Brokerage house Kotak Institutional Equities has initiated coverage on four IT services stocks, mainly from the Engineering and R&D (ERD) services space.

Kotak initiates coverage on 4 IT stocks with one ‘buy’, one ‘add’ and two ‘sell’ calls; details here

TL;DR.

Brokerage house Kotak Institutional Equities has initiated coverage on four IT services stocks mainly from the ERD services space with a ‘buy’ call on Cyient, an ‘add’ call on Persistent Systems and ‘sell’ calls on KPIT Tech and Tata Elxsi.

The brokerage believes that the Indian ERD services market can compound at 10-12 percent in the next five years, driven by investments in major tech, product and end-market themes, strengthening capabilities of service providers and a change in the sourcing patterns of enterprises. Pureplay Indian ERD service providers are well-positioned to benefit from structural growth drivers, but expensive valuations limit meaningful plays in the sector, it added.

It has a ‘buy’ call on Cyient, an ‘add’ call on Persistent Systems and ‘sell’ calls on KPIT Tech and Tata Elxsi. Meanwhile, it has also retained its ‘sell’ call on L&T Tech.

The stock pick framework is based on (1) better capabilities with a strong presence in faster-growing areas, (2) diversified industry exposure for sustainable growth, (3) improving competitive positioning, (4) healthy cash conversion and better return ratios and (5) reasonable valuations, informed Kotak.

As per the brokerage, Indian service providers have excellent capabilities across key growth themes. The uptick in digital engineering spends would be driven by six major themes: (1) cloudification, (2) connectivity, (3) IT-OT convergence, (4) industry 4.0, (5) Connected, Autonomous, Shared, Electric (CASE)— elevated growth till CY2025E, followed by significant moderation and (6) sustainability. These themes would be growth drivers of ERD spends across industries, explained Kotak.

It further stated that ERD services are discretionary and tend to have a high correlation to industry cycles with a significantly lower ‘maintenance’ component of work as compared to IT services. Typically, this benefits the companies that have higher exposure to an industry undergoing technology transition, e.g. in the auto segment.

Among industries, software and the internet has the highest share of digital ERD spends and contribute 41.9 percent of global digital ERD spends as of CY2022, as per Zinnov. Media and entertainment, BFSI and healthcare verticals too would see a faster uptick in ERD spends over CY2022-26E, it added.

Stocks

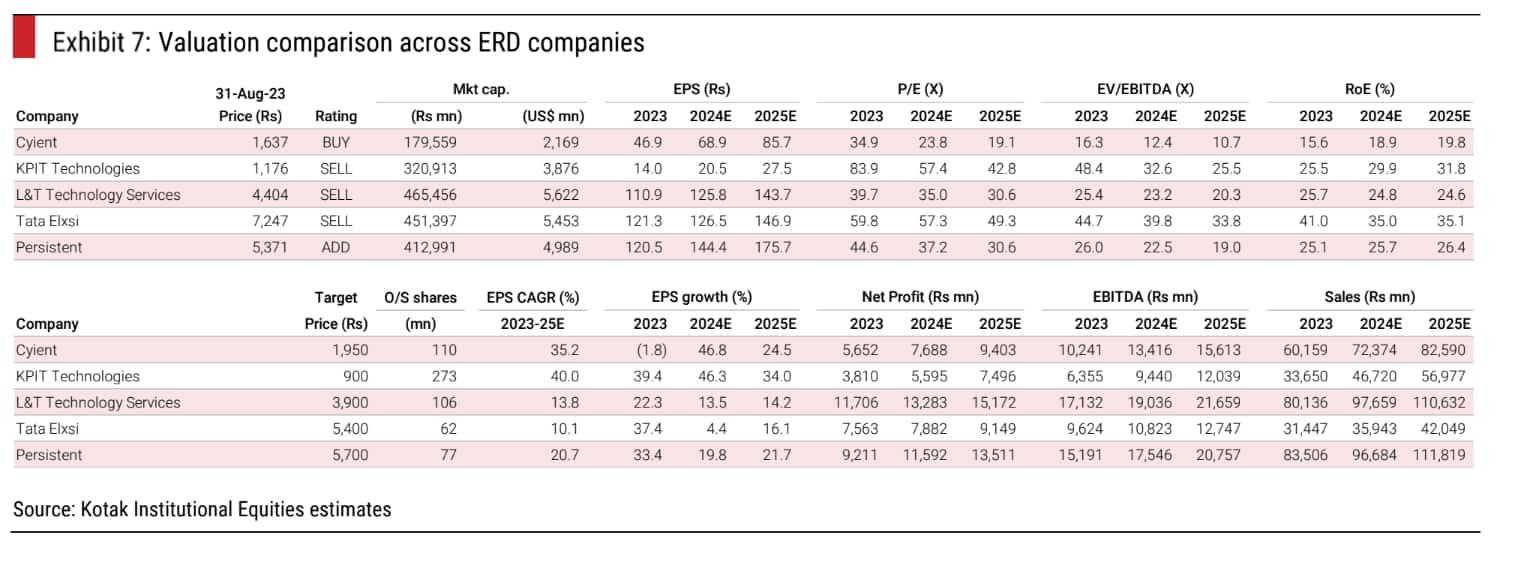

Cyient: The brokerage has a ‘buy’ call on Cyient with a target price of ₹1,950, indicating a 19 percent upside.

