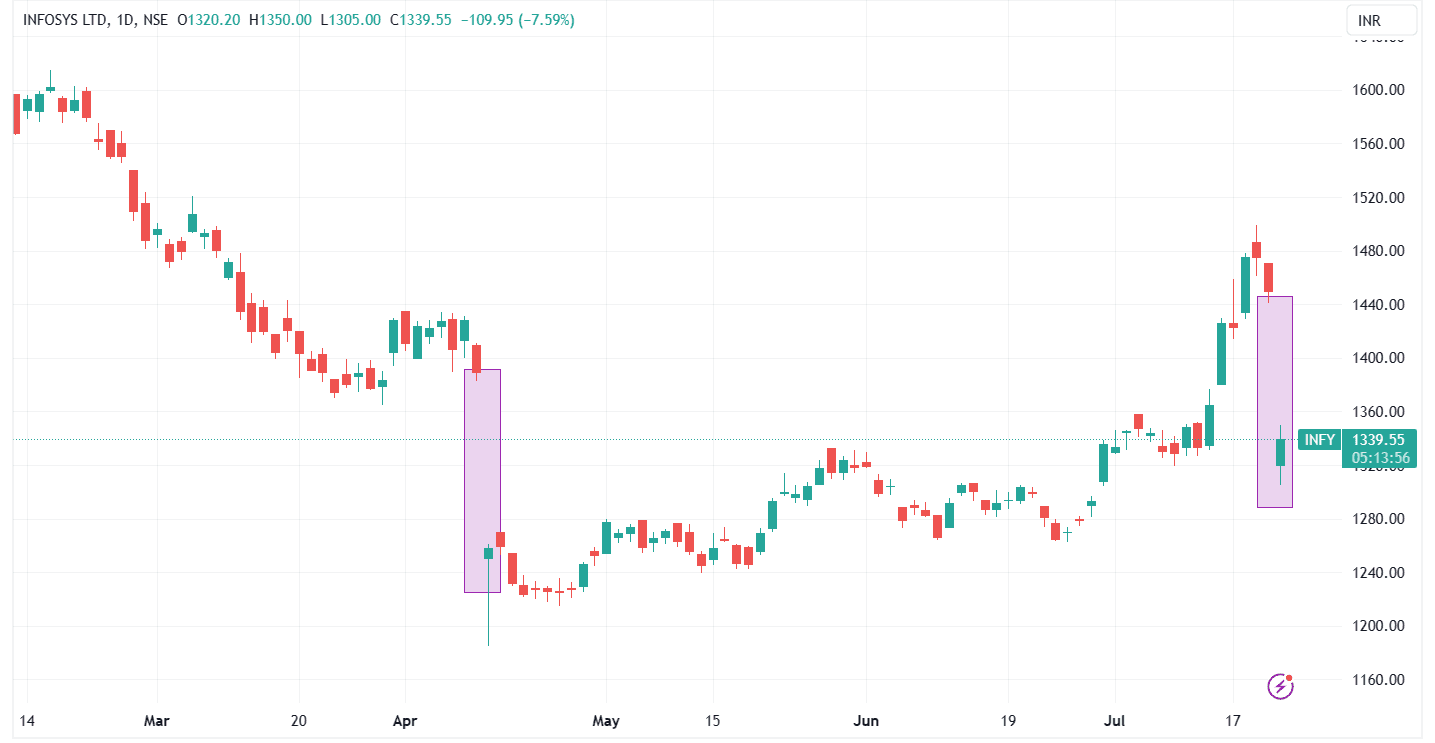

Infosys, the country's second largest IT services company, witnessed a sharp decline in its share price, falling by 10% to ₹1,305 apiece during early trade on Friday. The decline came in response to the company's lower-than-expected net profit in Q1 FY24 and a surprising revision of its revenue growth guidance for FY24 to 1-3.5% in constant currency terms.

This decline is reminiscent of a similar intraday fall that occurred on April 17 after Infosys announced its Q4 FY23 results. On that day, the shares opened with a substantial gap down as the company, for the first time since FY19 lowered its FY24 growth outlook to the single digit of 4-7%.

The company on Thursday reported an 11% jump in its consolidated net profit to ₹5,945 crore. This came below company expectations as certain projects saw unexpected deferrals that are discretionary in nature and have been pushed out to a later stage.

While the revenue from operations during the quarter came in at ₹37,933 crore, an increase of 10% YoY, the operating profit stood at ₹9,064 crore, a surge of 15.25% YoY.

Despite the soft 1Q performance, the deal pipeline remains healthy, with multiple large and mega deals being pursued actively in the areas of cost efficiency, vendor consolidation, and process optimization.

The company remains confident of achieving an EBIT margin in the range of 20–22%, despite the sharp cut in revenue guidance.

Following the company's Q1FY24 scorecard, brokerage firms delivered mixed views on the stock. Domestic brokerage firm Motilal Oswal is optimistic about the company's prospects, considering it a key beneficiary of the expected acceleration in IT spending in the medium term. The brokerage has revised its estimates and currently values the stock at 20.5x FY25E EPS.

It continued with its 'buy' rating on the stock with a target price of ₹1,600 apiece.

Global brokerage firm JM Financial maintains its 'hold' rating on the stock and trimmed its price target to ₹1,350 apiece from ₹1,360 earlier.

"The company revised its FY24E CC revenue growth guidance from 4-7% earlier to 1-3.5%. The implied CQGR came down from 1.6-2.7% earlier to (0.27%)-1.36%. This is despite the company winning USD 2.3 billion in TCV of deals during the quarter, with a net new component of 56%."

"Management attributed a sharp cut in guidance despite this to sustained pressure on the current book of business (driven by discretionary cuts in parts of BFS, Hi-Tech, Retail, and Communication) as well as a delay in ramp-ups and revenue conversion of large deals," said JM Financial.

Phillip Capital, on the other hand, revised its target price lower on the stock to ₹1,390 apiece from ₹1,580 earlier and downgraded its rating to neutral.

"We cut our FY24/25 PAT estimates by 4-6% on lower growth guidance by the company. We are now forecasting USD revenue growth of 3.2/10% with 21.1%/21.5% EBIT Margins in FY24/25. We now value Infosys at 20x FY25 EPS (22x earlier), on lower growth assumptions," said Phillip Capital.

What are the technical charts suggesting?

On the technical front, Gaurav Bissa, VP, InCred Equities, said, "Infosys has witnessed a strong correction after it announced weak results. The stock has reversed from a descending trendline hurdle on the weekly charts. However, the stock is currently trading above the previous swing low of 1250.

On long-term charts, the stock is trading comfortably above the 15-year ascending trendline breakout area, suggesting the structure remains strong for the long term. In the short to medium term, the stock may oscillate between the 1250–1500 range.

Long-term investors can use this dip as a buying opportunity with a time horizon of 18–24 months for fresh lifetime high levels in Infosys."

42 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.