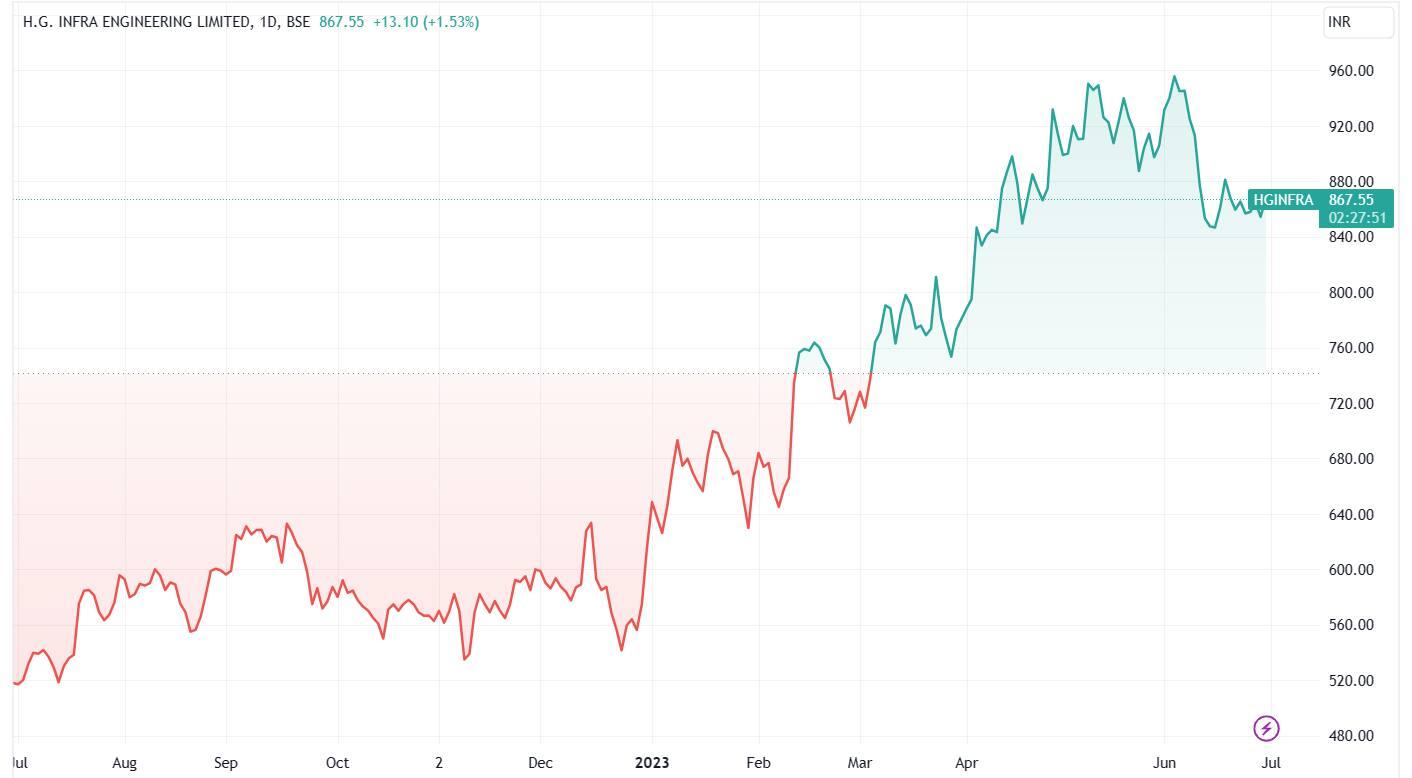

H.G. Infra Engineering, a road infrastructure company, has witnessed an impressive surge in its share price over the last one-year period, climbing from ₹519.70 to ₹865.25, reflecting a stellar gain of 64.5%. Notably, a significant portion of this rise, around 40%, has been achieved in the last five months, following the company's successful acquisition of multiple orders.

On May 02, the stock crossed the ₹900 mark for the first time, and in the following seven trading sessions, it gained 5% to record a historic high of ₹978. This recent upward momentum in the stock has resulted in a 122% gain over the past two years and a staggering 330% gain over the last three years.

Looking ahead, Emkay Global, a leading domestic brokerage firm, believes that the stock has the potential for further upside of over 30.6% from its current trading price.

Let's delve into the factors behind the brokerage's optimistic outlook.

Demonstrated profitable execution capabilities: During the last 5 years, the brokerage said the company has clocked 28%/38% EBITDAM/CAGR, with 23% order book growth over the same period. This, according to the brokerage, has been possible on the back of a disciplined project-bidding strategy and investment in a modern construction equipment fleet. RoE has been more than 20%, with NWC (net working capital) in the 25–45-day range, it noted.

Diversification has already started: The company's relentless bidding for non-roads sector projects for some time now has finally seen success, with a ₹15 billion order inflow during FY23. The company is focusing on rail, metro, and water projects in key states and targets achieving 20–25% inflow from the non-roads sector in the next few years, the brokerage stated.

This will alleviate concerns about H.G. being a single-sector EPC player. The brokerage said that opportunity size will grow along with valuations.

Monetization of HAM projects a confidence booster: In addition, the company has recently entered into a share purchase agreement for four HAM projects at 1.55x P/B. Emkay Global views this as a clear demonstration of the company's prudent bidding strategy for HAM projects.

Road tenders have seen 25% growth in 1QFY24 to date: The roads sector has witnessed a 25% growth in tenders during the April-May '23 period, which is expected to lead to order finalizations in the coming months.

Additionally, healthy tendering data for rail and water supply projects further strengthens the outlook. Emkay Global believes that H.G. Infra Engineering will be able to achieve an order inflow of ₹80–90 billion.

Valuation: Emkay Global believes that H.G. Infra Engineering's diversification strategy will significantly expand the opportunity size for the company in the EPC sector over the medium term, leading to an improvement in the price-to-earnings ratio (PER). Therefore, it has maintained a 'buy' rating on the stock, with a target price of ₹1,130 per share, reflecting an upside of 30.6% from the stock's current trading price.

Established in 2003, H.G. Infra Engineering is engaged in the business of engineering, procurement, and construction (EPC) services, maintenance of roads, bridges, flyovers, and other infrastructure contract works.

The company's customer base includes government bodies such as the National Highways Authority of India (NHAI) and the Ministry of Road Transport and Highways (MoRTH), as well as private road developers like IRB Infrastructure Developers Limited, Tata Projects Limited, and Adani Road Transport Limited.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.