IT major HCL Technologies reported a disappointing set of earnings for the April-June quarter (Q1FY24). The IT major's Q1 earnings missed the Street's estimate on both profit and revenue front.

HCL Tech: Should you buy the stock after Q1 results? Here's what experts say

TL;DR.

IT major HCL Technologies reported a disappointing set of earnings for the April-June quarter (Q1FY24). The IT major's Q1 earnings missed the Street's estimate on both profit and revenue front.

Even though the company posted a 7.6 percent year-on-year (YoY) rise in its Q1 net profit at ₹3,534 crore, on a sequential basis, the profit fell 11.2 percent. Meanwhile, its revenue was up 12 percent YoY to ₹26,296 crore in the quarter under review, but it also declined 1.2 percent sequentially on the back of a slowdown in deals and verticals like hi-tech and telecom.

The order booking also fell 24.5 percent QoQ to $1.6 billion, however, the firm maintained its revenue guidance of 6-8 percent for FY24 in CC (constant currency) terms and operating margins of 18-19 percent.

C Vijayakumar, HCL Tech CEO, commented on the results, saying that while Q1 is traditionally a slow quarter for the company due to productivity benefits for many contracts starting to kick in during the quarter, the performance has been "lower than our own expectations".

Stock Price Trend

While the stock fell 2 percent in morning deals to ₹1,087.75 after its weak Q1 results, it later turned green, up 1 percent, on the back of overall positive market sentiment to ₹1,124.70.

HCL Tech has risen over 23 percent in the last 1 year and 7 percent in 2023 YTD.

The stock has shed over 6 percent in July so far, snapping 2 months of gains. It has risen in 4 of the 7 months in this calendar year so far.

Meanwhile, in the long term - 3 years, the stock has advanced over 88 percent.

HCL Tech stock price trend

What brokerages say:

Brokerages remained mixed on the stock. While some retained ‘buy’ on the long-term growth prospects, others had ‘hold’ calls on the stock.

Motilal Oswal

The brokerage reiterated its ‘buy’ call on the stock with a target price of ₹1,280, indicating an upside of 15 percent. Given its capabilities in the IMS and Digital space, along with strategic partnerships and investments in Cloud, MOSL expects HCL Tech to emerge stronger on the back of healthy demand for these services in the medium term.

Higher exposure to Cloud, which comprises a larger share of non-discretionary spending, offers better resilience to its portfolio in the current context, with higher demand for Cloud, Network, Security, and Digital workplace services, it added.

"Our positive view on HCLT remains tethered to its defensive business profile, which should support the company in a demand-constrained environment. This is visible in the company’s strong topline expectation between Q2-Q4 (3 percent QoQ CQGR), among the best in our Tier 1 coverage despite factoring in growth below the management guidance. Moreover, the stock is currently trading at an inexpensive valuation of 16.5x FY25E EPS (4.7 percent Payout yield) and any near-term correction due to the Q1 miss should make it even more attractive. We have lowered our FY24/25 EPS estimates by 1-2 percent to account for the 1Q miss. Reiterate BUY with a TP of ₹1,280 (based on 19x FY25E EPS)," it said.

Nuvama

The brokerage also has a ‘buy’ call on the stock with a target price of ₹1,300, indicating an upside of 17 percent.

According to Nuvama, HCL Tech's strong growth in services and lower exposure to the troubled BFSI segment imply a high probability of stable earnings growth. It also believes that a high dividend yield and inexpensive valuation make the stock attractive at current levels

Though the brokerage feels that weak performance in Q1 makes meeting its FY24 guidance a tall ask for HCL Tech, it said that the company will still remain one of the fastest-growing large-cap IT majors even if it misses its guidance.

HDFC Securities

The brokerage has an ‘add’ call on the stock with a target price of ₹1,230, indicating an 11 percent upside.

"HCL Tech (HCLT) posted a weak Q1 but maintained its FY24E guidance (both on growth and margin). The revenue miss was largely due to ER&D services and the Telecom & Media vertical which had an aggregate revenue impact of -1 percent and -1.3 percent QoQ due to cuts in discretionary spending. We reckon that HCLT’s annual revenue guidance of 6-8 percent growth will be at the lower end (including inorganic) and the margin can still be closer to the mid-point (deferral/cancellation of wage hike). HCLT’s growth acceleration in H2FY24 has to be fairly steep to meet the guidance and offset the headwinds in Q2 of soft Q1 bookings and full-quarter impact of the Telecom vertical (guidance implies CQGR of 2.8 to 4 percent over Q2-Q4FY24E)," it said.

The brokerage has factored in a dollar revenue growth at 6.1 percent, 9.9 percent, and 8.1 percent for FY24E, FY25E and FY26E, respectively. Meanwhile, it estimates EBIT Margin at 18.3 percent, 18.8 percent and 19 percent respectively for FY24E, FY25E and FY26E, translating to 10 percent EPS CAGR over FY23-26E. Better capital allocation and cash generation support valuation (17x FY25E), it added.

Axis Securities

The brokerage has a ‘hold’ call on the stock with a target price of ₹1,200, indicating an 8 percent upside. Global uncertainties leading to delayed spending decisions pose a challenging environment to HCL Tech and will impact its performance in the near term, it said, adding that the supply-side constraints will take some more time to ease off.

"The near-term outlook for IT services still remains skeptical due to delayed decision-making and prevailing uncertainties in North America. On the positive side, the long-term demand scenario continues to remain strong and the IT sector is likely to regain its momentum in H2FY24 and onwards. The management is also confident of gaining medium-term demand momentum, supported by the deals it has won in the previous quarters. It also foresees improvement on the company’s margin front going forward," stated Axis.

InCred Equities

The brokerage retained its ‘hold’ rating but cut its target price to ₹1,125 from ₹1,133 earlier. The new target indicates a 1.3 percent upside.

"We retain a hold rating with a lower target price of ₹1,125 ( ₹1,133 earlier) as we bake in Q1FY24 miss and ASAP acquisition contribution in H2FY24F. We now model in a 7.8 percent US$ revenue CAGR (vs 8.1 percent earlier) over FY23-25F and a 10.5 percent PAT CAGR (vs 10.6 percent earlier). The 75 percent dividend payout ratio and 4 percent dividend yield could anchor the stock. Acceleration in deal velocity, lower attrition and product and platform (P&P) business improvement are upside risks. Weak execution is a key downside risk," it said.

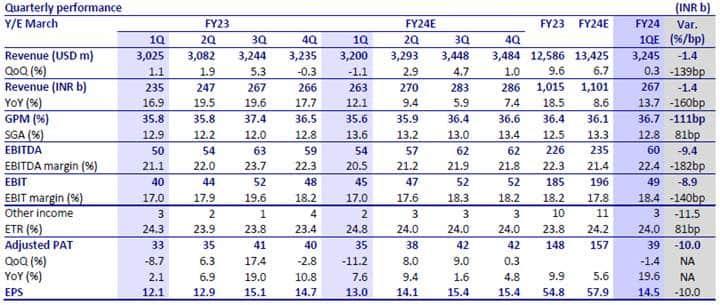

Source: MOSL

First Published: 13 Jul 2023, 03:27 PM IST