Domestic brokerage firm Systematix Institutional Equities in its research report said that Inox Wind is on the path to recovery after almost seven tough years faced by India’s wind power industry.

Inox Wind, part of the INOXGFL Group, is engaged in manufacturing and selling wind turbine generators (WTGs) and engineering, procurement, and commissioning (EPC) services. It provides services in operations and maintenance (O&M), common infrastructure facilities for WTGs, EPC, and wind farm development through its subsidiaries, INOX Green and Resco Global Wind Services Limited (Resco).

It stated that the last decade saw a series of government interventions and frequent policy changes, later laced with extensive lockdowns during the pandemic, which aggravated the situation further. In recent years, as per the brokerage, the sector experienced a downturn in installations and a highly leveraged balance sheet due to a significant decline in wind capacity additions in India.

However, with favourable policy changes introduced in FY23 and FY24, coupled with strategic actions, Inox Wind is at the forefront of reviving its operations which was already evident from the company's performance in 1QFY24, where the company turned EBITDA positive after reporting negative EBITDA over FY18-FY23 (barring FY19), as highlighted by the brokerage.

"In the Indian wind energy solutions space, we believe INXW is a market leader since it is one of the only two companies that provide end-end-end wind farm development services. Suzlon Energy Limited (SUEL: NOT RATED) is the only clear competitor, in our view. Together, INXW and SUEL command a market share of 50%," said Systematix.

Opportunity

The brokerage believes Inox Wind plays a pivotal role as India moves towards its wind capacity addition commitments with renewed thrust.

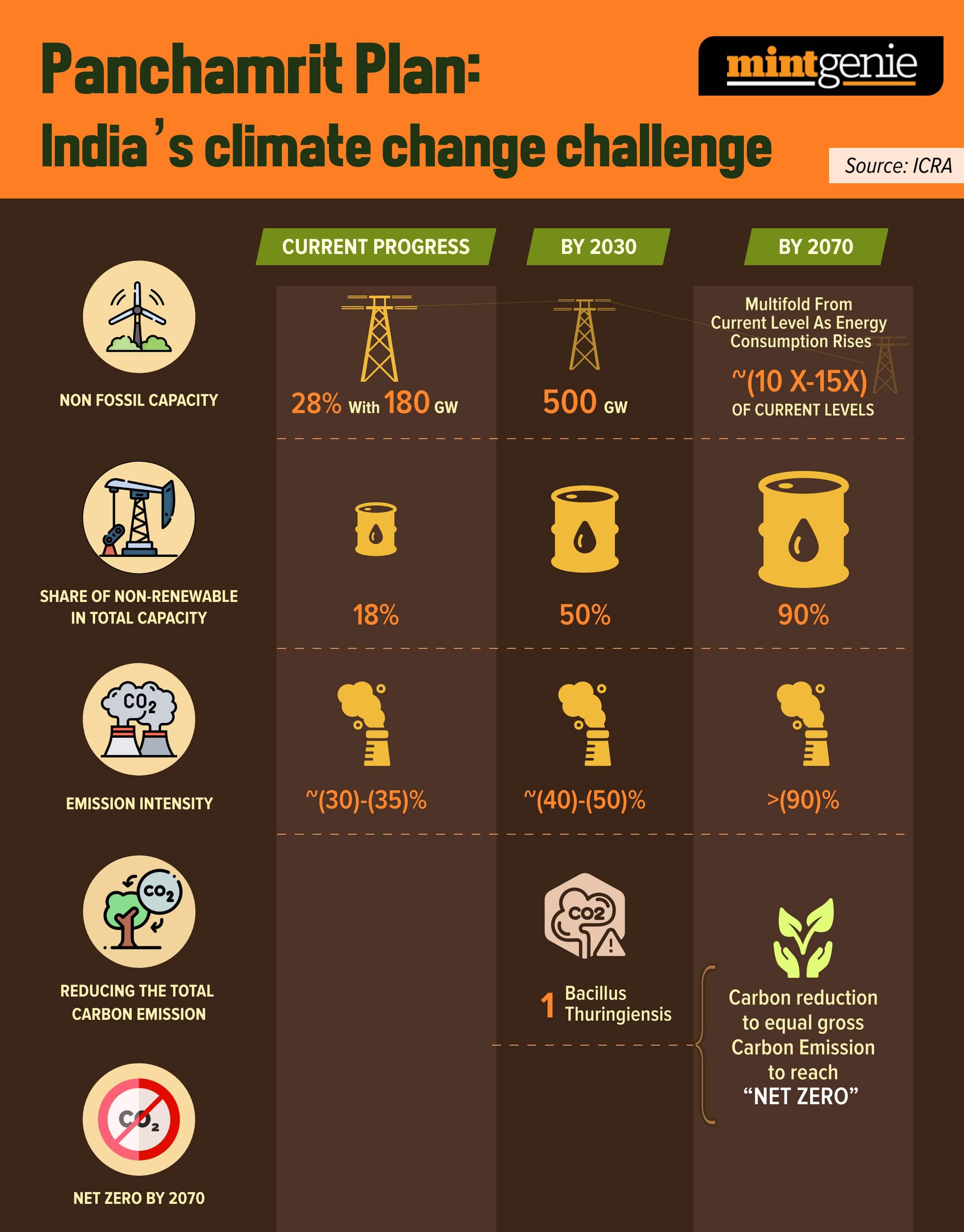

As part of its commitment to reducing emission intensity by 45% by 2030 compared to 2005 levels, India aims to generate approximately 50% of its electricity from non-fossil-fuel-based sources (currently at 43%). This underscores the critical role that Inox Wind is poised to play in India's transition towards cleaner, more sustainable energy sources, stated the brokerage.

Further, the company's upgrade to the latest technology (3MW WTG received type certification from TUV SUD and will begin commercial production in 3QFY24), lean cost structure, and deleveraging efforts put it at the forefront of benefiting from India’s transition to clean energy, it added.

Strong order book

As per brokerage estimates, Inox's net order book of 1.3 GW as of June 2023 is expected to translate into revenue of ₹66 billion for the next two years. It further expects the company's order book to expand significantly as new capacities come on stream in India, driven by various government initiatives.

Looking to turn net debt-free by FY25

The brokerage highlights the several strategic initiatives taken by Inox Wind to strengthen its balance sheet and turn net debt-free by FY25. These include Inox Green IPO, asset monetisation, infusion of the promoter’s preference share capital, and block sale of equity stake by the promoter.

It also points out that the company has neither defaulted on debt repayments nor resorted to debt restructuring, a huge distinguishing factor over peers. It noted that the company enjoys strong group backing, with one of the highest promoter shares in its shareholder base amongst the listed companies in the wind industry.

Valuation

The brokerage initiated coverage on the stock with a 'buy' rating with a target price of ₹262 apiece, based on 23x FY25E EPS. The brokerage also notes execution delays, insufficient grid capacity, and logistical constraints as key risks.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before making any investment decisions.