Private sector lenders Axis Bank and ICICI Bank, both have been in focus after reporting a strong set of numbers for the third quarter of FY23 on the back of improvement in asset quality, better loan growth and higher net interest income (NII).

ICICI Bank vs Axis Bank: Which is a better long-term investment?

TL;DR.

Private sector lenders Axis Bank and ICICI Bank, both have been in focus after reporting a strong set of numbers for the third quarter of FY23. Let's see which of these two private sector lenders is a better long-term investment.

Banks, overall, have been on a rise on the back of the expansion of loan portfolios and the decline in nonperforming loans.

Let's see which of these two private sector lenders is a better long-term investment:

Stock price trend

While ICICI Bank has risen 7 percent in the last 1 year, Axis Bank has advanced nearly 19 percent in this period. Both the lenders have been in the red in January till date with ICICI Bank down 8 percent and Axis Bank down 7 percent.

However, in the previous month, December 2022, Axis was in the green, up 3.6 percent whereas ICICI shed 6.5 percent.

In the 12 months of 2022, ICICI Bank was in the red in 5 of those months whereas Axis fell in 6. The highest decline in ICICI was seen in June when it lost 6 percent. For Axis also, that was in the month of June, when it lost 7 percent. However, the highest gain was witnessed in October by Axis Bank, up 23.5 percent and in July by ICICI, up 16 percent.

From a long-term perspective, ICICI Bank has outperformed Axis in the last 3 years. ICICI has jumped 55 percent in this time while Axis has added 18 percent.

ICICI Bank stock price trend

About the firms

ICICI Bank is a large private-sector bank in India. It offers a diversified portfolio of financial products and services to retail, small and medium-sized enterprises (MSE), and corporates. Through its subsidiaries, it has a wide presence across financial services such as insurance, asset management, merchant banking, and brokerage. The bank leverages technology to offer financial services through digital channels such as internet banking, mobile banking, and digital banking kiosks.

Axis Bank, on the other hand, is the third-largest private sector bank in India. It offers an entire range of financial products to its key customer segments such as large and mid-corporates, micro, small and medium-sized enterprises (MSME), agriculture, and retail. The bank also offers asset management and brokerage services through its subsidiaries. It has been at the forefront of offering digital banking services to its customers and is adopting new technologies such as the cloud to improve the customer experience.

Earnings

In the third quarter, ICICI Bank reported a 34.19 percent year-on-year (YoY) growth in its net profit at ₹8,311.85 crore against a profit of ₹6,193.81 crore in the same quarter a year ago. Its NII jumped by 34.6 percent YoY to ₹16,465 crore in Q3FY23, against ₹12,236 crore in the same quarter last year. Net interest margin (NIM) also increased to 4.65 percent in Q3 of the current fiscal compared to 3.96 percent in Q3FY22.

Its asset quality also improved during the quarter. Gross NPA dropped to 3.07 percent as of December 31, 2022, from 4.13 percent as of December 31, 2021. The net NPA ratio declined to 0.55 percent in Q3FY23 from 0.85 percent in Q3FY22.

Meanwhile, Axis Bank's net profit for Q3FY23 surged 62 percent YoY to ₹5,853 crore on the back of strong loan growth and high net interest income (NII). The lender reported a profit of ₹3,614 in the same quarter last year. Its NII rose 32.4 percent YoY to ₹11,459.3 crore and NIM further improved by 30 bps sequentially to 4.26 percent for the quarter ended December 2022.

Asset quality of the bank also improved with gross non-performing assets (NPAs) during the quarter under review at 2.38 percent versus 2.5 percent in the year-ago quarter. Meanwhile, the net NPA ratio declined to 0.47 percent, while PCR improved to 81 percent in Q3.

Axis Bank stock price trend

Which is a better long-term investment?

Anil Rego- Founder and Fund manager at Right Horizon PMS believes both lenders have growth potential going ahead.

"The banking sector is led by strong tailwinds and is likely to sustain till inflation is under control. Strong Asset Quality, Lower credit costs, and additional provisional and increased capital cushion are positives for the sector. We believe banks with a better portfolio mix, a higher share of floating rate loans, and a strong liability franchise are better. We are optimistic about both names over the long term and hold them in our portfolios," he said.

He is bullish on ICICI as advances are likely to grow by 20 percent YoY, supported by growth being broad across segments, growth in NII supported by healthy loan growth and marginal NIM expansion, moderation in slippages and higher recoveries to improve asset quality and credit costs at normalised levels. Meanwhile, he is positive on Axis Bank as its advances are expected to grow 16 percent led by retail & SME segments, expanding NIM’s, growth in operating profit led by better management of costs and the progress of Citi portfolio.

Ajit Kabi, Banking analyst at LKP Securities also believes both banks have good long-term prospects.

"ICICI Bank and Axis Bank have been performing strongly for many quarters. The legacy NPAs are well provided. The delinquencies from the retail book are at a manageable level. In terms of growth, ICICI Bank has outperformed Axis Bank. The margins of ICICI Bank are at a superior level. Nevertheless, Axis Bank is not far behind and catching up faster. The ROA/ROE of both the banks are superior," he explained.

Brokerage house Motilal Oswal also has buy calls on both the lenders post their earnings. It sees a 34 percent upside in ICICI (target ₹1,150) while for Axis, it has a target of ₹1,130, indicating a potential upside of 21 percent.

Motilal Oswal pointed out that ICICI Bank reported another strong quarter with in-line earnings. The bank's asset quality performance was exemplary as the GNPA and NNPA ratios and PCR improved further. Business growth was strong and broad-based across retail and corporate segments. The bank continued to invest in tech and digital initiatives to further boost growth momentum, said Motilal. It believes the bank is well placed to ride the rising interest rate environment and estimates ICICI Bank to deliver RoA and RoE of 2.2 percent and 17 percent, respectively, in FY25.

