Avenue Supermarts posted a 3.14% rise in consolidated net profit, at ₹427 crore, for the quarter ending March 31, 2022 (Q4FY22).

It's profit after tax (PAT) margin came in at 4.8% in the given quarter as compared to 5.5% in the same quarter of fiscal previous to last.

Consolidated revenues jumped to ₹8786 crore as against ₹7412 crore and EBITDA or pure profits stood at ₹739 crore versus ₹613 crore.

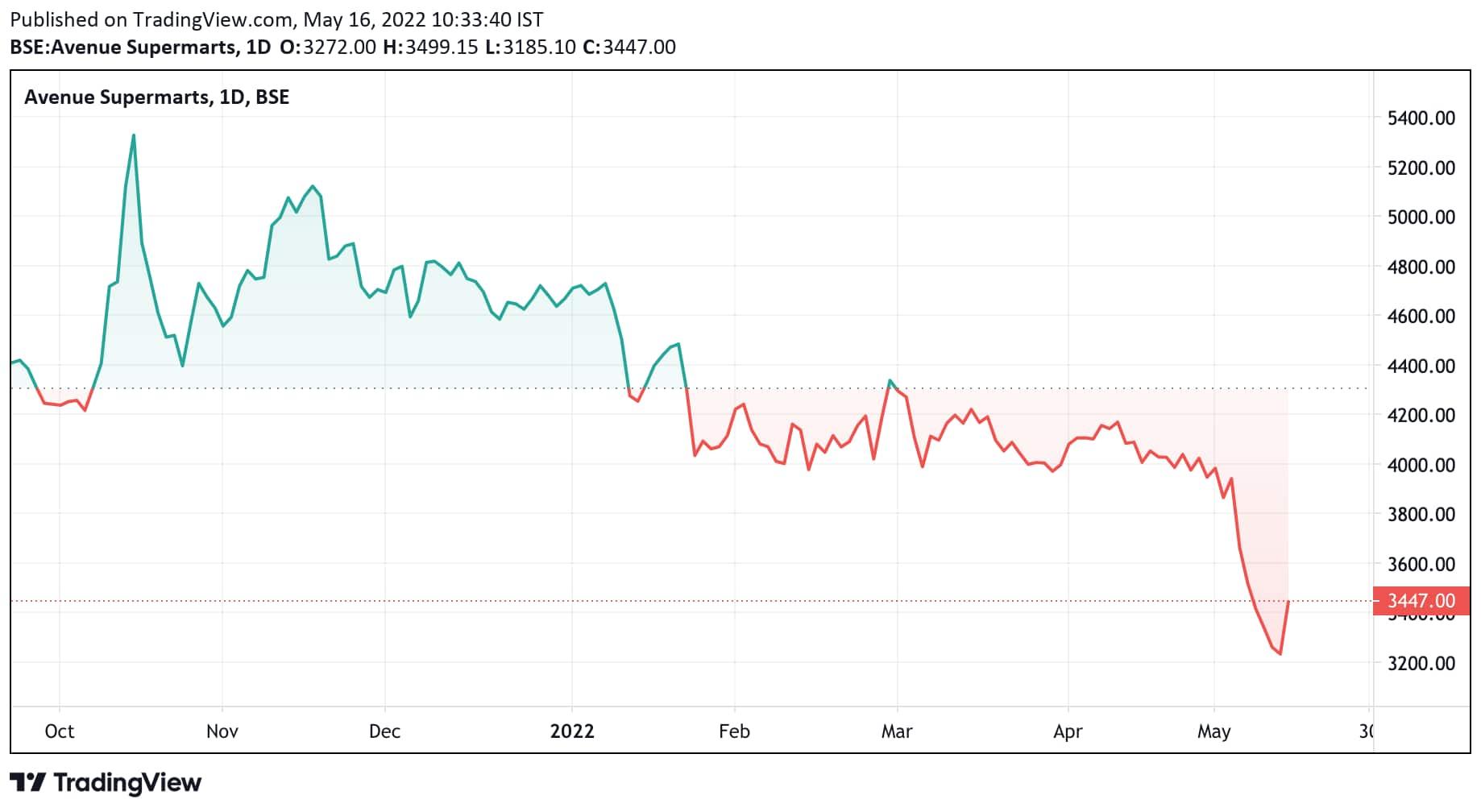

Share price of Avenue Supermarts jumped in early trade on Monday May 16, 2022, and was trading at ₹3445.80 per share, up 6.66%, on the NSE.

Recent market correction sent the DMart owner's stock price crashing like rest of the sector.

Nifty FMCG has fallen 5.56% over the past six months while its one-year returns currently stand at 5.86%.

Australian research firm Macquire is positive on the company's future. Post the results, the agency gave Avenue Supermarts ‘outpeform’ rating. It said, “Healthy recovery seen in the FMCG business in 4Q post Omicron wave reaffirms DMart’s mindshare in the value grocery segment.”

However, it also said, “We find weaker growth across discretionary higher-margin non-FMCG segment and across the ecommerce businesses concerning.”

Even though Macquire has cut the target price by 3%, from ₹4600 to ₹4400 per share, the agency has maintained its ‘outperform’ rating.

It said, “Recovery in FMCG sales suggests continued consumer preference for DMart in the value grocery segment. Further, with DMart earning a percent markup on product prices, inflation enhances the leeway to manage costs. Lastly, we do not see this weakness in non-FMCG recovery as a structural concern albeit acknowledge that further performance would need clarity on the same (likely in analyst meet/ pre-1Q release). DMart’s proven model of profitable expansion in the largely unorganised grocery market (just 4-5% organised), bolsters our bullish stance over the medium term.”