528 percent jump in UPI volumes since Mar-2020). In 2020, UPI grew over 200 percent with over 1.5 billion transactions in December alone, highlighted the brokerage. This trend has continued in the following years, with UPI transactions growing further, driven by the increasing adoption of digital payments and the convenience offered by the platform. Elara expects a similar impetus to the participation of the masses in online transactions.

The brokerage further stated that India's B2B e-commerce market is still in its nascent stage. Although IndiaMart was launched two decades ago, there are not many players who have followed it in an evolving market, Elara observed. As per Redseer, India's B2B e-commerce market is estimated to have $18-19 billion size in CY23, with an estimated CY22-25 CAGR of 81 percent to $60 billion revenue by CY25.

Amid the back of the rising digital penetration in India, the brokerage prefers IndiaMart and Justdial in the digital space.

Peers

The brokerage noted that Indiamart and JDMart operate within the internet B2B (business-to-business) classifieds space/B2B e-commerce space. These are the first of their kind ‘internet’ companies from India in such spaces. Thus, Elara believes that it is fair to compare such companies valuation-wise with new-age internet companies such as Affle, Nykaa, Yelp, Bharat Matrimony (Matrimony), Zomato, and Infoedge (older peer).

Though the business/revenue model is different, they all are internet-based business/brand aggregators at their core, which compels a valuation comparison, it added. However, it cautioned that the underlying domains of these businesses are diverse and thus serve as constrained comparable peers.

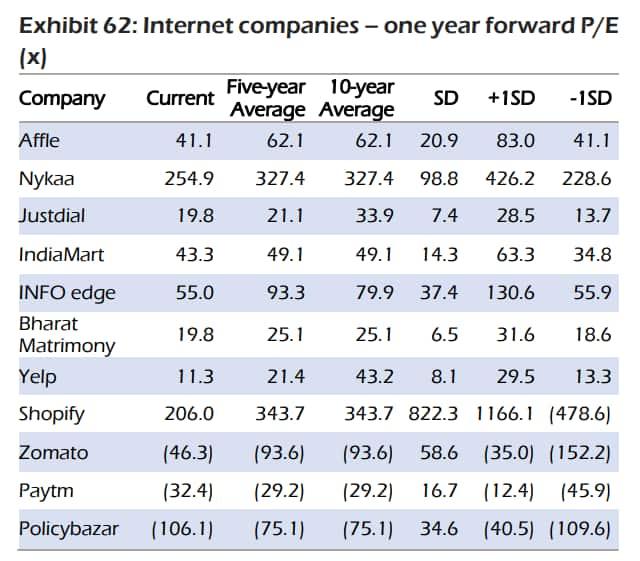

“The profitmaking peers trade at an average of 81.4x FY25E P/E, within a wide 16-115x range (Matrimony at the lower end and Nykaa at the upper end). In its view, BUY-rated IndiaMart, which trades at 43.3x 12m forward P/E (compared with its four-year average since the listing of 49.2x), is reasonably valued. Also, Justdial’s current one-year forward P/E is 19.8x, in line with its past five-year average of 21.1x and much lower than its 10-year average of 33.9x,” it stated.

Justdial's core business (excluding ₹3,930 crore cash) is trading at 12-13x P/E, far lower than that assigned to other internet businesses such as Affle, Nykaa, Indiamart, and Infoedge (41.1x/254.9x/ 43.3x/55x 12 month rolling forward P/E), highlighted the brokerage.

Source: Elara Capital

IndiaMART InterMESH

The brokerage has a ‘buy’ call on the stock with a target price of ₹5,700, indicating a potential upside of nearly 20 percent. As per the brokerage, Indiamart's leadership and strong business moats backed by a robust network effect and low digital penetration of MSMEs offer exciting growth prospects in the long term. The key risk is unfavorable technology-led market disruption, it added.

"IndiaMart is a market leader, enjoying a 60 percent market share in B2B digital marketing or the classified industry. The company’s superior matchmaking engine, robust network (74 lakh suppliers, 16.5 crore buyers and 9 crore products), and deep understanding of India’s online trade and commerce fortify its business moats, so as to leverage the structural opportunity in MSME digital adoption," noted the brokerage.

It further believes that the digitization of MSMEs (6x spike in FY20-25, as per Redseer) sets in a structural growth catalyst for the firm. Also, the ONDC (Open Network for Digital Commerce) initiative of the Indian government will boost the pace of MSME digitization by facilitating digital commerce infrastructure, it added.

