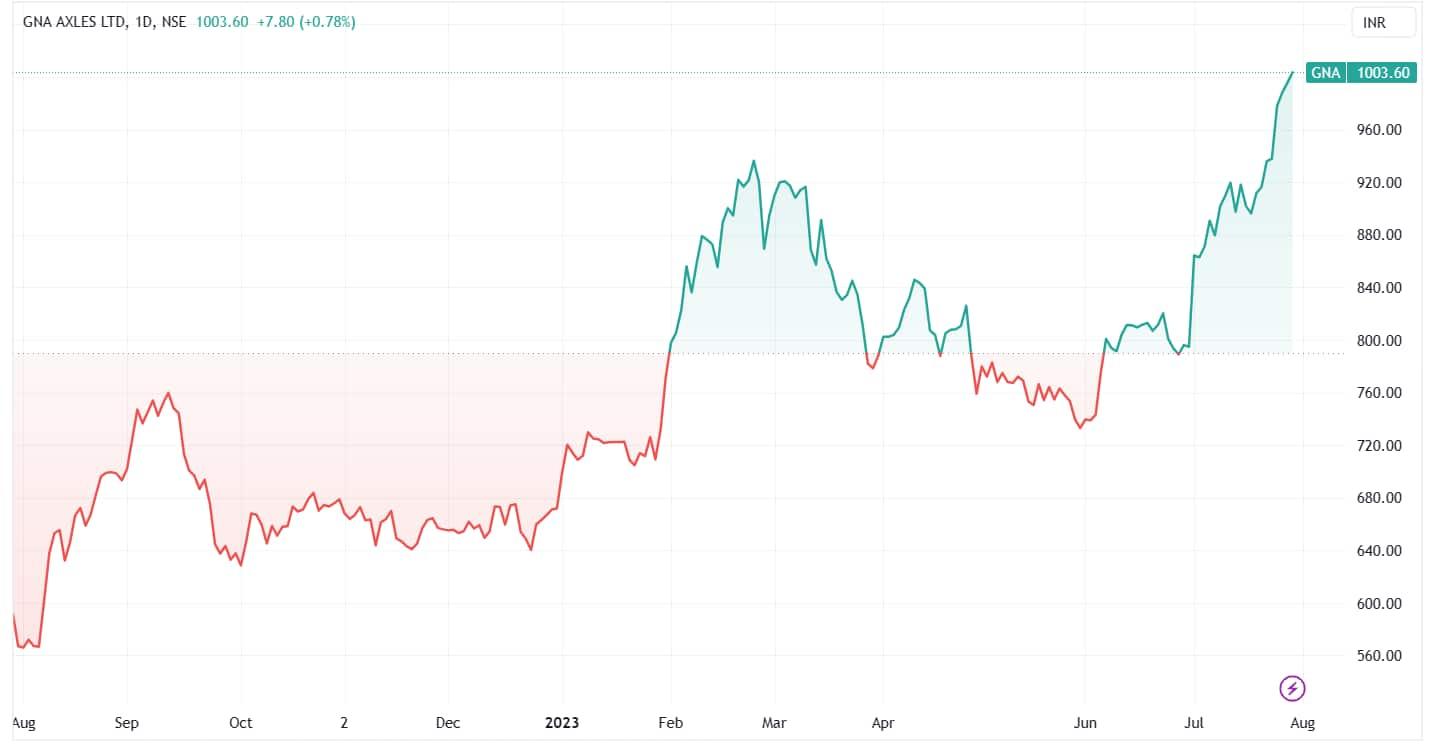

During Friday's trade, shares of GNA Axles, an auto ancillary company, continued their strong bull run by surpassing the ₹1,000 mark for the first time in nearly two years. They also achieved a new 52-week high of ₹1,008.60. This strong spike in shares came after the company's Q1FY24 performance beat analysts' estimates. Since its result announcement on July 21, the stock has zoomed 10% to date, and in the current month so far, it has rallied 26.3%.

The company is one of the leading manufacturers of rear axle shafts utilised in both on-highway and off-highway vehicular segments. In the on-highway segment, it offers a wide variety of rear axle shafts, other shafts, and spindles for light commercial vehicles (LCVs), medium commercial vehicles (MCVs), heavy commercial vehicles (HCVs), and other transportation vehicles such as buses.

In the off-highway segment, the company manufactures and supplies rear axle shafts and other shafts for agricultural tractors and machinery, forestry and construction equipment, electric cars, and other specialty vehicles used in the mining and defence sectors.

Following the company's Q1FY24 performance, domestic brokerage firm B&K Securities maintained its bullish outlook on the stock. Despite an 8.9% YoY drop in domestic tractor production volumes and flat domestic MHCV volumes, GNA Axles achieved a net revenue of ₹374 crore (flat YoY), benefiting from market share gains in the domestic MHCV and tractor segments, said the brokerage.

The company reported EBITDA at ₹59 crore, a 17.1% YoY increase, while the EBITDA margin improved by 240 bps YoY to 15.8%, driven by declines in raw material costs and other expenses. The company reported a profit after tax (PAT) of ₹33.1 crore, a 22.5% YoY growth, reflecting strong operating profits, it noted.

Looking ahead, B&K Securities anticipates a stable tractor demand despite the high base from the previous year, supported by steady water reservoir levels and improved Minimum Support Prices (MSP).

The brokerage expects GNA Axles to outperform the domestic tractor industry, driven by increased demand from multinational customers like Escorts and John Deere, leading to higher export orders. The brokerage also foresees a significant increase in volumes from the LCV/SUV segment due to new customer wins.

In overseas markets, the brokerage expects industry demand to remain stable throughout the year, benefiting from the expected increase in Sales Order Booking (SOB) with DANA Corp, resulting in improved volume growth for GNA.

Over the next two years (FY23–25E), the brokerage expects the company to report a strong earnings CAGR of 10%, mainly fueled by increased SOB with customers, new customer acquisitions, and ramping up production volumes in the SUV segment.

Moreover, the company's focus on the SUV and off-road vehicle segment in overseas markets will serve as a shock absorber, limiting volume declines during downcycles, it added.

To support its future growth trajectory, GNA Axles plans to expand its capacity by 2 million units (to 8.7 million units) with a capital expenditure of ₹2 billion in the next two to three years.

Maintaining their confidence in the company's performance, B&K Securities forecasts GNA Axles to maintain EBITDA margins at levels of over 14.5% for the next two years. In light of these growth factors, it maintained a 'buy' call on the stock with a target price of ₹1,123 apiece.

Meanwhile, taking the current trading price of ₹1,003 into account, the stock is trading 384% higher than its IPO price of ₹207. The company's shares made their debut on Indian exchanges on September 2016.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.