On the back of Indian markets hitting multiple highs and ahead of the June quarter results, many brokerage firms have initiated coverage on a number of stocks, mainly from the mid-and small-cap space. Most of these new initiations are with a positive outlook (buy/add) calls and an expected upside of up to 39 percent.

From Raymonds to Chalet Hotels, 13 stocks brokerages initiated coverage on with up to 39% upside potential

TL;DR.

On the back of Indian markets hitting multiple highs and ahead of the June quarter results, many brokerage firms have initiated coverage on a number of stocks, mainly from the mid- and small-cap space.

These stocks belong to various sectors such as cement, FMCG, auto ancillaries, pharma, fertilisers and retail. Let's take a look at the 13 stocks on which brokerages have recently initiated coverage:

UltraTech Cement: Axis Securities initiated coverage on the cement major with a ‘buy’ call and a target price of ₹9,350, indicating an upside of 11 percent.

"UltraTech Cement is the cement flagship company of the Aditya Birla Group and is the largest manufacturer of grey cement, ready mix concrete (RMC), and white cement in India. Excluding China, it is also the third-largest cement producer in the world and commands a robust market share of 22 percent in the Indian cement industry. Currently, it is in the process of expanding its existing capacity in India from 130 mtpa to 155 mtpa which will get operational in phases over FY24-FY26. The company reported robust Q4FY23 results on account of higher volumes and stringent control over operating costs. With ongoing capacity expansion, superior monitoring of cost drivers, and a strong demand environment, UTCL is expected to report Revenue/EBITDA/APAT CAGR of 9 percent//24 percent/32 percent, respectively over FY23-FY25. The said growth will be driven by the volume growth of 10 percent CAGR and realization improvement of 1% CAGR over FY23-FY25E," it explained.

CIE Automotive: Anand Rathi has initiated coverage on the stock with a ‘buy’ call and a target price of ₹635, indicating an upside of almost 21 percent.

With the increase in growth and addition of new products catering to EV space, the long-term growth prospects for the company are promising, said Anand Rathi. It expects the company to also gain from its parent’s expertise which could aid in increasing market share in the domestic EV (electric vehicle) value chain. On the growth front, the company aims to consistently grow faster than the overall markets with alpha in double digits, it noted, adding that the company’s new capacities are also expected to add to the growth. The brokerage expects an improvement in overall operating margins going ahead.

Sandhar Technologies: B&K Securities initiated coverage on the stock with a ‘buy’ call and a target price of ₹540, implying a massive 57 percent upside.

"STL is well positioned to outperform the industry, with an expected revenue compound annual growth rate (CAGR) of 16 percent over FY23-25E driven by enhanced product offerings, and new customer acquisitions. Manufacturing capacity built by STL over the last three years is expected to witness higher capacity utilisation on the back of strong growth. On the profitability front, absorption of start-up expenses, improved utilisation rate, and cost efficiency initiative is set to help the company improve its EBITDA margins to 10.3 percent by FY25E. Strong earnings growth of 48.7 percent CAGR (FY23-25E) will reduce the break-even levels, enable the company to reduce its net debt/EBITDA from 2.1x in FY23 to 0.9x in FY25E and enhance the company’s RoCE from 15.4 percent in FY23 to 23.2 percent in FY25," it explained.

Founded in 1987, STL is an auto-ancillary firm with a market share of 42 percent in two-wheeler Locking Systems, 35 percent in two-wheeler Visions and 70 percent in the Cabin and Fabrication (excavator) segment for Off-Highway Vehicles (OHV).

Electronics Mart: Equirus Securities initiated coverage on the stock with a 'long' rating and a target of ₹104, implying a 19 percent upside.

"Electronics Mart India (EMIL) is the fourth largest consumer durable retailer in India and the largest in the Southern region in terms of revenue. Over the years, strong brand connections, a loyal customer base, finest consumer experience have been the reason for the success of EMIL in the South market. Considering the growth potential of the Delhi – NCR market, EMIL has recently entered Delhi – NCR market post exit of some of the regional players. Revenue/EBITDA/ PAT has grown at a CAGR of 18%/12%/12% over FY19-23, which we expect to grow at a CAGR of 15%/16%/18% over FY23-26E. EBITDA margins are likely to remain at current levels only considering higher opex and lower throughputs of Delhi-NCR stores," it said.

Chalet Hotels: ICICI Securities has initiated coverage on Chalet Hotels with a ‘buy’ call and a target of ₹603, indicating an upside of 39 percent.