Cyient has developed strategic relationships with marquee clients in aerospace and large telecom operators, leveraging its mechanical engineering capabilities. It has since diversified into other verticals such as automotive, semiconductor, mining and utilities. Revenue growth has been volatile historically due to higher exposure to the aerospace industry. However, over the past three years, the company has been investing in (1) diversification of revenue from aerospace to high-growth areas such as mobility, connectivity, energy and sustainability, (2) enhancing capabilities in embedded and digital engineering services, (3) geo expansion to Nordics and Japan, (4) realigning incentives of sales teams by rewarding incremental revenue from deal signings rather than purely focusing on deal TCV, said Kotak.

For the consolidated business, it expects constant currency organic revenue growth CAGR of 12.2 percent over FY2023-26E and EBIT margin improvement from 12.8 percent in FY2023 to 15.0 percent in FY2026E. It expects EPS CAGR of 23.0 percent over FY2023-26E.

Persistent Systems: The brokerage has ‘add’ call on the stock with a target of ₹5,700, implying a 6 percent upside.

Persistent is well-established as a leader in product engineering. It has transplanted product engineering expertise to IT services, resulting in tech-led expertise in new technology stacks with high growth potential, such as cloud, data & analytics, AI, SaaS implementation, low code and automation. Under the current CEO, Persistent has morphed into a credible challenger in IT services. The new CEO Sandeep Kalra resumed focus on services, aligned the organisational structure and incentives, beefed up the management team through external hires, built strength in large deals and instituted good account management practices and cost discipline, explained Kotak.

It expects constant currency organic revenue CAGR of 14.5 percent over FY2023-26E and EBIT margin improvement from 14.9 percent in FY2023 to 16.3 percent in FY2026E. Revenue growth will be driven by strong participation in an improved discretionary spending environment aided by leadership in product engineering and the position of a credible challenger in fast-growing segments of IT services. Margin expansion will be driven by higher utilisation and operating leverage. It estimates an EPS CAGR of 21.6 percent over FY2023-26E.

KPIT: The brokerage has a ‘sell’ call on the stock with a target price of ₹900, indicating a 23 percent downside.

KPIT is among the largest software integration services providers that exclusively works with automotive clients and has strategic partnerships with OEMs and tier-1 suppliers. The company has benefitted from demand tailwinds in the auto industry. It expects elevated CC organic revenue CAGR of 21.4 percent over FY2023-26E aided by demand tailwinds and ramp-up of Renault and Honda deals. Revenue growth is likely to moderate from elevated levels as the R&D spends of clients normalise starting FY2026E. It estimates EBIT margin improvement of 440 bps over the period to 18.9 percent and EPS CAGR of 35.7 percent over FY2023-26E. The stock trades at expensive 43X FY2025E, it added.

Tata Elxsi: The brokerage has a ‘sell’ call on the stock with a target price of ₹5,400, indicating a 25 percent downside.

Tata Elxsi is strong in embedded services across three focus verticals—(1) transportation, (2) media & communication and (3) healthcare medical devices. Embedded design has seen a sharp uptick in spends post FY2020 driven by increased spends on digital, however, demand headwinds in media and medical devices businesses have been a drag on growth.

It expects CC revenue CAGR of 14.5 percent over FY2023-26E and EBIT margins stable at 28 percent over the period. Revenue growth during this period would be driven by embedded service offerings in transportation and medical devices verticals. It also estimates an EPS CAGR of 12.7 percent over FY2023-26E.

L&T Tech: The brokerage has a ‘sell’ call on the stock with a target price of ₹3,900, implying a 11 percent downside.

LTTS is the largest pureplay ERD service provider in India with a strong positioning in fast-growing and underpenetrated ERD services. However, benefits from scale and capabilities have not been reflected in the scale-up of top accounts, leading to significant growth moderation and underperformance against peers.

LTTS’s revenue CAGR has moderated to 9.0 percent over FY2020-23 as compared to 17.8 percent CAGR over FY2017-20. Kotak expects LTTS’ organic revenue growth at 8 percent in FY2024E to underperform pure-play ERD peers. It forecasts a 10.8 percent revenue CAGR over FY2023-26E and EBIT margin being flat at 17 percent during the period. It estimates an EPS CAGR of 13.8 percent over FY2023-26E. “We maintain a SELL rating on LTTS, given moderating growth and expensive valuations,” it said.

Pecking order: Cyient (BUY) > PSYS (ADD) > LTTS > Tata Elxsi > KPIT (SELLs).

Source: Kotak

First Published: 06 Sep 2023, 04:30 PM IST

Topics to follow

Related Stories

markets

Wipro: This large-cap IT stock is down 43% from its all-time high; what lies ahead?

A Ksheerasagar