Private sector lender IndusInd Bank beat Street estimates in its June quarter (Q1FY24) earnings. Most brokerages too cheered the lender on the back of robust financials with them retaining bullish calls on the stock after the Q1 results.

IndusInd Bank: Should you buy the stock after Q1 results? Here's what brokerages say

TL;DR.

Most brokerages cheered the lender on the back of robust financials with them retaining ‘buy’ calls on the stock after the Q1 results. The private sector lender posted a 33 percent jump in its net profit at ₹2,124 crore for the April-June quarter.

The private sector lender posted a 33 percent jump in its net profit at ₹2,124 crore for the April-June quarter versus ₹1,631 crore in the year-ago period. Meanwhile, its total income for the quarter also grew 28 percent to ₹12,939 crore and net interest income (NII) rose 18 percent to ₹5,863 crore from ₹4,125 crore last year.

The bank's asset quality also remained healthy as gross non-performing assets (NPA) stood at 1.94 percent, down from 1.98 percent last quarter. Its net NPA also came down to 0.58 percent from 0.59 percent on a sequential basis.

The IndusInd Bank CEO also retained loan growth guidance of 18–23 percent with MFI, including merchant business, likely to grow at the lower end of the range. IndusInd Bank said it would resume building buffer provisions of ₹400–500 crore in FY24.

Stock Price Trend

Post the June quarter earnings, the stock jumped almost 4 percent to its 52-week high of ₹1,443.35 in today's session (July 19, 2023). It is now around 72 percent higher than its 52-week low of ₹840, hit exactly a year ago (July 19, 2022).

The stock has surged over 63 percent in the last 1 year versus a 28 percent rise in Nifty Bank. Meanwhile, it has gained 16 percent in 2023 YTD, giving positive returns in 4 of the 7 months of this calendar year so far.

The stock has gained 3 percent in July so far, extending gains for the fourth straight month. It rose 6.8 percent in June, 11.6 percent in May and 7.9 percent in April. However, it shed 11.2 percent in Jan, 0.5 percent in Feb and 0.9 percent in March.

In the long term, in 3 years, the stock has given multibagger returns, rallying 168 percent.

IndusInd Bank stock price trend

Brokerage views

At least 6 brokerages have a bullish outlook on the stock post its June quarter earnings with a target price of up to ₹1,800, indicating an over 29 percent upside. The brokerages are bullish on the stock on the back of its robust financial performance, stable asset quality, strong growth in NII, recovery in NIMs, and lower slippages.

Morgan Stanley: The brokerage has an ‘overweight’ call on the stock with a target price of ₹1,800, indicating an upside of 29 percent.

With expectations that the rate cycle has peaked, the brokerage sees good returns from IndusInd Bank through compounding, estimate upgrades, and even re-ratings. The firm is positive on the lender's consistent earnings with a better retail deposit mix and easing credit costs.

LKP Securities: The brokerage retained its ‘buy’ call on the stock with a target price of ₹1,794, indicating an upside of nearly 29 percent.

LKP said that IndusInd Bank (IIB) has reported a strong set of numbers with the positives being 1) a 30.3 percent YoY jump in reported profit, led by NIMs surprise and lower provisioning expenses, 2) strong business growth, 3) Lower slippages, 4) Stable PCR level, 5) reduction in restructuring book, and 6) Ample capital cushion. It believes that IIB has made adequate provisioning against the potential stress from a spike in MFI and CV non-performing assets. However, the delinquencies from the vehicles segment and credit costs in the next quarters will be keenly watched.

It further highlighted that the core operating performance of IIB remains healthy but the deposit growth compared to advances in coming quarters will be a key monitorable. Nevertheless, a higher contingent buffer is likely to safeguard the bank from credit disruption from various restructured schemes, it added.

JM Financial: The brokerage reiterated its ‘buy’ call on the stock with a target price of ₹1,560, indicating an upside of 12 percent.

It believes that a) broad-based growth momentum led by positive macros in MFI and vehicle finance industry, b) strong delivery on profitability metrics and c) healthy asset quality should aid in future stock price performance.

