Domestic growth has slowed down as indicated by various macro indicators. Even the quarterly results of domestic-oriented companies and their growth outlook have indicated a clear slowdown, said Rajnish Girdhar, Chief Executive Officer of Karma Capital. In an interview with MintGenie, Girdhar shared his views on markets and economy and the sectors one should bet on.

Edited excerpts:

What is your broader view of the market for FY24? What are the key negatives and positives?

FY24 is expected to begin on a rough note for equity markets as headwinds in the form of inflation, interest rate hikes, banking crisis and global recession have muddled the near-term outlook for the economy.

Markets are thus expected to be rangebound in the short term.

As per the latest RBI report, the Indian economy is intrinsically better positioned than many parts of the world to head into a challenging year ahead, mainly because of its demonstrated resilience and its reliance on domestic drivers.

From a long-term perspective though, the growth prospects for India look significantly better than most developed economies.

The discretionary spending by the Indian consumer coupled with the various government initiatives towards infrastructure and reform activities should drive the growth of the economy.

Moreover, with crude oil prices cooling off, headline inflation in India is likely to moderate in the coming months, however, monsoon related issues could be a key risk.

El Nino conditions could have a bearing on the monsoon, which in turn, would have an impact on food prices, inflation, and economic growth.

The mid and small-cap space has been under pressure of late. Is more correction due or we are going to see the trend reversal soon in the mid and small-cap space?

Small and mid-cap space has been battered, especially in the last few months and has been broad-based where the richly valued companies have corrected even more.

So, depending on the valuations and growth outlook for the company, it is possible that specific companies may correct even from here.

For instance, we have seen some companies reversing nicely from their lows.

These types of corrections are healthy as they allow long-term investors to enter into good-quality companies at reasonable valuations

A bear market is usually followed by a bull market. What sectors should we bet on now if we have to reap the benefits of a coming bull market?

Volatility is an inherent phenomenon of equity markets. Generally, we have seen that investors who ride the volatility have reaped benefits.

We have observed this umpteen times in the past, the most recent being Covid-19 led to a fall in prices.

If one believes in the structural store of India, any downturn can be seen as an opportunity to invest.

Pharma and telecom are two sectors where we see significant earnings growth over the next two years.

In the last five-seven years, we have seen capital misallocation in the pharma sector, with money being deployed in the US market for growth which has not delivered desired return.

These companies have renewed their focus on the domestic market and are generating significant free cash flow.

These companies are now debt free, and we see a long runway of growth ahead of them and we believe that they are positioned where FMCG companies were 10 years back.

We have seen consolidation in the telecom sector with the top two players now controlling more than 75 percent revenue market share.

With higher data consumption per subscriber and new technology adoption, ARPUs will go up and these players will be key beneficiaries.

What is your outlook on domestic growth? Should we be worried about factors such as El Nino?

Domestic growth has clearly slowed down as indicated by various macro indicators.

Even the quarterly results of domestic-oriented companies and their growth outlook have indicated a clear slowdown.

Until the last few quarters, urban India was doing well, and premium and luxury segments were doing well. But even though that has slowed down, the rural economy has anyway been struggling for quite some time now.

Further, even the recent central government budget didn't provide any specific boost to the consumption part of the economy.

It remains focused on infrastructure and long-term growth drivers.

Further, the recent reports of a possible El Nino effect on Indian monsoons have further clouded the outlook.

We were blessed to have three back-to-back La Nina years which led to above-average rainfall in most parts of the country and helped keep the rural economy afloat.

I think the government has created sufficient buffers to take possible actions to boost near-term growth if El Nino really does play out.

Banking stocks, especially the PSU ones, have fallen significantly this year so far. What is your view on the PSU banking space? Why did they fall? What is the road ahead for them?

In the last two years, we saw PSU banks get significantly related as the normalisation of credit cost led to improved profitability and the fact that they were valued at significantly lower P/B multiples at the time.

In the past few months, while fundamentals have not seen a drastic change, the macroeconomic environment and overhang of exposure to a large conglomerate have led to stocks underperforming.

Structurally, however, we have seen a steady loss in PSU banks' loans and deposit market share.

There is a gap in the core profitability and return ratios of PSBs as compared to private banks due to weaker margins and higher credit costs.

Also, there is a substantial gap on the growth front both in terms of deposits and loans.

SBI, the largest bank in the country, is the exception among PSBs and remains a proxy to the banking sector.

The strong deposit franchise and wide distribution network of the bank cannot be replicated, and we could also see potential value unlocking in its subsidiaries.

Auto and FMCG stocks gained anticipating a rural recovery. Is there more steam left in these two sectors or should we start booking profits?

Auto stocks have been through a tough period in the last four years on account of multiple external headwinds. So, it was only a matter of time before they came out of the woods and saw a pent-up demand.

In addition, individual companies have taken multiple steps to come out of the stagnation such as new model launches, entering new segments and markets, etc.

Stock prices are only reflecting the potential growth in these companies.

FMCG stocks have seen a multiyear time correction although there have been stock-specific movements depending on their specific end consumer segment, geography, rural/urban mix, etc.

During a challenging macro environment like now, investors tend to shift to defensive sectors like FMCG.

