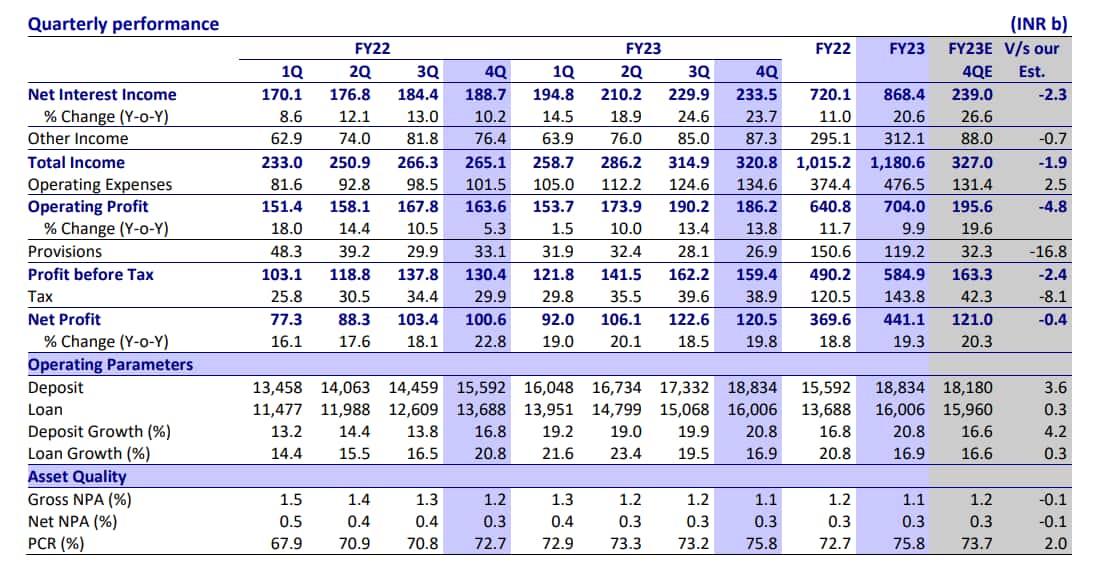

Private sector lender HDFC Bank reported in-line earnings for the March quarter of FY23 (Q4FY23). Its consolidated net profit jumped 21 percent year-on-year (YoY) to ₹12,594.5 crore. The bank also posted a 20.3 percent YoY rise in consolidated net revenue to ₹34,552.8 crore during the quarter under review versus ₹28,733.9 crore in the same quarter last year.

HDFC Bank Q4 Review: Should you buy the stock after March-quarter results? Here's what brokerages say

TL;DR.

On the asset quality front, Gross NPA (non-performing assets) and Net NPA ratios improved to 1.12 percent (1.17 percent in Q3FY22)and 0.27 percent (0.32 percent, a year ago), respectively, as slippages moderated to ₹4,900 crore (1.3 percent of loans).

Meanwhile, its net interest income (NII) advanced 23.7 percent to ₹23,351 crore as against ₹18,872 crore in the year-ago period.

On the asset quality front, Gross NPA (non-performing assets) and Net NPA ratios improved to 1.12 percent (1.17 percent in Q3FY22)and 0.27 percent (0.32 percent, a year ago), respectively, as slippages moderated to ₹4,900 crore (1.3 percent of loans).

Provisions and contingencies for the quarter ended March 31, 2023, were ₹2,685.4 crore as against ₹3,312.4 crore for the quarter that ended March 31, 2022. The pre-provision operating profit (PPoP) rose 14.4 percent YoY to ₹18,621 crore.

Most brokerages retained their ‘buy’ calls on the stock and raised their target prices post the lender's Q4 results. Let's see what various brokerages have to say:

Elara Capital

The brokerage has maintained its ‘buy’ call on the stock and raised its target price to ₹2,009 (earlier ₹1,925) post the Q4 results, indicating an upside of 19 percent.

"HDFC Bank is facing concerns about deserving a premium, post the merger (challenged differentiation unlike earlier cycles). But given its strong execution track and underlying strength in each business, such concerns may most likely be unfounded. Better performance in the run-up to the merger makes us comfortable on post-merger outcomes. We believe RBI dispensations may favor the bank (benefit excluded in our forecast). HDFCB is one of our top picks," it said.

The brokerage believes that FY24 will be characterized by the nature of balance sheets and deposit franchises. Add to that, the impending merger for the bank made deposit mobilization quintessential and essentially, the most discussed point with investors, it said.

