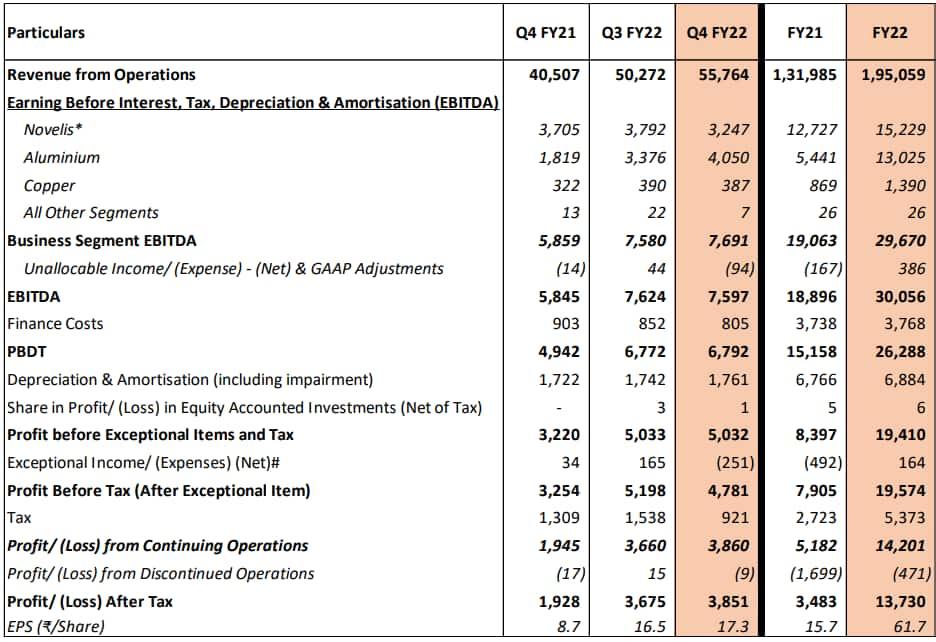

Hindalco Industries, the flagship metals company of the Aditya Birla group, reported a 100% rise in its consolidated net profit at ₹3,851 crore in the March quarter, compared with ₹1,928 crore in the same quarter last year.

Consolidated revenue for the fourth quarter increased 38% to ₹55,764 crore, up from ₹40,507 crore in the same quarter last year.

While EBITDA increased by 30% year on year to ₹7,597 crore.

The company also declared a dividend of ₹4 per equity share (400% of the face value of ₹1 each) for the financial year 2021–22 (FY22).

As per the company, the strong growth in both the top and bottom line was driven by an exceptional performance in the company's India business. Adding to that, favourable macros, strategic product mix, and an improved downstream business also contributed to the earnings rise.

"With record profitability in the fourth quarter, we had a very good end to the year." We attribute Hindalco’s highest-ever profits not just to strong macros but also to our consistent focus on operational excellence and cost optimization. "We continue to remain one of the world’s lowest-cost and highest EBITDA margin producers of aluminium," said Mr. Satish Pai, Managing Director, Hindalco Industries.

"Our growth strategy will continue to be shaped by our 2050 ESG goals – achieving Net Zero in carbon emissions, effluent discharge, biodiversity loss, and waste to landfill. "To sum up, Hindalco sees a positive horizon, which inspires us to invest in future-centric growth projects," he added.

Business Segment Performance in Q4 FY22

Aluminium

The Aluminium India business reported an all-time high quarterly Ebitda of ₹4,050 crore, up 123 per cent year on year.

Aluminium segment revenue was 9,847 crore in Q4 FY22, up from 5,969 crore the previous year.

Copper

Revenue from the Copper Business stood at ₹9,787 crore in the March quarter, up 15% YoY, primarily due to higher global prices of copper and higher volumes.

EBITDA for the business stood at ₹387 crore in Q4 FY22 compared to ₹322 crore in Q4 FY21, up 20% YoY.

Novelis

Novelis, a Hindalco subsidiary that makes flat-rolled aluminium products, reported net income from continuing operations of $217 million, up 21 per cent YoY, mainly driven by lower interest expense in Q4.

Novelis reported quarterly adjusted EBITDA of $431 million (vs. $505 million), a 15% decrease year on year. In Q4 FY22, Novelis reported an adjusted EBITDA per tonne of $437, down from $514 the previous year.

Novelis' revenue for the quarter was $4.8 billion, up 34% year on year, due to higher global aluminium prices.

The Novelis group has recently announced a capital expenditure (Capex) of $2.5 billion to build a new recycling and rolling plant in the US, in the largest greenfield expansion plan by the Aditya Birla group.

Financials

Stock Performance

The stock has declined 4.46% in a week, 16.73% over a month, and 12.2% in the calendar year 2022 on a year-to-date (YTD) basis.

However, In the last one year, the stock has delivered nearly 6.25% returns to its shareholders.

Brokerage Views

Global brokerage Macquarie has maintained an 'outperform' rating on the stock with a target at ₹689 per share, implying an upside of 67.63% from the current CMP.

While JP Morgan has kept the 'overweight' rating with a reduced target to ₹565 from Rs. 600 apiece.

Motilal Oswal has reduced Hindalco's consolidated EBITDA/PAT estimate by 16%, owing to a 28% reduction in India's EBITDA due to higher coal costs."We expect the coal crisis to dissipate in the next one-to-two quarters," it said.

The brokerage house maintains its 'buy' rating with a SoTP-based target price of ₹555 per share, representing a 35.03% increase from the current CMP. An extended coal crisis remains the key risk, it added.

An average of 20 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.