However, I would say that there are some interesting bottom-up stocks in the FMCG sector worth evaluating right now.

When do you expect the Fed to hit a pause button on rate hikes?

All central banks across the world are focused on taming inflation as their top priority.

With the global liquidity glut over the past years, inflation seems to be much more sticky than earlier anticipated, especially in developed markets like the US.

However, barring externalities like the sorts of SVB banks, we do not expect the Fed to mid-way pause their rate hikes with a terminal Fed rate in the vicinity of 5.5 percent.

In India, RBI has front-loaded 250 bps of a rate hike in the last year already and we do not see much room for it to go higher.

A gap of 1-1.5 percent from the US rates should also be reasonable in terms of not seeing a drastic impact on our currency.

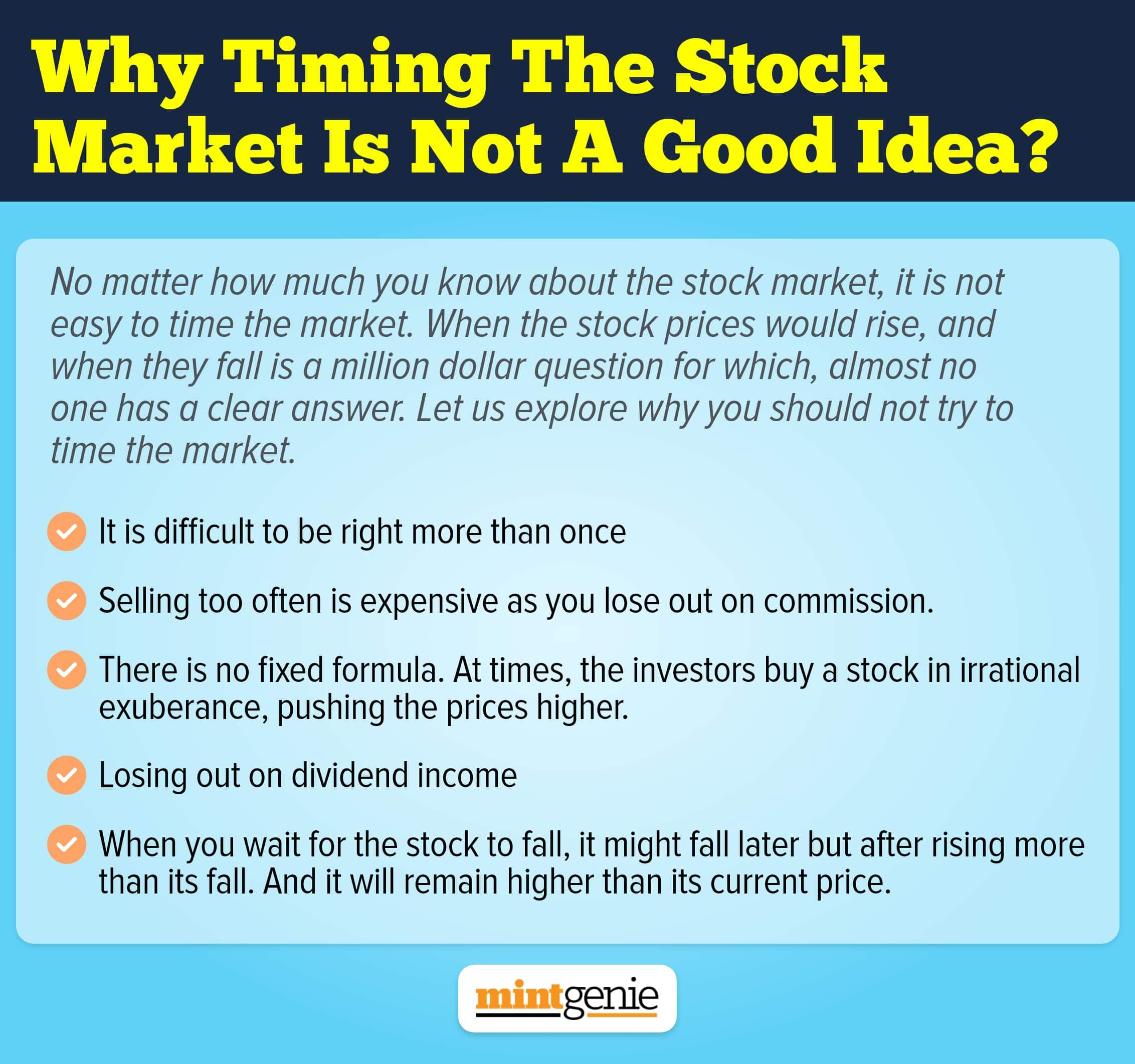

How should retail investors trade in this market? Should they avoid riskier equities and invest in safe-haven and fixed-income assets?

Be it equity or debt or gold, timing any market is difficult. Rather, retail investors need to have a balanced exposure to different asset classes, depending on their age, goals, and risk profile.

They should not trade in and out of different asset classes in the short term but always have a disciplined approach to investment in different asset classes.

This will allow them to benefit from the cycles that each asset class goes through.

Disclaimer: The views and recommendations given in this article are those of the expert. These do not represent the views of MintGenie.