"While industry peers are focusing on the asset-light expansion route, Chalet has chosen to grow its hotel room and office rental portfolio over FY23-27E through the ownership route (mix of existing project expansion and long-term leases). We believe that this is the right strategy in an industry upcycle (FY23-FY28E) and we estimate the hotel EBITDA CAGR of 18 percent over FY23-26E at EBITDA margins of 44-45 percent. We believe that total operating cash flow of ₹2,210 crore over FY24-26E is adequate to fund incremental capex of ₹1,760 crore over the same period," explained the brokerage.

It estimates the company’s operational hotels to clock 11 percent revenue CAGR over FY23-26E and reach FY26E revenue of ₹1390 crore driven by 6 percent ARR CAGR over the same period and balance from occupancy ramp-up. Along with new hotels, it expects hotel revenue CAGR (existing + new) of 17 percent over FY23-26E.

JTL Industries: Axis Securities has initiated coverage on the stock with a ‘buy’ call and a target of ₹470, indicating an upside of 30 percent. JTL has been operating in the structural steel tubes and pipes business for the last 30 years, led by an experienced management team with over 30 years of experience in the steel and pipes industry, said Axis Securities.

As per the brokerage, JTL has four state-of-the-art manufacturing facilities dispersed geographically across India, which allows the company to source raw materials at competitive prices as well as enable it to expand its sales and footprint in domestic and international markets. It also noted that JTL is planning to expand its capacity from the current 0.586MT to 1MT by FY25 and it will be enhancing its VAP share from the current 31 percent in FY23 to 50 percent by FY25. Axis forecasts Revenue/EBITDA/PAT CAGR of 50%/45%/51% over FY23-25E, which will be led by higher sales volumes and VAP share on the increased capacity ahead. The company is funding the growth Capex by raising share warrants and targets a debt-free status by FY25, it added.

Five Star Business Finance: Nomura has initiated coverage on the stock with a ‘buy’ call and a target price of ₹750, indicating a 15 percent upside.

The brokerage house believes Five-Star Business Finance is uniquely positioned with superior growth and best-in-class profitability among financial peers. The company provides secured business loans to micro-entrepreneurs and self-employed individuals with a strong presence in South India. It estimates an EPS CAGR of 25 percent during FY23-FY26 with RoA and RoE of 7.7 percent and 16.6 percent, respectively.

Mankind Pharma: Kotak Institutional Equities initiated coverage on the stock with an ‘add’ rating and a target price of ₹1,875, a 12 percent upside.

As per the brokerage, the newly-listed company is well-positioned to continue to capitalise on gaps in the domestic branded prescription drugs as well as over-the-counter drug segments. Apart from marketing strengths, the company boasts a strong R&D, which is reflected in the success of Dydroboon, tablets used to treat female infertility and relieve menstrual pain, it said. Kotak expects a 15 percent domestic sales CAGR for the firm versus a 9-13 percent organic domestic sales CAGR for the rest of its coverage over FY2023-26E. It sees a 22 percent and 26 percent adjusted EBITDA and adjusted PAT CAGR, respectively, over FY 2023-26E — driven by an uptick across branded Rx (prescribed medicine), consumer healthcare and international segments.

Godrej Consumer Products: Emkay initiated coverage on the stock with a ‘Buy’ rating and a target price of ₹1,225, implying an upside of over 15 percent.

"We expect GCPL to trade at a premium to its historical P/E on account of enhancement in execution. Most of GCPL's categories have low penetration as well as low per-capita consumption. With economic growth, we expect a long runway of growth," it said.

Suzlon Energy: ICICI Securities initiated coverage on the stock with a ‘Buy’ rating and a target price of ₹22, indicating an upside of 20 percent. It believes Suzlon is best equipped to benefit from industry tailwinds and expects a sharp uptick in earnings from FY24E onwards. The brokerage expects a revenue CAGR of 37 percent to ₹11,200 crore over FY23-FY25E, EBITDA CAGR of 37 percent to ₹1,600 crore with an EBITDA margin of 14 percent, and PAT at ₹1100 crore in FY25E.

Raymond: InCred Equities initiated coverage on Raymond with an ‘Add’ rating and a target price of ₹2,200, indicating an upside of 28 percent.

"We feel Raymond is all set to deliver stellar growth led by enhanced segmental focus, improving operating metrics and key management-level changes. The company has taken successive moves to drive the group to debt-free status; at the same time, the promoter has been increasing its stake in the company’s subsidiary which displays high confidence. Success in stepping up in ethnic wear space and realty business also bodes well for the stock," it explained.

JB Chemicals and Pharmaceuticals: Jefferies initiated coverage on the stock with a 'buy' recommendation and a target price of ₹2,680, indicating a 14 percent upside.

"JB Chemicals is the fastest-growing domestic pharma company with therapy dominance in cardiac and gastro. We expect life cycle management of key brands, synergistic acquisitions and targeted new launches should allow JB Chemicals to outperform industry growth," it said.