Axis Bank delivered a stable performance in 3QFY23, driven by margin expansion, high other income and improving cost metrics. Business growth was healthy, led by the corporate segment. Asset quality continued to improve, even as slippages increased marginally, compensated by healthy recoveries and upgrades. The restructured book moderated further, while a higher provisioning buffer provided comfort, said the brokerage. It tweaked its estimates slightly and expects the lender to deliver RoA/RoE of 1.9 percent/17.3 percent in FY25.

Nirmal Bang also has buy calls on both stocks. For ICICI, it sees an upside potential of 37 percent (target ₹1,174) while for Axis, it has an upside potential of 21 percent (Target ₹1,132).

"ICICI Bank reported strong Q3FY23 performance, which was higher than our estimates on the back of high margins and healthy credit growth. Operating profit increased by 30.8 percent YoY (13.6 percent QoQ) and was nearly 7.7 percent above our estimate. We remain positive on ICICI Bank given its growth outlook and earnings trajectory," said Nirmal Bang.

"Axis Bank reported strong numbers for Q3FY23 ahead of our estimates. RoA/RoE came in at a multi-year high of 1.9 percent/19 percent. Profitability growth was led by margin expansion and higher-than-expected fee income. We have raised its earnings estimates and expect the bank to report RoA of 1.8 percent and ROE of 16.6 percent by FY25E," the brokerage added.

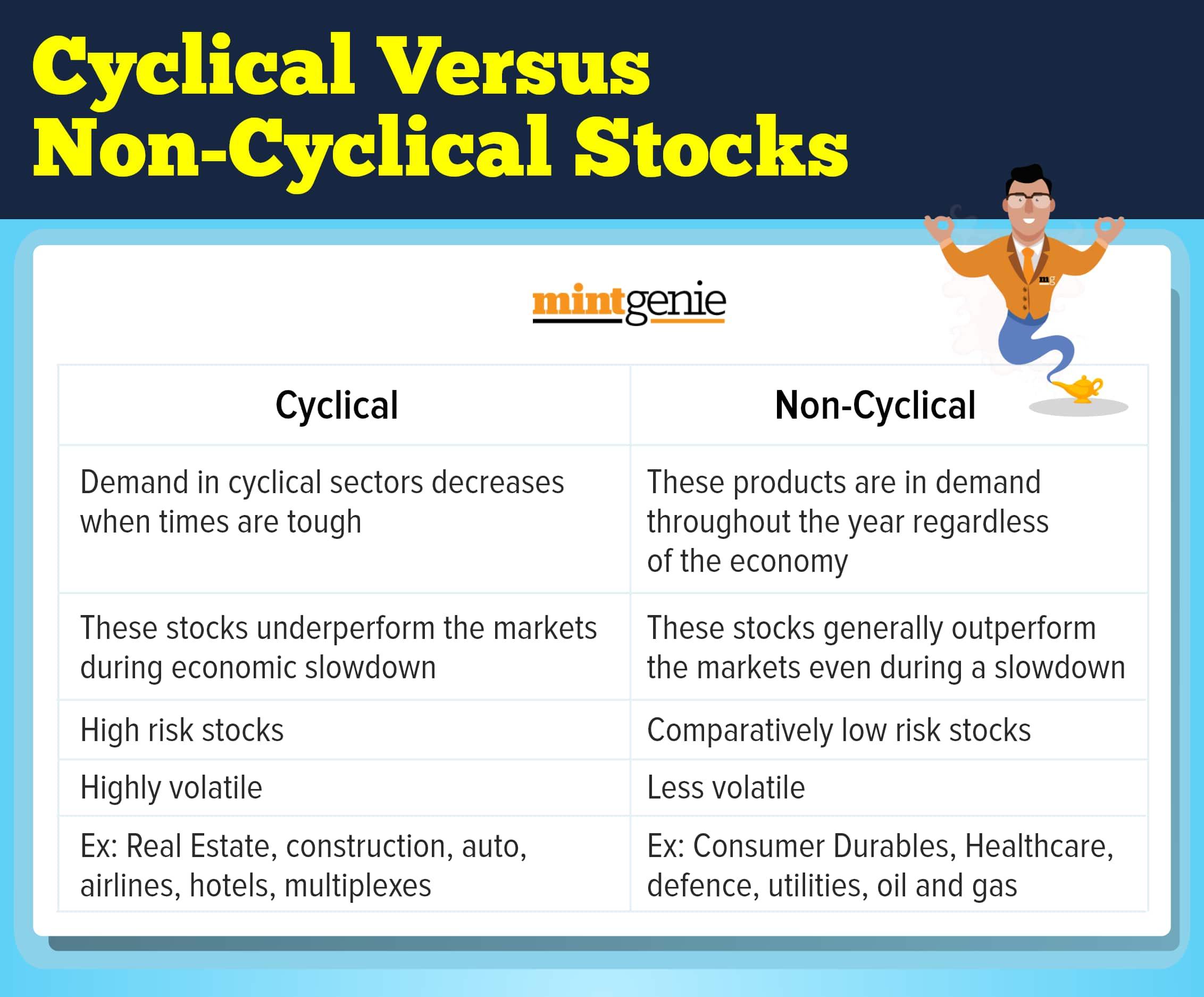

Cyclical vs non-cyclical

First Published: 27 Jan 2023, 03:23 PM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

Growth Vs IDCW plan: What should investors choose for their mutual fund investments?

Team MintGenie