However, it added that the merger outcome may take precedence over business performance in the near term. Given the nature of these, the impact is hard to gauge, and the outcome is contingent on regulatory action/market condition, noted Elara.

Emkay

The brokerage believes HDFC Bank offers the best play on India's consumption story notwithstanding the merger-related regulatory overhang and is also a good defensive bet in current choppy waters. It has retained a long-term ‘BUY’, with a revised target of ₹2,050/share vs ₹1,925. The new target indicated a potential upside of 21 percent.

Despite the healthy NII growth, HDFC Bank reported moderate core PPoP growth at 14 percent YoY, mainly due to higher opex as the bank continues to invest heavily in franchisee network, and customer acquisition, noted the brokerage. However, higher fees including TPD (Transaction Processing Division) and lower credit costs led to in-line profitability, at ₹12,000 crore (up 20 percent YoY), it added.

The brokerage has slightly cut the FY24E earnings, by 1 percent, factoring in the elevated costs, but expects the standalone bank to deliver a superior RoA/RoE of 2 percent/17-18 percent over FY24-26E. Bank expects the merger to close down by July 2023, once RBI approval is in place which Emkay believes will be critical from the point of view of the merger's structure, including clarity on HDFC Life stake/merger of NBFC subsidiaries and regulatory dispensations, if any.

ICICI Securities

The brokerage has retained its ‘buy’ call and revised its target price to ₹1,990 from ₹1,874 earlier. The new target price indicates an upside of 17.5 percent.

"HDFC Bank’s Q4FY23 PAT at ₹12050 crore, up 19.8 percent YoY but down 1.7 percent QoQ, was broadly in line with I-Sec estimate. NII growth for the four quarters of FY23 averaged 20.4 percent vs 11 percent for FY22. On the contrary, opex growth for the four quarters of FY23 averaged 27.2 percent vs 14.7 percent for FY22. Hence, it can be inferred that the bank utilised gains from higher NII to make investments for the future, which led to elevated opex. Profitability thereby was stable with FY23 RoE at 17.4 percent vs FY22 RoE at 16.9 percent. The merger with HDFC is likely to come into effect from Jul’23, as per the management," said the brokerage.

Nirmal Bang

The brokerage retained its ‘buy’ call for the stock with a target price of ₹1,958, indicating an upside of 16 percent.

"We expect balance sheet growth momentum to remain healthy, but higher cost and increasing funding costs are likely to put some pressure on earnings growth going forward. We remain cautious about merger transition, which along with elevated opex and the margin trajectory would be a key monitorable going forward," stated Nirmal Bang.

Motilal Oswal

The brokerage maintained its ‘buy’ call on the stock with a target price of ₹1,950, indicating an upside of 15 percent.

HDFCB reported an in-line quarter with PAT up 20 percent YoY, supported by healthy NII growth and lower provisions. NIMs stood stable QoQ, said MOSL. Strong demand for Commercial and Rural Banking, and Agriculture, Corporate and Retail loans led to a healthy QoQ growth in the loan portfolio. Deposits also showed strong traction, it noted.

Further, MOSL pointed out that asset quality ratios also improved as slippages moderated. PCR improved to 76 percent, which coupled with a contingent provision buffer, should support asset quality, it stated.

"We uphold our earnings projection and estimate a 19 percent PAT CAGR over FY23-25, with RoA/RoE at 2 percent/17.7 percent in FY25. A potential pick up in margins and progress on the merger would be the key monitorables," it predicted.

Phillip Capital

The brokerage has retained its ‘buy’ call on the stock with a target price of ₹1,950, indicating an upside of 15 percent.

"Results were below our expectation as operating expense elevates further. The near-term business strategy would revolve around creating enablement for smooth amalgamation, hence growth in deposit and retail loans including SME/Agri would take center stage. The regulator’s view on key issues (like Stake in HDFC Life; approval to keep HDB Fin as a subsidiary; any regulatory dispensation on priority/SLR/CRR etc ) would be important events for the bank in the next 3 months. We remain constructive on the bank with mid to long-term perspective," said the brokerage.

As the benefits accrue over a period, the brokerage believes the intermittent period will see merger-related costs in the form of pressure on margins and cost-to-income ratio. The return on equity is expected to moderate in the near term owing to the low leverage of the parent, however, it expects RoA to sustain at a 1.9 percent level.

Source: MOSL

First Published: 17 Apr 2023, 03:09 PM IST