Deepak Fertilisers & Petrochemicals: Philip Capital initiated coverage on the stock with a ‘Buy’ rating and a target price of ₹687, implying an upside of 20 percent.

"DFPC's story hinges on its ability to constantly offer improved products to its customers through persistent innovation. We expect growth over the medium term (FY24-25) to be driven by commercialization of two key projects – ammonia and TAN," it said.

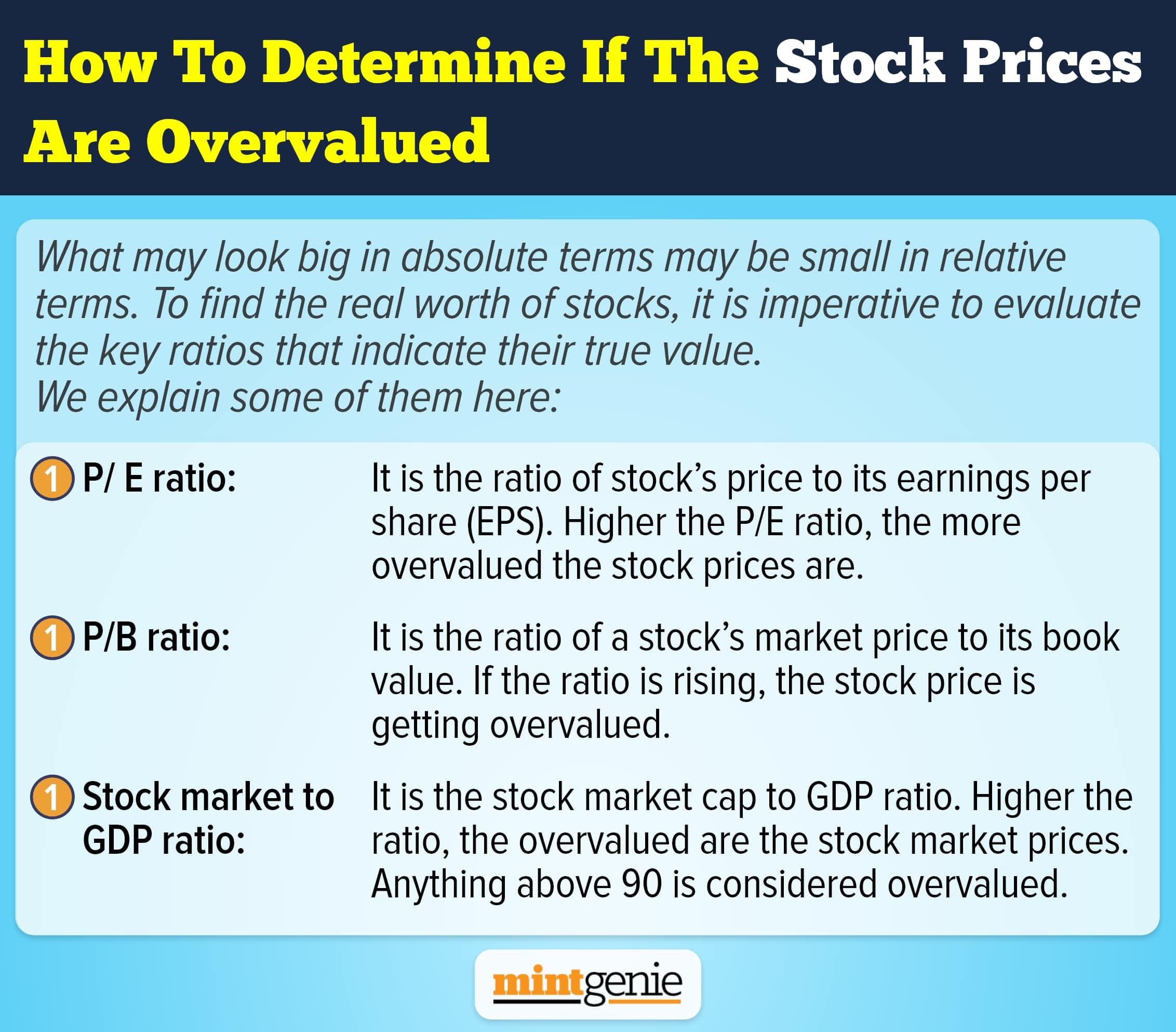

How to determine if the stock prices are overvalued.

First Published: 05 Jul 2023, 02:39 PM IST

Topics to follow

Related Stories

markets

PTC Industries stock zooms 68% in just one month, up 164% from August 2022 lows

A Ksheerasagar

Explain Like I am 5

markets

What is the significance of market capitalisation and how is it calculated?

Dhanya Nagasundaram