The brokerage further noted that while the stock has outperformed Nifty Bank by 14 percent/9 percent/24 percent over 3 months/6 months/1 year, it still trades at attractive valuations of 1.5x P/B FY25E.

Phillip Capital: The brokerage has maintained its ‘buy’ call on the stock with a target price of ₹1,610, indicating an upside of 16 percent.

"IndusInd bank’s Q1FY24 earnings were in line with expectation. Stability in NIM on a sequential basis was driven by the corporate book, higher proportion of consumer loans and utilization of excess liquidity. Asset quality performance was above expectation due to moderate slippage in MFI and corporate book," stated PC.

The brokerage highlighted that the bank is back on a growth trajectory and the domain segment of the bank like vehicle and microfinance is expected to witness accelerated growth. Bank has been able to maintain NIM despite the rise in the cost of funds by increasing the mix of high-yielding loans. It also has a high proportion of fixed-interest rate loans to cushion NIM in a declining rate cycle. Re-deployment of excess liquidity towards loans and reduction in credit cost would drive earnings growth by 14 percent/18 percent in FY24e/25e translating into RoA of 1.83 percent/1.9 percent, it forecasted.

Prabhudas Lilladher: The brokerage also retained its bullish outlook on the stock with a target price of ₹1,530, indicating an upside of 10 percent.

"IIB saw a good quarter with core PAT beating PLe by 5.2 percent driven by better NII, fees and asset quality. NIM at 4.72 percent was 12bps ahead of PLe as a higher retail asset base supported yields. Bank has maintained its growth guidance of 18-23 percent which in our opinion would be a function of superior growth in MFI, vehicle, and small business. We expect a loan CAGR of 18.5 percent over FY23-25E. A key positive has been a consistent increase in retail deposit share to 43.4 percent vs 41.0 percent a year ago. Earnings quality for IIB has been improving since the past 9 quarters led by 1) strong loan growth that was funded by granular deposits and 2) better asset quality which translated to lower credit costs. However, a high proportion of wholesale deposits and lower buffer provisions at 56 bps leaves limited headroom for multiple expansions," it said.

Motilal Oswal: The brokerage also reiterated its ‘buy’ call on the stock with a target price of ₹1,600, implying a 15 percent upside.

As per the brokerage, IIB’s operating performance remains on track, led by steady NII growth and controlled provisions. Asset quality remains steady, with fresh slippages declining QoQ in the corporate book. Overall, the outlook for credit cost remains controlled, it noted. Management is guiding for continued momentum in loan growth at 18-23 percent over FY23-26E. Healthy provisioning in the MFI portfolio and contingent provisioning buffer of 0.6 percent of loans will enable a decline in credit cost, thus driving earnings recovery, added MOSL. It estimates PAT to report a 27 percent CAGR over FY23-25, leading to a 17.5 percent RoE in FY25.

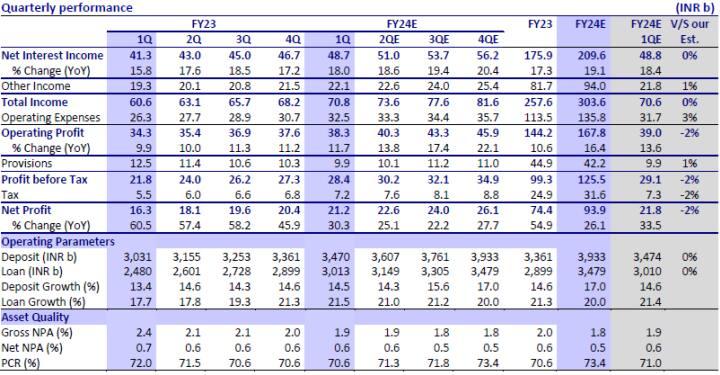

IndusInd Bank quarterly performance: MOSL

First Published: 19 Jul 2023, 12:44 PM IST

Related Stories

markets

Just Dial shares soar 5.5% to reach new 52-week high on healthy Q1FY24 earnings

A Ksheerasagar