IT major TCS kickstarted the earnings season yesterday, April 12, missing Street estimates. Infosys is now set to announce its March quarter results later today, April 13. The IT major is also expected to post subdued numbers in this seasonally weak quarter.

Q3 Earnings: In the December quarter, Infosys reported a 20.2 percent year-on-year (YoY) rise in consolidated revenue at ₹38,318 crore. Meanwhile, its consolidated net profit for the quarter rose 13.4 percent YoY to ₹6,586 crore. The IT major, however, surprised the Street by raising its constant currency (CC) revenue growth guidance for FY23 to 16-16.5 percent from 15-16 percent earlier. However, it retained its operating margin guidance for FY23 at 21-22 percent. The company's constant currency revenue growth came in strong at 13.7 percent YoY, and 2.4 percent sequentially.

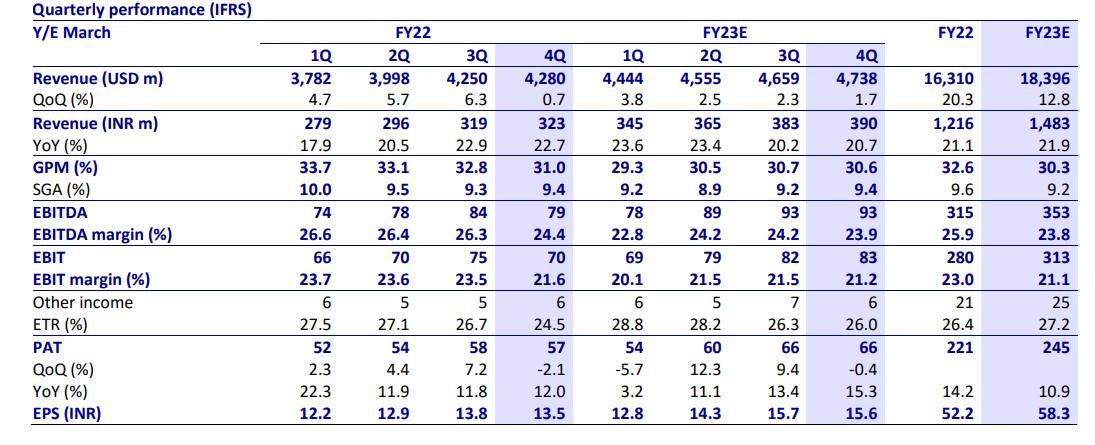

Let's take a look at what analysts expect from this IT major in the March quarter.

Brokerages see the company reporting double-digit year-on-year (YoY) growth for both its net profit and revenue in the March quarter, however, CC revenue growth is likely to remain muted. The EBIT margin for the IT major is expected to come in around 21-22 percent.

Motilal Oswal: The brokerage expects Q4 profit for the firm to rise 15.3 percent YoY to around ₹6,600 crore but be down 0.4 percent on a sequential basis. Its overall consolidated revenue in rupee terms is estimated to jump 20.7 percent YoY, as per MOSL, to ₹39,000 crore, while in dollar terms, its revenue is seen growing 1.7 percent QoQ to $4.7 bn.

The brokerage expects muted CC revenue growth of just 0.6 percent QoQ due to seasonality and weakness in financial services. Also, US dollar growth implies a 110 bps of currency tailwind, it added. There is no material change in large deal momentum compared to last quarter and the operating margin is likely to remain under pressure in the seasonally weakest quarter for Infosys, it said. MOSL expects the margin to decline by 30 bps QoQ. IT budget allocation, deal TCV, outlook on BFSI and attrition are key things to be watched out for, it said.

ICICI Securities: As per the brokerage, Infosys' superior digital capability, focus on large cost optimisation, digital transformation, integrated deals and strong management execution would enable it to remain the fastest-growing large-cap IT services company globally. It sees Infosys starting with a conservative revenue growth guidance of 6-8 percent in CC terms for FY24E given the overhang around the recent banking crisis and limited visibility on how it may unfold over the next few months. The brokerage has forecasted a 7.4 percent CC revenue growth for the firm in FY24E followed by strong double-digit growth of 12.7 percent and 13.8 percent in FY25E and FY26E, respectively. For Q4FY23, it expects a 0.1 percent QoQ growth in CC terms leading to FY23E CC revenue growth of 16.4 percent, at the higher end of guidance of 16-16.5 percent.

IDBI Capital: The brokerage expects a 20.5 percent YoY and 4 percent QoQ rise in Infosys' Q4 net profit at ₹6,852 crore. Meanwhile, it sees the firm's overall revenue to jump 20 percent YoY to ₹38,701 crore and dollar revenue growing 1 percent QoQ to $4.7 bn. IDBI forecasts revenue growth to be flat in CC terms and a cross-currency tailwind of 100 bps. Growth is expected to be muted due to delayed decision-making by clients, it added. EBIT margin is likely to expand by 83 bps QoQ to 22.3 percent mainly led by a flatter pyramid and reduced attrition levels, said the brokerage.

Kotak Institutional Equities: As per the brokerage, Infosys' net profit will jump 12.2 percent YoY to ₹6,379 crore in Q4 while rupee revenue will post a 20 percent growth at ₹38,693 crore. It expects Infosys to post a muted 0.1 percent CC revenue growth driven by both cloud and digital programs and cost take-out agenda of clients and sees a 25 bps sequential decline in Ebit margin with headwinds from visa costs (40 bps) partially offset by operational efficiencies and lower pass-through expense. Kotak noted that it does not expect material incremental revenue contribution from the Daimler deal. It also said that front-ended growth guidance will give a lot more comfort and even create scope for upgrades; back-ended growth guidance, meanwhile, may not be viewed favourably.

Sharekhan: Infosys is likely to post a 14.2 percent rise in its Q4 net profit at ₹6,494 while its rupee revenue is expected to jump 19.6 percent to ₹38,598 crore, said Sharekhan. The brokerage estimates the IT major to post a flat CC QoQ revenue growth with a likely 80 bps cross-currency tailwind that can lead to QoQ dollar revenue growth of 0.8 percent. Weakness in operating margin is likely and the brokerage expects Ebit margins to fall by 25 bps QoQ, it added.

Key Monitorables: 1) Tech budgets by clients; 2) Impact on BFSI in US & Europe 3) Large deal pipeline and wins; 4) Impact on discretionary spends, 5) Attrition level and trends 6) Margin outlook, 7) Outlook on telecom, retail, BFSI & Hi-tech verticals, 8) IT budget allocation