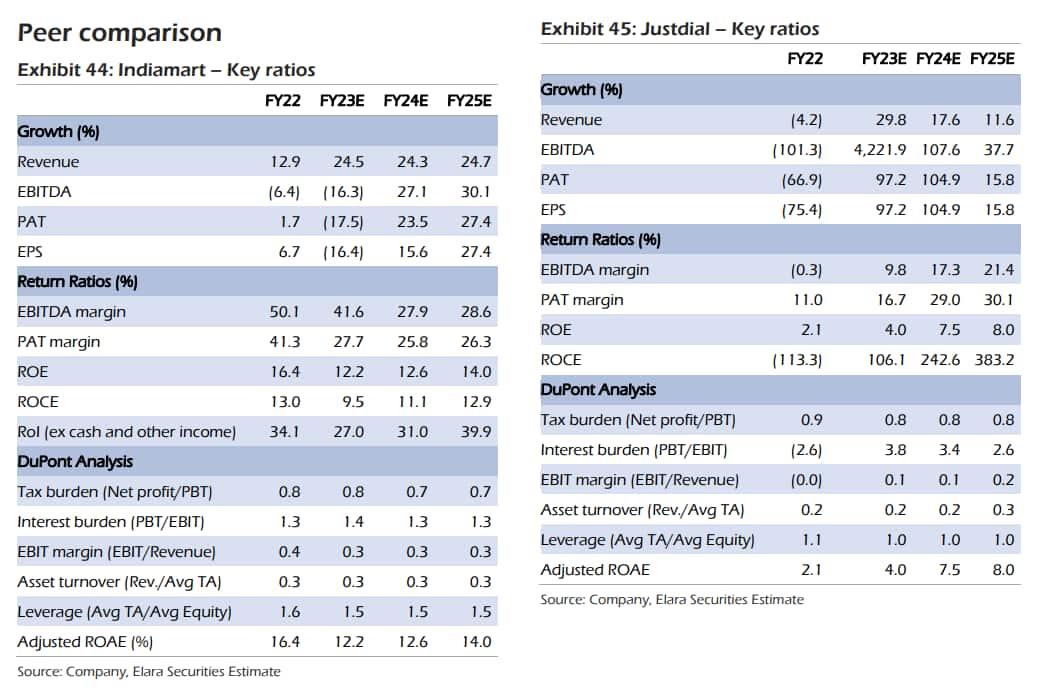

It forecasts a 24.5 percent revenue CAGR in FY23E-25E supported by a revamped sale engine, which underwent a transformation during Covid. It also expects operating margin to stabilize after post-pandemic cost base course correction in the past four quarters and expects margin stability to rekindle EPS growth from FY24, marking a trend change compared with a -16 percent EPS dip in FY23E. It estimates 29 percent/21 percent EBITDA and EPS CAGRs in FY23E-25E.

Justdial

The brokerage has initiated coverage with a ‘buy’ call on the stock with a target price of ₹825, implying a potential upside of 42 percent on account of attractive valuations, strengthening fundamentals, hefty cash on the balance sheet and strategic advantage from Reliance Retail Ventures (RRVL) parentage.

"Justdial (JD), a pioneer in local search and discovery business pan-India, is set to script a revival post-Covid-led loss. It is on a steady ‘margin improvement’ journey (post-Covid-led wipe-out), led by reduced employee cost, lower ad expenses and improved traffic addition. The RRVL backing is also expected to bring in strategic digitization impetus from Reliance parentage, which augurs well for the newly-started JDMart business," explained the brokerage.

Justdial saw a peak margin of 31.7 percent in Q4FY20 in the past five years, however, the brokerage informed that it dipped post that, reaching a trough of -10.4 percent in Q1FY22 led by: 1) hit to MSMEs on Covid-19 Wave II and 2) increased employee/ad spends.

Now with consistent YoY growth improvement over the past three quarters (from 12.2 percent in Q1FY23 to 39.3 percent in Q3FY23), steady YoY growth improvement in deferred revenues and overall progress in operating parameters – business listings, paid campaigns, revenue/paid campaign – Q3FY23 EBITDA margin at 12.3 percent is set on a strong growth trajectory, it forecasted.

Elara further highlighted that post the acquisition by RRVL, Justdial’s balance sheet saw a new lease of life post the ₹3,497 crore cash infusion. The RRVL parentage will bring in a strategic advantage for Justdial as Reliance has its own ecosystem of MSMEs on Jiomart, with its own digital ecosystem of partner MSMEs/merchants. This can unlock advantages for Justdial in the future, it observed.

Source: Elara

First Published: 23 Mar 2023, 02:31 PM IST